IMF says debt binge leaves US corporate assets exposed

Global financial stability report warns of risks from US business loans

by: Shawn Donnan and Gemma Tetlow in Washington

A debt binge has left a quarter of US corporate assets vulnerable to a sudden increase in interest rates with the ability of companies to cover interest payments at its weakest since the 2008 financial crisis by one measure, the International Monetary Fund has warned.

The IMF’s twice-yearly Global Financial Stability Report released on Wednesday highlights what economists at the fund see as one of the main risks facing President Donald Trump and his plans to boost US growth via a combination of tax cuts and infrastructure spending.

Although the Republican plans are far from finalised, the IMF’s assumption is that tax cuts will end up adding to both the US deficit and the country’s debt load, predicting it would be as much as 11 percentage points of gross domestic product larger in five years than they forecast a year ago.

But it is the potential impact of those plans on borrowing costs and companies that the IMF also finds concerning.

Mr Trump’s hope is that lower taxes and a reduced regulatory burden will prompt companies to increase investment and hire more workers in the US, leading to stronger growth.

The IMF said there was also another possible scenario, however, in which the administration’s fiscal plans turned out to be economically “unproductive”.

Should Mr Trump’s plans lead to larger US budget deficits and higher inflation it would force the Federal Reserve to raise rates faster than expected. That could lead to a rapid appreciation in the dollar and consequences for emerging economies with as much as $230bn in debt there vulnerable.

But it would also have an impact on the borrowing costs of US companies, which according to the IMF have added $7.8tn in debt and other liabilities since 2010.

.

The problem, according to fund economists, is that already “corporate credit fundamentals [in the US] have started to weaken, creating conditions that have historically preceded a credit cycle downturn”. And by the IMF’s calculations companies with almost $4tn in assets — or 22 per cent of the total US corporate assets — would be “weak” or “vulnerable” to a fiscal expansion that went wrong and led to a sharp rise in borrowing costs.

Viewed as a whole, “the US corporate sector is healthy,” said Tobias Adrian, the IMF’s new financial stability watchdog. But “there is a tail of vulnerable firms in the corporate sector”.

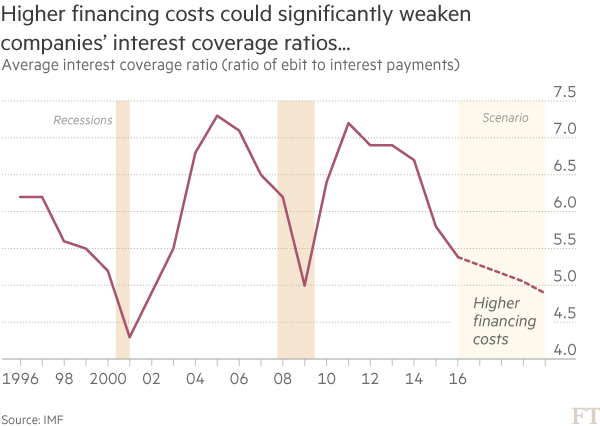

While the absolute level of debt servicing costs as a proportion of income was now low compared with during the global financial crisis other measures were less encouraging. The average interest coverage ratio has fallen sharply over the past two years, the IMF said, with earnings less than six times the cost of interest, a figure “close to the weakest multiple since the onset of the global financial crisis”.

That sort of deterioration has historically corresponded with widening credit spreads for risky corporate debt and been concentrated on smaller companies with less access to capital markets.

But, already, the IMF said, companies accounting for 10 per cent of US corporate assets appear unable to cover the cost of interest payments out of their current earnings.

Many of those companies are in the energy sector and suffering due to the oil price volatility of recent years. “But the proportion of challenged firms has broadened across such other industries as real estate and utilities,” IMF economists wrote.

The warning about the potential US risks came alongside what was otherwise a relatively cheery assessment of the broad state of global financial stability, which the IMF said had been improving since last year.

Besides the possibility of US policy mis-steps the IMF said China’s credit boom continued to pose a major risk to the global economy as authorities there struggled to rein in credit growth, repeating what has increasingly become a regular warning from the fund.

The total assets of China’s banks were three times the size of its GDP, non-bank financial institutions were continuing to lend more and corporate bond issuance had surged in 2016.

“Credit booms this big can be dangerous,” Mr Adrian said. “The longer booms last and the larger credit grows, the more dangerous they become.”

Despite “substantial progress” the IMF said risks also continued to lie in the European bank sector, where “persistently weak profitability is a systemic stability concern”, the IMF said.

0 comments:

Publicar un comentario