Why Do We Own Gold?

by: Chris

- A suitable store of value.

- A potential hedge against the frailties of the global monetary system.

- A potentially undervalued asset?

- A potential hedge against the frailties of the global monetary system.

- A potentially undervalued asset?

Why do we own gold?

In this short memo (written on March 10th, 2017), we would like to present our reasoning for including gold to our overall asset allocation.

1. A suitable store of value

In a piece of research entitled Of The Evolution Of The Global Monetary System that we wrote in June 2016, we recounted that for the vast majority of human economic history spanning thousands of years, gold and silver coins were the most commonly used form of money (please reach out to us if you'd like to read this memo). They fulfilled all of the generally accepted conditions for something to be suitable as 'money,' namely i.) a store of value, ii.) a unit of account, and iii.) a medium of exchange.

Perhaps the most important of these conditions is the first one: a store of value. This means that whatever we choose to use as money - be it silver, gold, or simply paper currency accepted as a legal tender of debts and backed by the faith and credit of a sovereign government - it must preserve its purchasing power over time. The phenomenon that hinders this from occurring is inflation, or the gradual depreciation of currency relative to the value of what it can purchase in the real economy. From the perspective of individual economic actors, this phenomenon is more easily observable as a persistent increase in the price of goods and services.

Ensuring price stability is one of the foundations of a sound and stable capitalistic system. It protects savings from confiscation through inflation; and thus fosters capital formation, which is a key driver of economic development. While most economic textbooks typically associate inflation with brisk demand or surging input costs, by far the most significant cause of inflation is expanding the money supply at a faster rate than what is consistent with the size and growth potential of an economy. It can also be argued that such unwise monetary policies play a major part in creating long-term business cycles via credit booms and subsequent busts, which often lead to recession or even depressions.

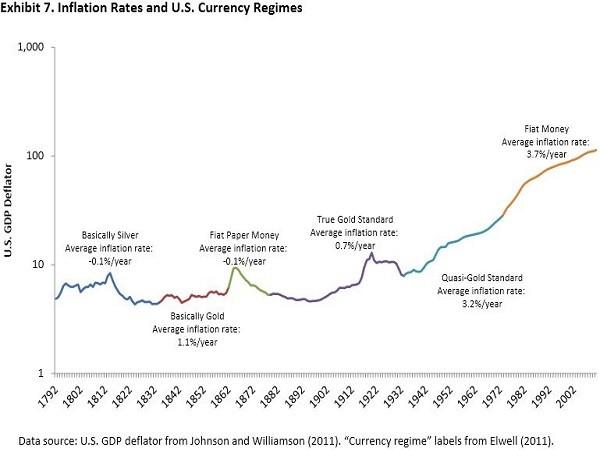

Our long-term track record of managing price stability under various monetary systems paints an unequivocal picture. As shown in Figure 1 below, inflation in the US averaged about 0% to 1% per annum between 1792 and the early 1930s, a 140-year period that coincides with silver- and gold-based monetary systems, bar for a brief period during the American Civil War.

By contrast, from the early 1930s onwards, as the US started to expand its money supply at a much faster rate than previously, the average inflation rate picked up to about 3% p.a. Then, following the closing of the 'gold window' in 1971, at which point US dollars were no longer redeemable in gold at all, monetary expansion accelerated further and inflation picked up closer to the 4% p.a. mark. Just to put this into mathematical context: the power of compounding works both ways, and it only takes 18 years for a currency depreciating at 4% p.a. to lose half of its value!

