Up, up and away

As the Fed raises rates, Janet Yellen’s legacy is pondered

Donald Trump has the chance to mould America’s central bank

THIRD time lucky. In each of the past two years, the Federal Reserve has predicted multiple interest-rate rises, only to be thrown off-course by events. On March 15th the central bank raised its benchmark Federal Funds rate for the third time since the financial crisis, to a range of 0.75-1%. This was, if anything, ahead of its forecast, which it reaffirmed, that rates would rise three times in 2017.

“Lift-off” is at last an apt metaphor for monetary policy. But as Janet Yellen, the Fed’s chairwoman, picks up speed in terms of policy, she must navigate a cloudy political outlook. The next year will define her legacy.

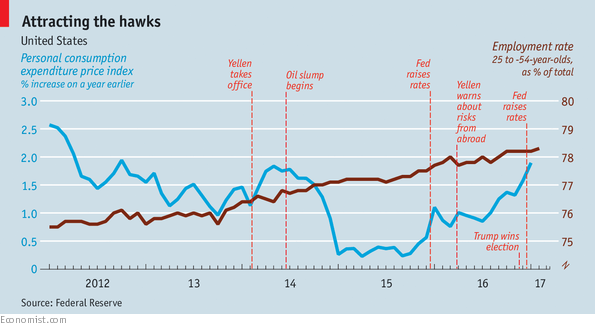

Ms Yellen took office in February 2014 after dithering by the Obama administration over a choice between her and Larry Summers, a former treasury secretary. Left-wingers preferred Ms Yellen, in part because she seemed more likely to give jobs priority over stable prices. Indeed, Republicans in Congress worried that she would be too soft on inflation. The Economist called her the “first acknowledged dove” to lead the central bank.

Today Ms Yellen looks more hawkish—certainly than Mr Summers, who regularly urges the Fed to keep rates low. Headline inflation has risen to 1.9% a year; but excluding volatile food and energy prices it is a bit stuck, at around 1.7%. Yet Ms Yellen has not really changed her plumage. As expected, she has consistently given high weight to unemployment. Before her appointment, when joblessness was high, she wanted the Fed to promise to keep rates low for longer than it then planned. Now that unemployment is just 4.7%, she is keener to raise rates than those who worry about stubbornly low inflation.

In March 2015 Ms Yellen argued that, were the Fed to ignore a tight labour market, inflation would eventually overshoot its 2% target. The Fed might then need to raise rates sharply to bring it back down, risking a recession—and hence more unemployment. Better to lift rates in advance.

Unemployment, however, was already down to 5.5%. So most rate-setters had started 2015 forecasting a rapid lift-off, taking rates up by at least one percentage point over the year. But inflation remained strangely tepid (see chart). Cheap oil and a strong dollar were partly to blame. But wages also seemed stuck. Ms Yellen and her colleagues deduced that unemployment could safely fall a bit further.

In the end, they raised rates once in 2015, in December. Again, they forecast four rate rises for the next year. This time they were delayed by worries over the global economy (China wobbled early in 2016). Officials also began to see lower rates as a permanent feature of the economy.

Today, the setters think rates will eventually stabilise at 3%, down from a forecast of 4% when Ms Yellen took office.

Ms Yellen’s Fed, then, has proved very willing to change course. And this time the Fed is speeding up, rather than postponing, rate rises. Three factors are at play. First, the global economy has been reflating since the middle of 2016. Second, financial markets are booming, boosting the economy by almost as much as three interest-rate cuts, by some estimates. Third, a fiscal stimulus is looming.

According to the Fed’s model, a tax cut worth 1% of GDP would push up interest rates by nearly half a percentage point. During his campaign Donald Trump promised cuts worth nearly 3% of GDP, according to the Tax Policy Centre, a think-tank.

Doves insist that the Fed risks halting an incomplete recovery. Before the crisis of 2007-08, about 80% of 25-to 54-year-olds (the “prime age” population) had jobs. Today the proportion is 78%. The difference is about 2.5m potential workers, mostly not counted as unemployed because they are not looking for work. Were the Fed to aim for the nearly 82% prime-age employment seen in April 2000, the jobs shortfall would look twice as high.

