Buttonwood

Stockmarkets give up some of their Trump bump

The president’s promises look less plausible; his threats more menacing..

.

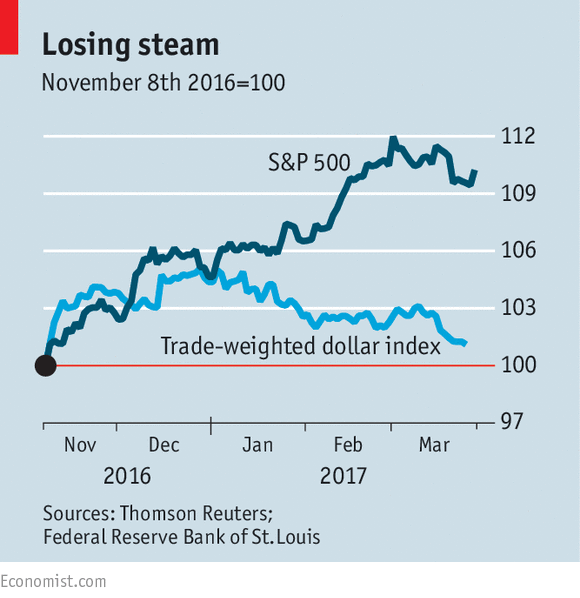

HONEYMOONS don’t last for ever. Having been a reluctant bride to President Donald Trump when courted in the run-up to November’s election, the American stockmarket quickly melted into a mood of romantic euphoria. Shares rose by 12% between election day and March 1st (see chart). But in recent days, sentiment has dimmed. There is talk of the “Trump-disappointment trade”.

For the markets to experience some kind of sell-off is hardly a surprise. The S&P 500 index had gone more than 100 days without a 1% decline, the longest such streak since 1995. And the setback should not be exaggerated. The S&P 500 remains well above its pre-election level, compared with the dollar, which has given up around half its gains. The ten-year Treasury-bond yield, which hit 2.62% on March 13th, has dropped back to 2.38%.

On its own this change of mood made investors look naive. Mr Trump came to office as a political neophyte with a reputation for being sketchy on policy detail. His differences with the congressional Republican Party were made clear throughout the campaign. No one should have expected a smooth roll-out of policy. Nor is a lower corporate-tax rate a sure route to growth.

Britain has cut its marginal rate from 28% to 20% since 2010, without sparking a runaway boom.

In any case, given the lengthy negotiations needed to create a tax package, and the inevitable lag before the policy has an effect on the economy, it would probably be 2018 before the impact of a fiscal stimulus became clear. And if any pickup in growth is delayed, then the Federal Reserve may have less need to push interest rates up as rapidly, weakening the appeal of the dollar for international investors. The latest forecast from the tracking model of the Atlanta Fed suggests that first-quarter growth in America may have been only an annualised 1%.

With analysts forecasting 12% growth in S&P 500 companies’ profits this year, in other words, there was scope for disappointment for the stockmarket. That was especially so since American shares are trading on a cyclically adjusted price-earnings ratio of 29, a level exceeded only in the booms of the late 1920s and 1990s.

Globally, however, stockmarkets are not dependent on Mr Trump to push through his agenda.

Their mood started to brighten last spring as concerns about “secular stagnation” and a hard landing for the Chinese economy began to dissipate. By the end of 2016 Asian exports were picking up, commodity prices were rebounding and growth forecasts for 2017 were being revised higher.

So investors started the year in optimistic mood. A recent survey of fund managers by Absolute Strategy, a research firm, found that 74% expect global equities to produce better returns than government bonds over the next 12 months and 70% expect global profits to rise.

Recent positive data have included the German Ifo survey of business confidence, which was its strongest since 2011; a rebound in euro-zone consumer confidence; and Chinese industrial profits, which were 31.5% higher in January and February than in the same period a year ago.

Emerging markets have risen much faster than the S&P 500 this year, gaining 12%, and trade on an historic price-earnings ratio of less than 14, according to Société Générale, a French bank.

So the markets might have been doing very well even if the presidential election had produced a different outcome. Indeed, the Trump agenda could well be more of a threat than a promise for international investors, particularly if the administration pursues a more protectionist line or makes a blunder in its approach to flashpoints with China, Iran or North Korea. Markets turned round so dramatically on the morning after Mr Trump’s election that investors may yet have cause to remember the old saying: “Marry in haste; repent at leisure.”

0 comments:

Publicar un comentario