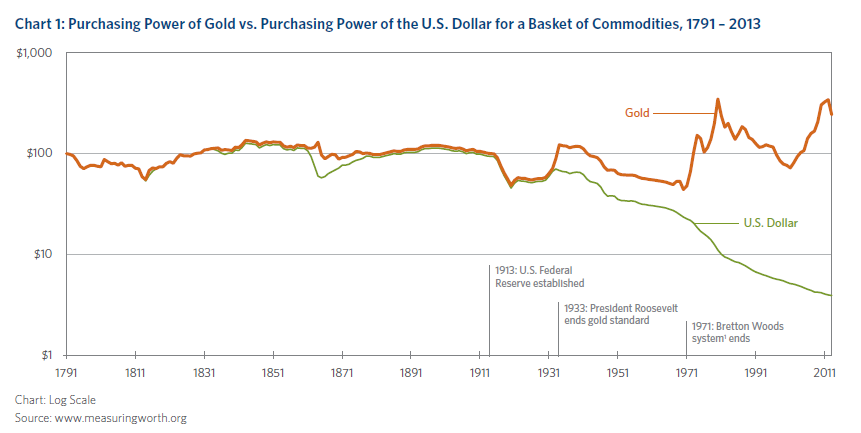

Figure 2 below essentially depicts the exact same information, but presented as the purchasing power of gold and the US$ for a given basket of commodities between 1791 and 2013. It shows a clear inflection point when the US first devalued, and then eventually completely broke off the relationship between the dollar and gold, as well as the impact this had on their respective ability to act as an adequate store of value. While gold has basically maintained a steady purchasing power, the dollar has lost over 98% of its original purchasing power over that 220+ year period.

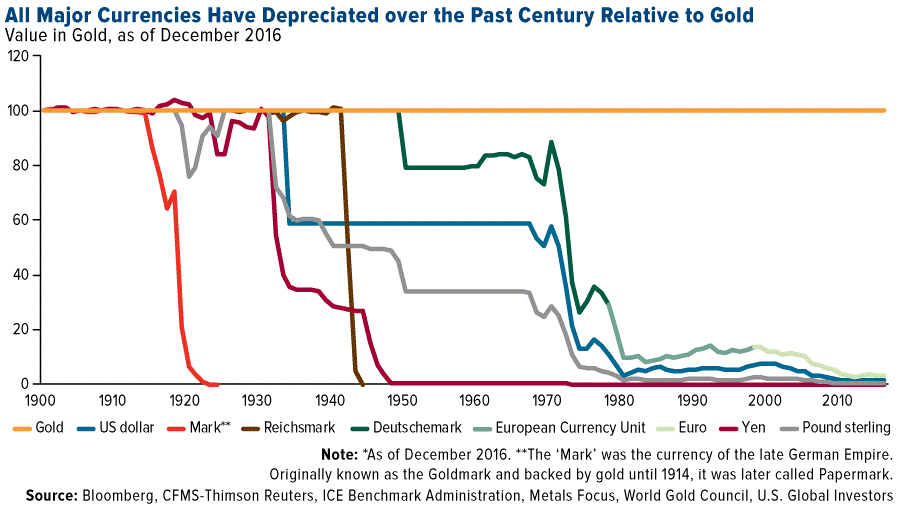

So, to sum up: on the one hand, we have precious metals like gold that have a track record spanning centuries of acting as an adequate store of value; and on the other hand, we have every single man-made currency without exception that has lost nearly all of its purchasing power over the long term (as shown in Figure 3 below). If you'd have to explain this to a 5-year old child, you'd probably say something along the lines of: 'when you create a large amount of money out of thin air, you can't expect it to keep its value over time. Gold can't be created out of thin air.'

Prudent financial planning recommends that a portion of our wealth should be held in reserve, as a safety net to protect us against hard times and unexpected events. Given its vastly superior ability to store value over time relative to paper currency, it appears obvious to us a portion of our long-term reserves should be held in physical gold.

2. A potential hedge against the frailties of the global monetary system

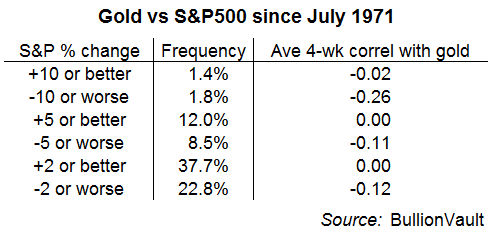

We've previously described the manner in which gold is a very effective hedge against inflation relative to paper currencies. But beyond that, does it also offer a potential source of downside protection against various asset classes? As shown in Figure 4 below, gold is essentially uncorrelated to stock returns, but does offer a small downside protection when stock prices drop significantly. Similarly, gold is largely uncorrelated to bond prices, although a small positive relationship can sometimes be observed during times of financial distress, as both are considered as a 'safe haven' asset. So, generally speaking, gold offers a source of uncorrelated returns, which at the very least can be beneficial as a 'portfolio diversifier' that reduces volatility in an overall asset allocation.

