Reflation Meets Stagflation In The Asymmetric Dot Plots

By: Adam Whitehead

Summary

- The Fed is predicting and accepting a period of "mild" Stagflation.

- Neel Kashkari has more in common with Janet Yellen than she has with her other colleagues.

- The San Francisco Fed has tried to frame the FOMC as being ahead of the curve.

- James Bullard has introduced the word overkill into the debate over FOMC policy.

- President Trump is stacking his political capital chips on tax reform.

- Neel Kashkari has more in common with Janet Yellen than she has with her other colleagues.

- The San Francisco Fed has tried to frame the FOMC as being ahead of the curve.

- James Bullard has introduced the word overkill into the debate over FOMC policy.

- President Trump is stacking his political capital chips on tax reform.

(Source: Business Insider)

The last report discussed Janet Yellen's targeting of a yield curve steeper at the recent FOMC meeting and press conference. This steepening is driven by her willingness to tolerate an overshooting of inflation from the 2% target. Yellen's indication of this tolerance for inflation may be a response to new wording in the FOMC statement itself. The FOMC added the word "symmetric" to its explanation of its understanding of its 2% inflation target. A "symmetric" interpretation implies that the Fed will be equally as aggressive in responding to undershooting and overshooting inflation data.

Yellen however immediately made the interpretation asymmetrical with her overriding comment about tolerating inflation overshooting. For the FOMC, the target may be "symmetric," but for Yellen it is clearly asymmetric and implies her greater concern for undershooting. Yellen has therefore framed perceptions of what "symmetric" really means in practice, which is something different from the wording.

The FOMC is therefore fooling observers into believing that it is tough on inflation by using the word "symmetric" when in fact Yellen has no intention of delivering on this commitment.

Evidently, she wishes the yield curve to steepen, but not to get out of control to levels that will hit economic growth. An alleged official FOMC "symmetric" posture may be just enough to raise inflation expectations to steepen the curve to where she wants it without being called upon to actually do anything radical with interest rate increases.

Evidently, she wishes the yield curve to steepen, but not to get out of control to levels that will hit economic growth. An alleged official FOMC "symmetric" posture may be just enough to raise inflation expectations to steepen the curve to where she wants it without being called upon to actually do anything radical with interest rate increases.

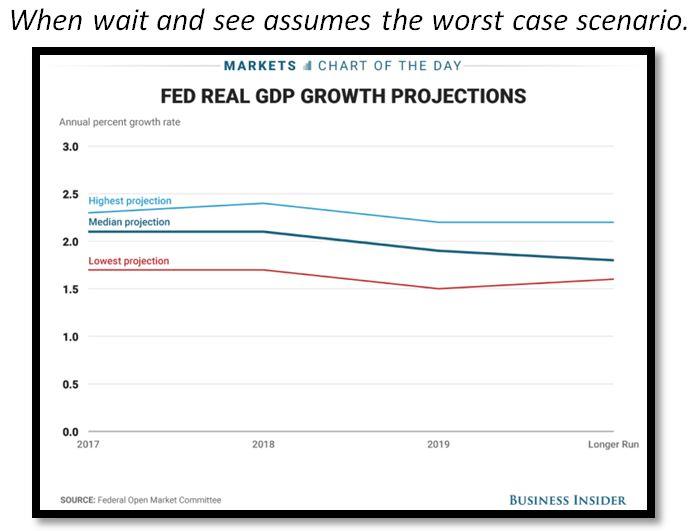

Further study of the Dot Plots from the last FOMC meeting puts Yellen's curve steepener comments into perspective. The Dots very clearly show that the FOMC does not yet see the positive impact from President Trump's expected economic stimulus. Yellen to some extent framed the Dots when she said that she remains overwhelmingly in wait-and-see mode in relation to the expected Trump stimulus. Following her reasoning, the Dot Plotters should therefore have declined to forecast GDP out into 2019 and qualified this refusal by admitting that they are in wait-and-see mode.

