International Inflation Cycles Sync Up

Lakshman Achuthan

In the 21st century international inflation cycles have become more synchronized, enabling even earlier detection of cyclical turns in inflation.

Taming Inflation

The behavior of international inflation cycles has changed substantially in the 21st century in terms of the coordination of cyclical timing as well as amplitude. These shifts have made it feasible to devise a long leading index of those inflation cycles that works sequentially with ECRI’s 11 existing international future inflation gauges (FIGs), offering the earliest forecast of cyclical turning points in international inflation.

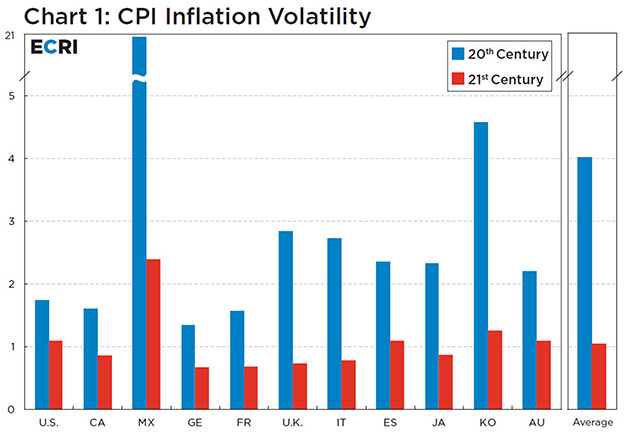

To understand how dramatically the international inflation landscape has changed, we first showcase inflation volatility in the 11 OECD, i.e. rich-country economies, whose inflation cycles are regularly monitored by ECRI (Chart 1). For these economies, we present the five-year moving standard deviation of year-over-year (yoy) CPI growth – a proxy for its volatility – comparing the 20th-century (1969-99) and the 21st-century (2000-17) patterns.

Without exception, it is clear that inflation volatility in all 11 economies has decreased considerably in the 21st century (red bars) from the 20th century (blue bars), with Mexico seeing the greatest drop from the hyperinflationary highs of the 1980s, followed by Korea and the U.K. Across all countries, CPI inflation volatility in the 21st century is, on average, only about a quarter of what it was in the 20th century (rightmost set of bars).

A number of factors are responsible for this plunge in volatility, including the waning power of OPEC – in part resulting in smaller oil shocks – alongside high oil prices incentivizing greater supply, as well as concerted efforts by major central banks to target and curb inflation. Also playing an important role were the disinflationary and deflationary effects of globalization, as China, India and ex-Soviet economies were integrated into the global economy, starting in the late 20th century. As globalization advanced, economies turned much more trade-dependent by the early years of the 21st century (ICO Focus, October 2016), with significant consequences for international inflation cycles, as we shall now detail.

Inflation Cycles Increasingly in Sync

More than a decade ago, we showed that cycles in industrial growth for major economies tend to be more or less synchronized (ICO, October 2006). A key reason for such synchronization has been the growing global interdependence among countries through expanding trade and financial linkages. It therefore makes sense to monitor global industrial growth cycles, and to do so we have employed a set of sequential leading indexes.

We now examine whether there is also a distinct international inflation cycle marked by broadbased cyclical upturns and downturns in inflation rates across different economies.

That is, do economies exhibit similar cyclical patterns in inflation, or do they move independently? If a single international inflation cycle can be identified, monitoring a country’s inflation outlook would entail monitoring both this international inflation cycle and country-specific swings in inflationary pressures.

That is, do economies exhibit similar cyclical patterns in inflation, or do they move independently? If a single international inflation cycle can be identified, monitoring a country’s inflation outlook would entail monitoring both this international inflation cycle and country-specific swings in inflationary pressures.

