Happy returns

America’s big banks have an encouraging first quarter

Uncertainty over the future of regulation still clouds the Outlook

WHAT a difference a year makes. When America’s big banks reported first-quarter earnings for 2016, the mood was glum. The Federal Reserve was proving tardier than hoped in raising interest rates, which held down lending margins. Jitters about the world economy meant rotten results for investment-banking units, in what is usually their best season of the year. Regulators added to the misery: last April the Fed rejected the “living wills”—plans for liquidating lenders that get into trouble—of five of the six largest banks.

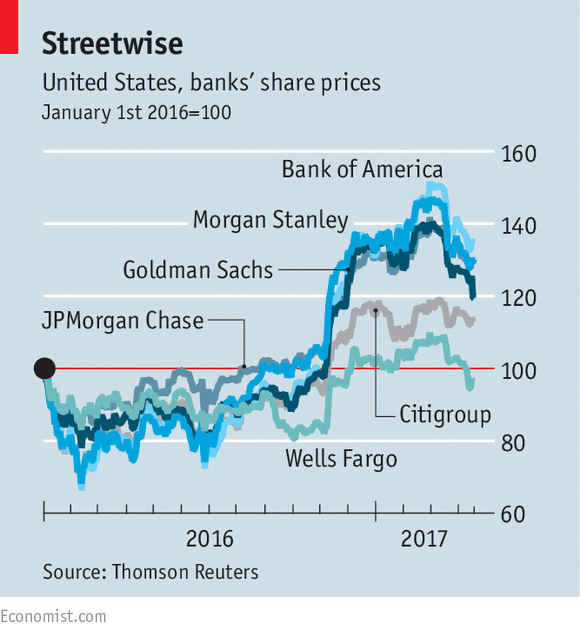

This spring bankers are happier. Business perked up last year after that dismal start. Donald Trump’s election in November, accompanied by promises to ginger up the American economy, cut corporate taxes and roll back regulation of finance, gave banks’ shares a lift (see chart).

The Fed raised rates in December and again in March and is likely to keep increasing them.

And 2017’s first-quarter results have, mostly, seen an improvement—though the cheer was not evenly shared.

Underwriting and fixed-income trading were buoyant; equity trading and advice were flattish. Morgan Stanley, the last big bank to report, was arguably the star turn. On April 19th it said its fixed-income revenues had almost doubled, to $1.7bn, apparently vindicating a thorough overhaul of the division early last year. The firm’s net income rose by 70%, to $1.9bn.

The previous day Goldman Sachs had disappointed analysts, although its net income was twice as high as a year before. Its fixed-income, currency and commodities revenues were flat, also at $1.7bn. It also lagged behind the field in equities. Volatility in the foreign-exchange, crude-oil and equity markets was subdued: hedge funds (on which Goldman’s trading business is more reliant than its rivals) were consequently less active. Even so, admitted Goldman’s Martin Chavez, “we didn’t navigate the market well”.

Business on Main Street was more sluggish. Bank loans grew in the first quarter by just 0.7% at an annualised rate, according to the Fed, the slowest for almost six years. Commercial and industrial lending shrank for the first time since late 2010. Residential-mortgage lending also declined. But widening interest margins helped some banks, as loan rates went up faster than funding costs: Bank of America’s spread rose by 18 basis points from the previous quarter and JPMorgan Chase’s by ten.

In such a quarter Wells Fargo, the least dependent of the big six on investment banking, was perhaps the least likely to shine. Its net income, at $5.5bn, was virtually unchanged from a year before and a shade up from the fourth quarter. A quarterly increase in commercial lending was outweighed by a decline in consumer loans, mainly mortgages.

But Wells has other worries. It is still recovering from last September’s revelation that it had opened more than 2m ghost accounts. It hopes that a scathing report this month by outside consultants, the dismissal of several executives and the clawing back from them of $180m in pay and shares will help it to recover customers’ trust. It has some way to go: the number of current (checking) accounts opened in March was up by 7% from February, but 35% lower than a year before. Institutional Shareholder Services, a firm which advises investors, has recommended voting to replace most of Wells’s board at the annual meeting on April 25th.

Wells’s woes notwithstanding, banks ought to be able to look ahead in good heart. Rates are likely to rise further, America’s economy is in good shape and Wall Street firms stand to gain as Europe picks up too. But a cheerful year is by no means assured. Mr Trump’s tax-cutting plans are not yet formed and the future of bank regulation is still unclear. Hence the stalling, in recent weeks, of the rally in banks’ shares.

Bankers have argued that it is high time red tape was cut: lending, they say, is being held back.

Mr Trump is due to appoint several regulators who may lift their burden. But his chief economic adviser, Gary Cohn, formerly at Goldman Sachs, has mused vaguely about a “21st-century version” of the Glass-Steagall act, the Depression-era law that separated commercial and investment banking, repealed only in 1999. With no details, bank bosses were coy in earnings calls with analysts, but “Glass” and “Steagall” are not soothing words.

0 comments:

Publicar un comentario