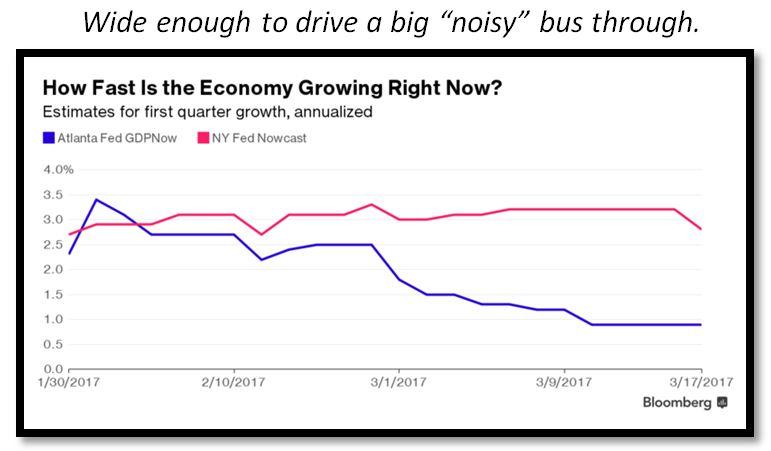

GDP Dot Plots should come with a large disclaimer, given their dispersion. The gap between the New York Fed and the Atlanta Fed over the current state of GDP clearly shows this divergence and the lack of utility in the measures. Yellen herself has cast significant aspersions over what she calls the "noisy" GDP data. Her own guide to GDP, however, is not what could be termed robust. In her words:

"I would describe our economy as one that has been growing around 2 percent per year ….. That's something we expect to continue over the next couple of years.''

Evidently she has already discounted President Trump's campaign promise of 4% GDP, which has now been revised down to 3% by Secretary Mnuchin. Her own underwhelming view confirms and converges upon the median Dot Plot assumptions with alarming precision. It should also be noted that this median trajectory is downward sloping.

Much has been made of the way that the markets are no longer calling out the Fed for being too aggressive on rate increases. Whilst the forward curve has converged on the Fed's signal of three rate hikes this year, it is also reasonable to say that the FOMC's GDP plots are converging on the market's own pessimistic baseline. This general meeting of the minds has been viewed as the Fed asserting control of the narrative and the situation. Whilst this may be the case, care should be taken over interpreting the narrative as a sign of a vigorous economy.

The Fed's pervading view is just less bad than that originally foreseen by the markets.

The Fed's pervading view is just less bad than that originally foreseen by the markets.

Given the wide dispersion of the current GDP Dots and their uniformly lower convergence trajectory over time, along with Yellen's disclaimer, the lone dissenting voice of FOMC member Neel Kashkari perhaps does not look like an isolated maverick call after all. Indeed, when Kashkari recently spoke to provide context to his dissent, his explanation sounded very consistent with the "noisy" downward sloping GDP dots. He opined that the Fed in fact does not adhere to a "symmetric" inflation target, and also treats its 2 percent goal as a ceiling. This position does not conflict with Yellen's inflation overshooting tolerance; it rather seems to support her own recent waiver clause for tolerating an inflation overshoot. Kashkari also rejected the conventional wisdom of his FOMC colleagues that gradual, preemptive increases are more effective than swifter hikes in response to actual inflation data. Once again, he is consistent with the overshooting inflation prediction of Yellen, and also has a tactical policy tool of deliberate tolerance to address it.

Kashkari's comments on the labour market then painted a picture consistent with Stagflation conditions. He believes that slack persists in the labor market despite low unemployment. An overshooting of inflation with no pre-tightening moves by the FOMC would then be acceptable based on the perceptions of labor market slack. If the inflation did not drop back, the slack in the labour market would still give the FOMC time to react with remedial rate hikes without falling behind the curve. Thus far, Kashkari's comments are much closer to Yellen's than the 9 to 1 FOMC vote against him initially suggests. By logical inference therefore, one should not rule out Yellen's potential to pull a Kashkari on her colleagues, especially after she has said that their GDP plots are "noisy."

Kashkari may therefore come in very handy for Yellen this year as a new FOMC member.