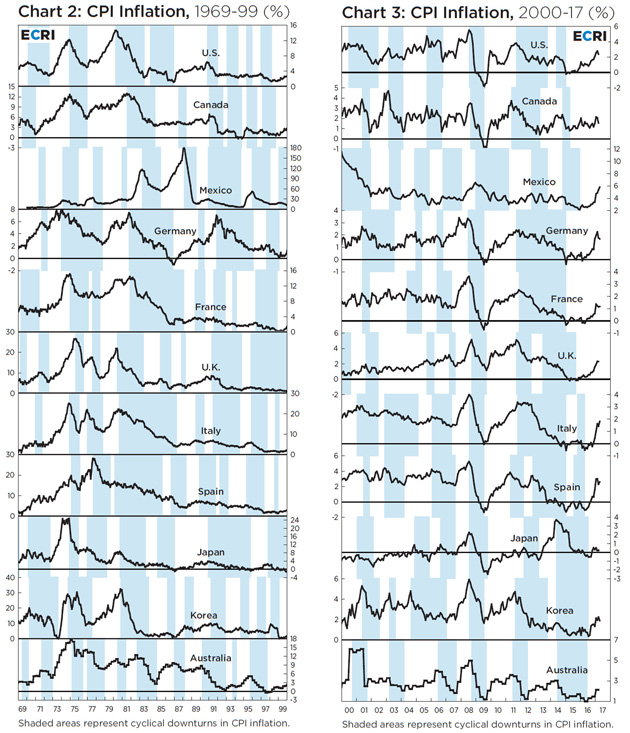

Aligning the yoy CPI growth rates of the 11 economies for which ECRI has developed country-specific FIGs over the two different timespans shown in Charts 2 and 3 offers some visual clues. White areas and blue bars represent cyclical upturns and downturns, respectively, in each country’s CPI growth. The reason for splitting the overall timespan into two periods, namely, 1969-99 and 2000-17, is that the drop in volatility is so sharp that cycles in the 21st century become largely imperceptible when plotted on the scales appropriate for the earlier period.

Comparing the two charts, it is apparent that there is greater alignment of cyclical upturns and downturns in the 21st century than in the 20th century. For instance, in the 30-year period from 1969 to 1999, the 11 economies experienced roughly concurrent inflation cycle downturns only three times, starting in the mid-1970s, early 1980s, and early 1990s (Chart 2). Since 2000, however, these economies have already had four fairly concerted inflation cycle downturns in 17 years – starting around the early 2000s, the mid-2000s, 2008 and 2011 – and are currently all in cyclical upturns (Chart 3).

To objectively measure the degree of synchronization of cyclical upturns and downturns among the 11 economies, we calculated the concordance of cyclical swings, i.e., the proportion of months during which those economies were in simultaneous inflation cycle upturns or downturns. According to this measure, the proportion of time that all 11 economies spent in synchronized upturns or downturns has more than tripled in the 21st century, while the proportion of time that over 80% of the economies were in the same phase of the inflation cycle rose more than 1½ times (not shown).

Predicting International Inflation Cycles

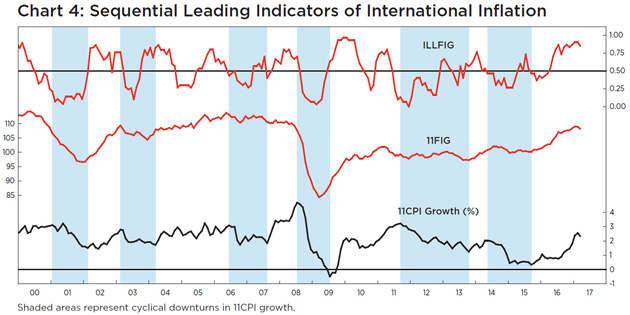

With 21st century inflation cycles across major economies becoming fairly synchronized, it makes sense to define and forecast the resultant international inflation cycle. The international inflation cycle consists of cyclical upswings and downswings in the yoy growth rate of the 11-Country CPI (11CPI), a weighted average of the 11 individual countries’ CPIs (Chart 4, bottom line). Meanwhile, ECRI’s 11-Country Future Inflation Gauge (11FIG, middle line) is constructed in an analogous weighted manner, combining the 11 corresponding future inflation gauges. The 11FIG is a summary measure of underlying inflation pressures across these economies, and leads cyclical turning points in 11CPI growth by a little over one quarter, on average.

Adding to this toolkit, we introduce the International Long Leading Future Inflation Gauge (ILLFIG, top line), designed to be a long leading indicator of the international inflation cycle. The ILLFIG leads the 11FIG by almost one quarter, on average, at cycle turning points, therefore leading the international inflation cycle by a little over half a year, on average. Together, the ILLFIG and the 11FIG serve as a sequential leading indicator system for international inflation cycles, increasing the forecast horizon and enhancing the clarity of the international inflation outlook.

As the chart shows, in the most recent cycle, the ILLFIG and 11FIG turned up in early 2015, signaling with conviction an upcoming cyclical upswing in international inflation pressures. Indeed, 11CPI growth started to turn up, as well, in the fall of 2015. In their latest readings, both indexes remain elevated, though slightly off their recent highs.

With the yo-yo years unfolding as the major developed economies experience long-term declines in secular trend growth (ICO, March 2012), lowflation, and even occasional deflation, has become the norm. Meanwhile, with CPI inflation volatility having dropped markedly, especially in the 21st century, international inflation cycles have become more subdued.

The synchronization of international inflation cycles highlights the importance of global factors in assessing domestic inflation prospects. Our analysis underscores the 21st-century reality that the timing of inflation cycles may be beyond the control of any individual central bank. Yet this very development makes it possible for ECRI to provide even earlier signals of peaks and troughs in the inflation cycle.

Currently, both the ILLFIG and the 11FIG remain in cyclical upturns, and close to multiyear highs. However, they both dipped in their latest readings. As such – and especially in the context of the global industrial growth downturn that is now at hand (ICO Essentials, April 2017) – they bear watching for early signs of a potential reversal in the global reflation cycle that we flagged last summer (ICO Essentials, August 2016).

0 comments:

Publicar un comentario