It is premature to abandon global reflation theme

by: Gavyn Davies

The global reflation regime that has been dominant in the financial markets for much of the past 12 months has paused in recent weeks. Many commentators, including James Macintosh at the Wall Street Journal and the FT’s Gillian Tett, have suggested that this pause in the markets is giving ominous signals about the health of global economic activity. Concerns have been expressed about the strength of official US GDP data in 2017 Q1, and there have been unexpectedly low readings for core inflation in several economies.

This shift in mood is probably too pessimistic. The change in market behaviour has so far been small, relative to the large rise in equities and the decline in bond prices seen since world activity bottomed in February 2016. Furthermore, while there has been a modest slowdown in US activity indicators since March, the growth rate remains well above trend, and the official GDP numbers are likely to be much stronger in 2017 Q2 and Q3.

However, there are legitimate concerns about the ability of the Trump administration to deliver the large fiscal stimulus that had been expected. These concerns need to be addressed in the announcements on tax policy that are expected imminently.

What, exactly, is the “reflation” trade? Since the China currency squall blew over a year ago, indicators of global growth have picked up sharply, and fears of deflation in the Eurozone and Japan have evaporated.

These developments were taken as evidence that an expansionary demand shock was driving the global economy towards recovery. First, in February 2016, equities embarked on a new leg of their long-term bull market, defying forecasts of a global recession. Then, in mid 2016, global bonds entered a bear tack as deflation risks were priced out of markets. Finally, the reflation trade received a large further boost in November, when it seemed clear that the Trump administration intended to implement a huge cut in corporate and household tax rates, Congress permitting.

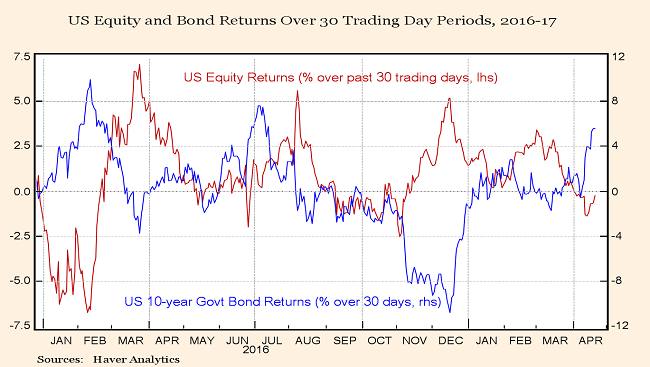

This is how US equities and bonds have responded to changing perceptions of reflation since the start of last year:

In the last few weeks, the theme has begun to fade in the asset markets. The graph below shows 30-day returns from US bonds and equities. These returns have continued to move in opposite directions, which is what would be expected if the global economy is being driven by shocks to aggregate demand. (Higher demand growth should raise profit expectations and thus help equities, but also raise inflation and interest rates, damaging bonds.)

But in this latest period, it seems that demand expectations have been marked lower, raising bond prices substantially, and reducing equity prices somewhat less. It is possible that there has also been a rise in risk aversion in response to today’s French election, North Korean tensions, and the US military raid in Syria. The increase in geopolitical risk perhaps explains why bonds seems to have been affected more than equities:

Apart from geopolitics, several economic developments have come along to cause investors to have doubts about the “reflationary” theme.

First, markets seem to have lost confidence that the US economy is accelerating, let alone showing signs of achieving “escape velocity”. These doubts are probably misplaced.

Admittedly, economic data surprises have been less favorable than they were in 2017 Q1, and there has been little sign that hard data are breaking upwards. However, the Fulcrum nowcasts suggest that US activity has been growing at 3.9 per cent in April, only slightly lower than the 4.5 per cent rates seen in the previous couple of months. Goldman Sachs’ current activity indicators, which track real time growth data using a slightly different methodology, show a similar pattern: growth is down a bit, but it remains very firm.

The well known seasonal adjustment bias in US GDP data may result in the first official estimate Q1 growth rate coming in at only 1.0-1.5 per cent, but a more realistic estimate of the state of the economy is the 2.7 per cent growth rate shown in the New York Fed’s latest nowcast for the quarter. As the seasonal bias is ironed out in Q2 and Q3, it would not be very surprising if the official GDP data jump to above 3 per cent, ending the idea that the US economy is in the doldrums. Meanwhile, the rest of the world economy is now in the midst of an unambiguous and synchronised acceleration, as the IMF cautiously acknowledged this week.

Second, there is the issue of global inflation. Some months ago, I argued that inflation in the advanced economies would move sideways this year, having risen last year as it returned to normal after the commodity price shocks of 2014-16. Global “reflation” would still involve faster growth in nominal GDP, but this would come entirely from the real output component, and not from any further rise in inflation. That assessment seemed to be on course until last month.

However, it did not allow room for any decline in core inflation as the year progressed. Oil and metals prices have dropped in the spring, and that will probably bring headline inflation down for a while. But there would be real concern if core inflation also starts to drop, which is why the the apparently weak inflation data released last week in the US and the Eurozone has come as a nasty surprise.

Fortunately, the official data releases in March have probably been distorted downwards by special factors, including the timing of Easter. The graph below shows the latest Fulcrum estimates of trend inflation in the two regions, adjusted for all seasonal factors and smoothed using the Stock and Watson method. In our view, this is the best method available for assessing underlying inflation in real time. It is clear that there has been little change in core inflation rates in March, and that the official data in the US have been heavily distorted downwards:

We therefore conclude that the incoming economic data have not changed enough in the past couple of months to justify the shift in market behaviour towards what is now known as “reflation off”. (See the FT’s John Authers for more on this view.)

However, the theme will face more severe tests from geopolitics, notably the French Presidential election and Steven Mnuchin’s US tax plans, to be announced next week. Disappointment on either front could upset the apple cart.

0 comments:

Publicar un comentario