Even his position on balance sheet exit has its utility. Officially he has now stated that he is in favor of the Fed publishing a plan with a timetable for balance sheet reduction before it raises rates again and "once data support tightening monetary policy." He also says that this move in and of itself will tighten liquidity conditions in advance of the scheduled exit. In the unfolding debate about the balance sheet, he has therefore served a purpose to anchor expectations of balance sheet reduction on a baseline that is not aggressive.

Even his position on balance sheet exit has its utility. Officially he has now stated that he is in favor of the Fed publishing a plan with a timetable for balance sheet reduction before it raises rates again and "once data support tightening monetary policy." He also says that this move in and of itself will tighten liquidity conditions in advance of the scheduled exit. In the unfolding debate about the balance sheet, he has therefore served a purpose to anchor expectations of balance sheet reduction on a baseline that is not aggressive.

What the FOMC has done is to fill in the Dots in such a broad manner that implies that its members either doubt that the Trump stimulus will occur or that it will be ineffective.

Furthermore, the plotters may be assuming negative impacts from the president's trade agenda and the rise of populism in Europe. Treasury Secretary Mnuchin has already dialed back President Trump's campaign promise of 4% GDP to 3% GDP. The stimulus details have yet to be debated and legislated into existence by Congress, and it is unlikely that the president could get them through by decree given the very evident checks and balances on his policy making ability of late. Thus far, there has been an allegedly deficit neutral mix of spending proposals that redirect resources away from welfare and foreign aid to defence spending. Republican Congressmen and women are already baulking at these.

Furthermore, the plotters may be assuming negative impacts from the president's trade agenda and the rise of populism in Europe. Treasury Secretary Mnuchin has already dialed back President Trump's campaign promise of 4% GDP to 3% GDP. The stimulus details have yet to be debated and legislated into existence by Congress, and it is unlikely that the president could get them through by decree given the very evident checks and balances on his policy making ability of late. Thus far, there has been an allegedly deficit neutral mix of spending proposals that redirect resources away from welfare and foreign aid to defence spending. Republican Congressmen and women are already baulking at these.

A pattern is emerging of presidential policy stimulus inertia combined with growing Fed skepticism of the Trump stimulus plans. Yellen's tolerance for an inflation overshoot hints that she is seeing a mild Stagflation as an elevated probability. More interestingly she is willing to tolerate it, which implies that she does not see strong economic growth in the future, and that also any inflation may actually take away from economic growth by sapping consumption power. The toleration of an inflation overshoot is therefore a neat way to arriving at the place of sub-optimal economic growth implicit in the Dot Plots. Arrival at this point will then be an acceptance of the requirement for greater fiscal and monetary policy stimulus.

The experience with central bankers this year is that they have been swift to discount the rise of headline inflation on the back of oil prices coming off a low base. The inflation component of any Stagflation will thus be subdued in their opinion. The real driver of the Stagflation is therefore the weak growth dynamic, hence Yellen's asymmetric prioritising of it over the inflation overshoot.

There are therefore conflicting forces at work on the yield curve. The worsening inflation picture and the Fed's tolerance of it will steepen the curve. On the other hand, the Fed's prediction of weak economic growth will tend to flatten it. Such conflicting forces make any attempts by the Fed to target the yield curve in order to manage the process of shrinking its balance sheet very tricky to pull off successfully. The Fed may thus find it practically impossible to attempt to shrink its balance sheet meaningfully over the period between now and 2019.

The recent comments from Fed policy makers since the last FOMC meeting neatly demonstrate this balance of risks.

Philadelphia Fed President Patrick T. Harker was the first Fed speaker to try and paint over the widening cracks between the GDP Dots and case for rising interest rates. In an interview on CNBC, he moved perceptions back to a baseline on which the FOMC still does not have visibility on the Trump stimulus plans, so that it must by necessity remain gradualist.

Harker was followed by Dallas Fed President Robert Kaplan, who took up the orthodox position of articulating another two rate increases for the year. This should be expedited "patiently and gradually" in order to avoid jolting capital markets. On shrinking the balance sheet, he believes that discussion about how this will be done should continue over the course of the year even while interest rates are rising. Even when the decision on when and how to shrink the balance sheet is made and published, he is in favor of a tactical execution which is incremental and does not have a major impact on the bond markets. He would also be in favour of selling both the MBS and Treasuries that the Fed owns.