In October Ms Yellen wondered aloud whether a “high-pressure economy”, and a resulting wage boom, might coax more people to seek work. This led to reports—soon corrected—that she would let the economy overheat after all. In fact Ms Yellen has long warned that many drivers of labour-force participation are beyond the central bank’s control. A gentle pickup in wage growth since mid-2015 seems to support her view that unemployment is the best measure of economic slack.

Rarely has unemployment been this low without inflation taking off. Once was in the late 1990s, when Alan Greenspan, a former Fed chairman, correctly predicted that rising productivity would stop a booming labour market from stoking inflation. Jeffrey Lacker, chairman of the Richmond Fed, recently offered another example. In 1965 unemployment fell to 4%, while inflation was only 1.5%.

Yet prices took off in the years that followed: by 1968, inflation had reached 4.3%.

That is what Ms Yellen wants to avoid. But the Fed has not often managed to tighten monetary policy without an ensuing recession. Should she manage it, her tenure will go down as a great success.

That is, if she has time to finish the job. Her term ends in February 2018. If Mr Trump replaces her, she could stay on as a board member. But she would probably leave. So would Stanley Fischer, the Fed’s vice-chairman, whose term expires four months later. Two of the Fed’s seven seats are already vacant, and Daniel Tarullo, the de facto vice-chairman for regulation, goes in April. So Mr Trump may be able to appoint five governors, including the chairman, within 18 months of taking office.

What then for monetary policy, and for Ms Yellen’s legacy? During his campaign, the president attacked the Fed for keeping rates low and said he would replace Ms Yellen with a Republican.

Mooted successors include Glenn Hubbard, who advised George W. Bush; Kevin Warsh, a former banker and Fed governor; and John Taylor, an academic and author of a rule, named after him, for setting interest rates.

All these potential successors are monetary-policy hawks. Some versions of the Taylor rule, for example, call for interest rates more than three times as high as today’s. Mr Trump, who promises revival and 3.5-4% economic growth, might not like the sound of that. If, like most populists, he wants to avoid tight money, he could appoint someone malleable to the Fed. But that would also be risky. One cause of the inflationary surge of the 1960s, notes Mr Lacker, was political pressure to keep policy loose even after ill-timed tax cuts. On one occasion, President Lyndon Johnson summoned the Fed chairman, William McChesney Martin, to berate him for raising interest rates (and to drive him around his ranch at breakneck speed).

A simpler way to keep hawkish Republicans at bay would be to reappoint Ms Yellen. With Mr Tarullo out of the frame, Mr Trump would still be able to impose his deregulatory agenda, yet keep faith with Ms Yellen to set monetary policy. Senators would struggle to come up with reasons not to reappoint a central-bank chairwoman so close to achieving her goals. Bill Clinton and Barack Obama reappointed incumbent Republican chairmen. It might be in Mr Trump’s interest to reciprocate.

“Lift-off” is at last an apt metaphor for monetary policy. But as Janet Yellen, the Fed’s chairwoman, picks up speed in terms of policy, she must navigate a cloudy political outlook. The next year will define her legacy.

Ms Yellen took office in February 2014 after dithering by the Obama administration over a choice between her and Larry Summers, a former treasury secretary. Left-wingers preferred Ms Yellen, in part because she seemed more likely to give jobs priority over stable prices. Indeed, Republicans in Congress worried that she would be too soft on inflation. The Economist called her the “first acknowledged dove” to lead the central bank.

Today Ms Yellen looks more hawkish—certainly than Mr Summers, who regularly urges the Fed to keep rates low. Headline inflation has risen to 1.9% a year; but excluding volatile food and energy prices it is a bit stuck, at around 1.7%. Yet Ms Yellen has not really changed her plumage. As expected, she has consistently given high weight to unemployment. Before her appointment, when joblessness was high, she wanted the Fed to promise to keep rates low for longer than it then planned. Now that unemployment is just 4.7%, she is keener to raise rates than those who worry about stubbornly low inflation.