.

The main potential hedge that we believe gold offers is against the frailties of the global monetary system. As described at length in our Annual Report 2016, the extremely expansionary monetary policies of central banks over the past decades, and particularly since the financial crisis of 2008, have facilitated a rapid accumulation of debt to a clearly unsustainable level.

As long as creditors are confident in governments' ability to honour their long-term financial obligations, and not devalue their currencies or pursue monetary policies that may lead to a high level of inflation in doing so, then the current global monetary system may perpetuate itself for many decades still. But let's be absolutely honest with ourselves: it is the very definition of a 'confidence game.'

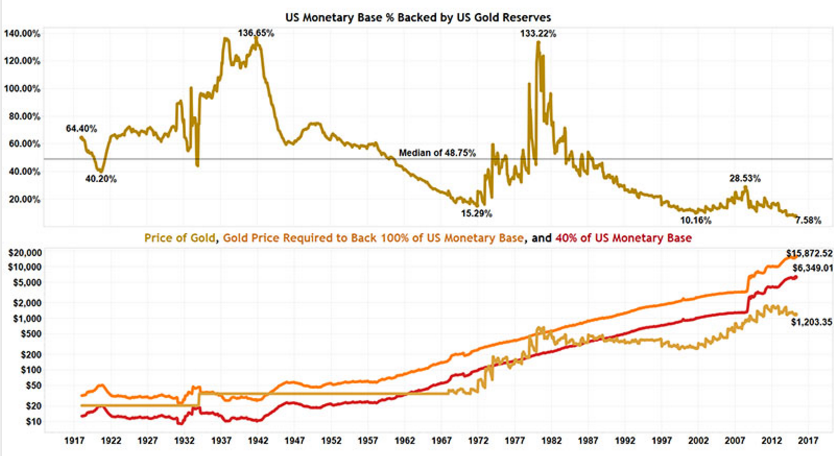

Let's put this into the appropriate context in order to illustrate how fragile this confidence really is. We've previously described how currency used to be 100% backed by gold[1]. Figure 5 below illustrates the physical gold coverage of the US monetary base between 1918 and 2016.

Note that this ratio is not only impacted by the amount of gold reserves held, but also largely by the price of gold, so it can be quite volatile. A long-term trend is nonetheless clearly apparent: gold reserves as a % of the monetary base have steadily fallen to an all-time low of 7.5% vs. a median of nearly 50%.

Today's monetary base in the US is slightly less than $3.8 trillion, compared to gold reserves of $315 billion at today's gold price. That's a multiple of 12x.

.

Source: National Inflation Association (2017)

The proportions get even more absurd when one considers the total credit that is extended to both the public and private sector on the back of this monetary base. In the US, total credit is a staggering US63.4 trillion in 2016. That's 17x times the monetary base, and over 200x the US gold reserves backing that monetary base! And that's just within the US. On top of that, the Bank of International Settlements estimates that there is approx. $9.7 trillion in dollar-denominated debt outside of the US at the end of 2015.

Bottom line: if everybody suddenly decided to collect the debts they owned at the same time, there would not nearly be enough dollars to go around, let alone enough gold.

Now, remember that this debt is supposedly backed by the full faith and credit of sovereign governments. And yet every serious economist out there is telling us that most governments in both Western and emerging nations are on a clear path to insolvency and bankruptcy, unless they enact major structural economic reforms. So, it's anyone's guess how long will this confidence last...

Historically, during times of credit crises and financial distress, gold has been considered as the ultimate 'safe haven,' and its price has spiked. We believe it will continue to behave in such a way, making it an adequate hedge against a loss of confidence in the world monetary system.

And for those asking themselves 'what's the likelihood of that happening?' remember that what we're talking about here is far from unprecedented. Since the end of the Classical Gold Standard in 1914, we've altered our global monetary arrangements a number of times, typically every couple of decades.