Dove-turned-Hawk Boston Fed President Eric Rosengren gritted his teeth in relation to the fallout from the tightening process, and signalled that the Fed's job is not to save the casualties who will get hurt through their greed. Flagging the commercial real estate sector as a clear bubble, he opined that managing a soft landing in this sector was beyond the FOMC's monetary policy remit. Macroprudential rules would be best served to address this problem in his opinion, which suggests capital adequacy hikes for those institutions exposed to this sector.

As President Trump pushes back on bank regulation, this dog will struggle to hunt. With this ugly inevitable real estate market outcome in mind, he then pushed his own base case scenario of four rate hikes this year, justified in his own words because:

As President Trump pushes back on bank regulation, this dog will struggle to hunt. With this ugly inevitable real estate market outcome in mind, he then pushed his own base case scenario of four rate hikes this year, justified in his own words because:

"My (his) own view is that an increase at every other FOMC meeting over the course of this year could and should be the committee's default."

Cleveland Fed President Loretta Mester was swift to downplay any economic weakness in Q1 as transient and is confident to continue to raise interest rates this year on multiple occasions, although not sequentially at each FOMC meeting. Interestingly, she is also ready to begin shrinking down the Fed's balance sheet this year.

Mester's continued Hawkish stance is now contrasted by the weakening Hawkish stance of her colleague Kansas Fed President Esther George. George has been a perennial Hawk, which makes her softening attitude stand out. Whilst she remains committed to tightening this year, she has now changed her rhetoric to become less insistent. In her opinion:

"The Federal Reserve is moving into what I consider a very critical time" and "It's going to require a lot of conversation and analysis".

Evidently, George is not seeing the kind of economic momentum that her previous Hawkish stance was based upon. This may have something to do with her view of fiscal policy. George has yet to factor in the Trump stimulus to her own baseline case for interest rate increases. Her view was recently supported by Fed Governor Jerome Powell, who noted that the recent healthcare reform failure has clouded the Fed's perceptions further.

New York Fed President Bill Dudley, often viewed as a good market signal, is also comfortable with two more rate increases this year, recently opining that the economy will cope "just fine."

It would appear that Dudley is motivated to portray the Fed as engineering a soft landing, as it emerges from the end of QE.

It would appear that Dudley is motivated to portray the Fed as engineering a soft landing, as it emerges from the end of QE.

Dove-turned-Hawk Chicago Fed President Charles Evans is also in favour of the median consensus for two more rate hikes this year, although his logic seems slightly conflicted with his own growth forecasts. He has pushed his expectations for the impact of the Trump stimulus out into 2018, hence his median positioning for this year. His raised expectations for 2018 however do not fit the trajectory of the GDP dots.

Fed Vice Chairman Stanley Fischer also supports the current median consensus for two more rate hikes this year. Fischer is however visibly shaken by the threat to globalism that President Trump represents, so his embrace of the median forecast for interest rates is loaded with a big get-out-of-jail clause should global trade relations deteriorate from here.

The Fed may therefore be struggling to keep up with real-time developments. There is however a school of thought which says that it is in fact ahead of the game.

A research piece by the San Francisco Fed neatly put the Fed's dilemma on how far to press on with rate increases given the paucity of details on the Trump fiscal plan into context. The article noted that the labour force remains artificially shrunk by those who would like a job, but who have given up looking since the Credit Crunch. Thus far, this unskilled reserve has not been called upon to participate. Maybe it lacks the skills to get the jobs on offer, and maybe the jobs for which it has skills have gone abroad. Perhaps this cohort was what tipped the balance for President Trump's victory. It has still to be repaid by the president for its kindness and support. The true unemployment rate according to the San Francisco Fed is therefore nearly half a percentage point higher, which, although significant, is much less than President Trump has estimated it to be. There is some slack there, but the Fed is already anticipating that it will be swiftly taken out and is raising rates accordingly.