In March 2015 Ms Yellen argued that, were the Fed to ignore a tight labour market, inflation would eventually overshoot its 2% target. The Fed might then need to raise rates sharply to bring it back down, risking a recession—and hence more unemployment. Better to lift rates in advance.

Unemployment, however, was already down to 5.5%. So most rate-setters had started 2015 forecasting a rapid lift-off, taking rates up by at least one percentage point over the year. But inflation remained strangely tepid (see chart). Cheap oil and a strong dollar were partly to blame. But wages also seemed stuck. Ms Yellen and her colleagues deduced that unemployment could safely fall a bit further.

In the end, they raised rates once in 2015, in December. Again, they forecast four rate rises for the next year. This time they were delayed by worries over the global economy (China wobbled early in 2016). Officials also began to see lower rates as a permanent feature of the economy.

Today, the setters think rates will eventually stabilise at 3%, down from a forecast of 4% when Ms Yellen took office.

Ms Yellen’s Fed, then, has proved very willing to change course. And this time the Fed is speeding up, rather than postponing, rate rises. Three factors are at play. First, the global economy has been reflating since the middle of 2016. Second, financial markets are booming, boosting the economy by almost as much as three interest-rate cuts, by some estimates. Third, a fiscal stimulus is looming.

According to the Fed’s model, a tax cut worth 1% of GDP would push up interest rates by nearly half a percentage point. During his campaign Donald Trump promised cuts worth nearly 3% of GDP, according to the Tax Policy Centre, a think-tank.

Doves insist that the Fed risks halting an incomplete recovery. Before the crisis of 2007-08, about 80% of 25-to 54-year-olds (the “prime age” population) had jobs. Today the proportion is 78%. The difference is about 2.5m potential workers, mostly not counted as unemployed because they are not looking for work. Were the Fed to aim for the nearly 82% prime-age employment seen in April 2000, the jobs shortfall would look twice as high.

Rarely has unemployment been this low without inflation taking off. Once was in the late 1990s, when Alan Greenspan, a former Fed chairman, correctly predicted that rising productivity would stop a booming labour market from stoking inflation. Jeffrey Lacker, chairman of the Richmond Fed, recently offered another example. In 1965 unemployment fell to 4%, while inflation was only 1.5%.

Yet prices took off in the years that followed: by 1968, inflation had reached 4.3%.

That is what Ms Yellen wants to avoid. But the Fed has not often managed to tighten monetary policy without an ensuing recession. Should she manage it, her tenure will go down as a great success.

That is, if she has time to finish the job. Her term ends in February 2018. If Mr Trump replaces her, she could stay on as a board member. But she would probably leave. So would Stanley Fischer, the Fed’s vice-chairman, whose term expires four months later. Two of the Fed’s seven seats are already vacant, and Daniel Tarullo, the de facto vice-chairman for regulation, goes in April. So Mr Trump may be able to appoint five governors, including the chairman, within 18 months of taking office.

What then for monetary policy, and for Ms Yellen’s legacy? During his campaign, the president attacked the Fed for keeping rates low and said he would replace Ms Yellen with a Republican.

Mooted successors include Glenn Hubbard, who advised George W. Bush; Kevin Warsh, a former banker and Fed governor; and John Taylor, an academic and author of a rule, named after him, for setting interest rates.

A kettle of hawks

A simpler way to keep hawkish Republicans at bay would be to reappoint Ms Yellen. With Mr Tarullo out of the frame, Mr Trump would still be able to impose his deregulatory agenda, yet keep faith with Ms Yellen to set monetary policy. Senators would struggle to come up with reasons not to reappoint a central-bank chairwoman so close to achieving her goals. Bill Clinton and Barack Obama reappointed incumbent Republican chairmen. It might be in Mr Trump’s interest to reciprocate.

0 comments:

Publicar un comentario