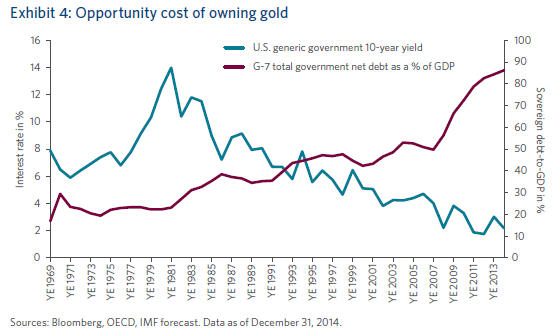

We view a position in gold as an insurance policy against such an event, rather than as an absolute return investment or trading opportunity. Remains the question of whether this represents a cost-effective insurance policy as of today. We believe that the current opportunity cost of owning gold is relatively low, as both the yields on paper assets such as sovereign debt and the credit worthiness of that debt, as measured by debt to GDP, are at very low levels (as shown in Figure 6 below).

3. A potentially undervalued asset?

This claim is by far the hardest to establish. How does one value the intrinsic worth of a commodity that isn't a really productive asset, and therefore doesn't offer either a yield or the prospect of capital appreciation?

The most appropriate way that we can think of is based on the basic principle of supply and demand: or the existing stock of gold above (and to a lesser extent below) ground, and the demand for that stock.

The supply side is the easiest to deal with: we know with some level of reliability that the total amount of gold ever mined amounts to about 186'700 tons in 2016, according to the World Gold Council. And the US Geological Survey estimates that proven global reserves below ground amount to some 52'000 tons. To put this into perspective, this represents about 0.8 ounce per person of gold above ground (about 1.0 ounce per person of gold above and below ground). In short, on a per capita basis, there is not a lot of gold to go around! Furthermore, due to declining ore grades, gold production is expected to have peaked in recent years, at slightly over 3'000 tons per year. Scarp gold is another important source of supply, representing about 1/4th of total supply, or over 1'000 tons per year.

What about the demand side? According to a primer on gold by Bank of America - Merrill Lynch dated June 2015, jewelry demand accounts for over 2'000 tons per year, or about half of total demand, with India and China as the largest buyers. Other fabrication uses (electronic, industrial, and dental applications) add another 500 tons. Investment demand, both from the private sector and central banks, makes up the rest, or some 1'500 tons per year. It is worth noting that an increasing amount of gold's investment demand is now supplied by collective investment vehicles, such as gold exchange-traded funds (ETFs). As briefly discussed later, this is a very different proposition from actually owning the tangible commodity, which suffers from many drawbacks.

How does all of this fit into our evaluation of gold's intrinsic worth? As a first indication, we can consider that a commodity for which supply and demand are balanced should trade around its marginal cost of production, which is about $700 per ounce for gold (the 'all-in sustaining cost' is likely to be higher than that figure). We believe this represents a strong long-term floor for gold prices. We also believe that given the monetary imbalances described earlier, it would only take a small crisis of confidence for the investment demand in gold to skyrocket.

Again, let's try to put this into an appropriate context. At today's price, the total amount of gold ever mined represents a monetary value of about $6.6 trillion. By contrast, global institutional pension fund assets in major markets amounted to over $36 trillion in 2016, according to the latest figures by Willis Towers Watson. There's another $7.4 trillion in sovereign wealth funds' assets globally. If both of these heavy-weight categories of investors decided to attribute even just 1% of their total asset allocation to gold, that would represent a demand of over 12'000 tons at today's price. That's about 4x the global annual output, and 1/15th of the total amount of gold that we've ever mined!

Let's consider a somewhat more realistic hypothetical scenario: if the US were to back its monetary base, as used to be the case during the Gold Standard, say to the tune of about 40%, it would require a gold price of over $6'000 per ounce given its current physical gold reserves.

It seems quite obvious to us that any move, even small, in perception regarding the role of gold in the global monetary system would result in a manifold increase in the price of gold, in the 5-10x range.

On the other hand, downside risk in the long term is likely limited to the gold price falling towards its cost of production, or some 40%. Having said all of that, we state again that generating an absolute return is not the primary objective of having an allocation to gold.

4. Gold as part of an overall asset allocation

We've aimed to briefly outline our rationale for considering gold as part of an overall asset allocation given today's investment landscape. It is based on gold being i.) a suitable store of value over the long term, ii.) an effective hedge against a confidence crisis in our fragile global monetary system, and iii.) the large upside potential in the price of gold should that happen.

