Buttonwood

The unusual gap between American and European bond yields

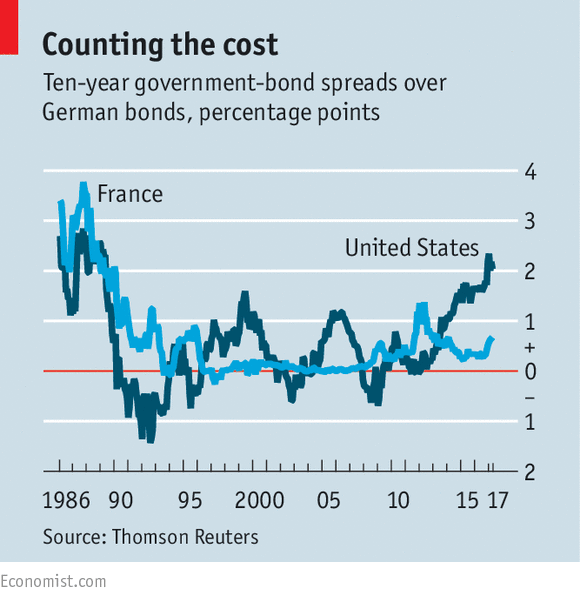

America has the world’s largest economy and a strong currency, yet it costs its government more to borrow than Italy’s

The gap between American and German ten-year yields has been above two percentage points. For much of the past 25 years, it was very rare for the difference to exceed a single percentage point. On occasions, American yields fell below German levels (see chart).

Instead, the gap may reflect differences in both monetary and fiscal policy. In America the Federal Reserve stopped buying Treasury bonds a while ago and has raised interest rates three times since December 2015; the European Central Bank (ECB) is still buying bonds as part of its “quantitative easing” programme, and pays a negative rate on deposits. The Trump administration is committed to tax cuts and infrastructure spending that would increase the budget deficit and require more bond issuance. The euro zone has no plans of this sort for fiscal stimulus.

The present divergence recalls that between American and Japanese bond yields. The latter have been consistently low for much of the past 20 years, as the Japanese economy became mired in slow growth and deflation. Perhaps investors expect the euro zone to get stuck in a deflationary quicksand as the American economy returns to more robust growth.

But that view does not show up in inflation expectations. An oft-used measure, derived from the bond market, is known as the “five year/five-year forward rate”. At the moment this gauge is showing the market forecast for the average inflation rate in 2022-27. In America the forecast is around 2.1%; in the euro zone it is around 1.7%. Six months ago the forecasts were 1.68% and 1.34%. Both have risen a little, but the gap has not widened significantly.

Although few people think Ms Le Pen will actually become president, investors have been burned by last year’s voting upsets. So there has been a tendency to opt for the safest bonds in the euro zone—those issued by the German government. The spread between French and German ten-year yields is more than double its level on October 28th.

Another factor may be the actions of institutional investors. In a recent speech Hyun Song Shin of the Bank for International Settlements (BIS), an organisation of central banks, pointed out that both life-insurance companies and pension funds tend to have long-dated liabilities, ie, claims they must meet over many decades. They try to match those liabilities by buying government bonds. Accounting and regulatory rules often require them to use long-dated bond yields to calculate their liabilities.

But there is a mismatch: the liabilities of these companies and funds tend to be longer-dated than the bonds they hold. So when long-dated bond yields fall, their financial position deteriorates. That means they need to buy more bonds. This drives prices up—and yields further down, making the problem even worse. The BIS says euro-zone insurance companies accounted for 40% of the net purchases of the region’s government’s bonds in 2014. American pension funds and insurers own around $1.7trn of Treasury bonds (out of more than $14trn owned by the public), but seem to play a less substantial role in setting yields than European institutions.

The trend may change again, of course. Kit Juckes of Société Générale, a French bank, says the factors that have widened the spread between American and German yields may start to dissipate.

Political worries may subside if Ms Le Pen doesn’t win; the ECB may scale back its monetary easing; Mr Trump’s stimulus plans may be delayed, or watered down. Whatever else history teaches us, it does not suggest that German ten-year yields of 0.41% will turn out to be a bargain.

0 comments:

Publicar un comentario