How much of total assets should we allocate to gold? Our recommendation is for an allocation of approx. 4%, with a discretionary potential to deviate +/- 2% depending on the investment and monetary landscape, as well as the price of gold.

This target allocation can be supported by a number of arguments. First, we've demonstrated the manner in which gold is an effective way to store wealth while protecting it from inflation.

Our gold allocation should, therefore, cover a portion of our long-term cash reserves. Second, we've argued that gold is an effective hedge against a fragile global monetary system. We believe that for any unlevered hedge to be effective, it should represent at least close to 5% of a total asset allocation. Anything less will simply not have the desired impact to overall investment results.

We recommend that the vast majority of the gold allocation should consist of physical gold, either in kilos or ounces, stored at a safe counterparty, and deliverable on demand.

We are very skeptical of 'paper gold' investments such as ETFs, for a number of reasons. First, because there is a huge difference between owning gold as a financial instrument vs. gold as a tangible commodity. As the main reason to own gold is to protect oneself against a potentially unstable monetary system, to take out such an insurance policy in the form of a financial instrument defeats the purpose. Second, one must consider the counterparty risk. For example, take the SPDR Gold Trust (NYSEARCA:GLD), which is the world's largest gold ETF. Its underlying custodian is HSBC, a bank that we consider to be far from a safe custodian in case of pronounced financial turmoil. Last comes the issue of the gold being deliverable on demand.

Again, sticking with our example of the SPDR Gold Trust, the prospectus states that you must own at least 100'000 shares to be eligible for physical gold delivery, which represents an investment of about $11.5m at today's price. What a joke! Basically, this sentence strongly suggests that their ETF is not 100% backed by physical gold. If there ever comes a point when people feel that it is no longer sufficient to own 'paper gold' in the form of an ETF, but that they rather want to own the actual physical commodity, then we may all wake up to the harsh reality that there are many, many financial claims on gold out there that aren't effectively backed by the physical commodity.

The only other form of gold investments that we recommend is gold mining companies located in developed economies and 'relatively safe' developing countries, such as Canada, Australia, the US, and South America. While gold above ground is the safest way to own physical gold, and investing in gold miners entails some additional risk related to mining activities, it also offers a number of advantages. First, it occasionally offers the opportunity to buy gold 'at a discount.' Because the spot price of gold generally exceeds the cost of extracting it, the valuation of gold mining companies with proven reserves can sometimes be at a discount to the price of gold, even after accounting for the cost of extraction. Second, established gold miners often pay out a dividend, which effectively represents ownership of proven gold reserves with a yield.

Third, gold miners offer a way to build some leverage to a physical gold position in a simple, clean, and cost-effective way. Historically, gold stocks are leveraged 2-3x to the price of gold bullion.

We recommend that the proportion of physical gold to gold mining companies in our overall asset allocation be approximately 80% to 20%.

5. Closing quotes

In closing, we want to reassure readers that we aren't completely crazy to advocate for a position in a shiny yellow metal that has no uses, doesn't yield anything, or offer the prospect of capital appreciation. To do so, we've included a number of famous quotes on the topic of inflation and the monetary system below:

'By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens.'

- John Maynard Keynes

'Inflation is the one form of taxation that can be imposed without legislation.'

- Milton Friedman

'In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. There is no safe store of value.'

- Alan Greenspan

'In reality there is no such thing as an inflation of prices, relatively to gold. There is such a thing as a depreciated paper currency.'

- Lysander Spooner

'The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.'

- Ernest Hemingway

'It is well enough that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning.'

- Henry Ford

'The 'boom-bust' cycle is generated by monetary intervention in the market, specifically bank credit expansion to business.'

- Murray Rothbard

'Give me control of a nation's money supply, and I care not who makes its laws.'

- Amschel Rothschild

'He who controls the money supply of a nation controls the nation.'

- James A. Garfield

'A system of capitalism presumes sound money, not fiat money manipulated by a central bank. Capitalism cherishes voluntary contracts and interest rates that are determined by savings, not credit creation by a central bank.'

- Ron Paul

[1] This is in the theoretical sense of the term, in that currency was fully redeemable in gold on demand, although still subject to the practice of fractional reserve banking, which meant that the actual coverage was always substantially below 100%.

0 comments:

Publicar un comentario