The Sand Francisco Fed's report implies that the Fed is actually being somewhat preemptive, if admittedly gradually so, by raising interest rates in anticipation of the cushion in the labour force being taken out swiftly. The Fed is then actually ahead of the curve following the logic of report's authors. The growing risk is therefore that the Fed is actually way ahead of the political gridlock and fun and games in Washington that is frustrating President Trump's abilities to create jobs for the labor force slack that put him in office. The rise in bond yields and the US dollar until recently were further headwinds blowing alongside the political gridlock.

San Francisco Fed President John Williams, although not an FOMC voting member this year, is generally accepted to be a good median FOMC consensus indicator. His recent comments suggest that two more rate hikes and possibly more data permitting are expected this year, which will then put the Fed where it needs to be to start shrinking the balance sheet. 2017 can therefore be seen as the year that preparation is being made for balance sheet reduction in 2018.

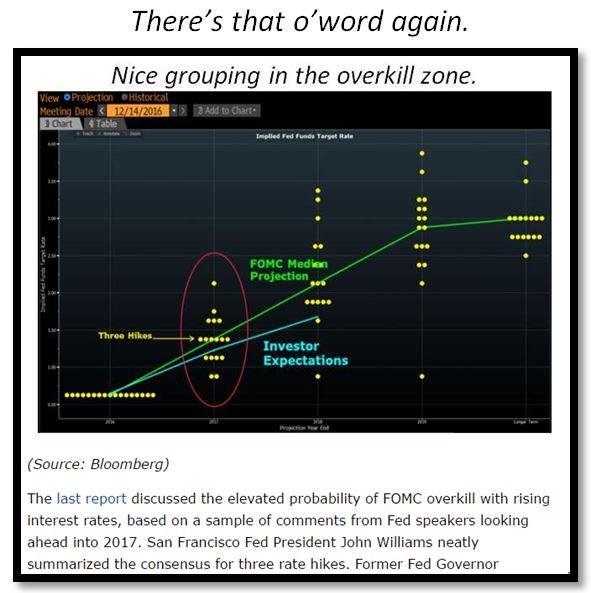

The median consensus signaled by Williams and the signal that this is preemptive by his colleagues at the San Francisco Fed are ideas that are strongly refuted by St. Louis Fed President James Bullard. Bullard has been hotly contesting the views of his colleagues of late.

In a recent report he was observed to call them out for adopting a yield curve targeting strategy without officially debating or communicating it.

In a recent report he was observed to call them out for adopting a yield curve targeting strategy without officially debating or communicating it.

(Source: Seeking Alpha)

The source of Bullard's latest dissenting rhetoric can be traced back to an earlier report in which it was suggested that the FOMC may be creating monetary policy "overkill" by following through on its expected path of tightening this year. The rhetoric and behavior of the Fed "rate setters" on the FOMC was seen as widely divergent from the "staffers" who provide their data inputs. Indeed, the "rate setters" were observed to subjectively place their own estimates of economic performance above those of the "staffer" inputs. This situation can be seen again in the latest GDP Dots which show an economic growth pessimism that contradicts the verbal signals from the FOMC about the rising path of interest rates.

(Source: Seeking Alpha)

A negative feedback loop was then discerned in a later report, which noted that market observers and FOMC members were mutually reinforcing each others' perceptions about the need for further monetary policy tightening.

Evidently, Bullard has been watching the situation closely and has decided that it has reached a dangerously unstable tipping point which needs addressing. Perhaps the appearance of Eric Rosengren's new base case of four rate hikes this year has tipped the balance. The word "overkill" has now been officially introduced by Bullard into the debate over FOMC policy going forward. In his recent comments, in relation to the median consensus indicated by John Williams he said that: "I think it is potentially overkill." Moving on to dispute the San Francisco Fed's report about the FOMC being in preemptive mode, Bullard then opined that: "We do not need to be preemptive in this situation," and that "Some of my colleagues seem to think you really have to get out in front with a faster pace of rate increases in order to keep inflation and unemployment where they are. I don't think you have to do that. I think you can take much more of a wait-and-see posture." As with Neel Kashkari, Bullard articulates a good case for caution that supports his one rate hike and done in 2017 position eloquently.

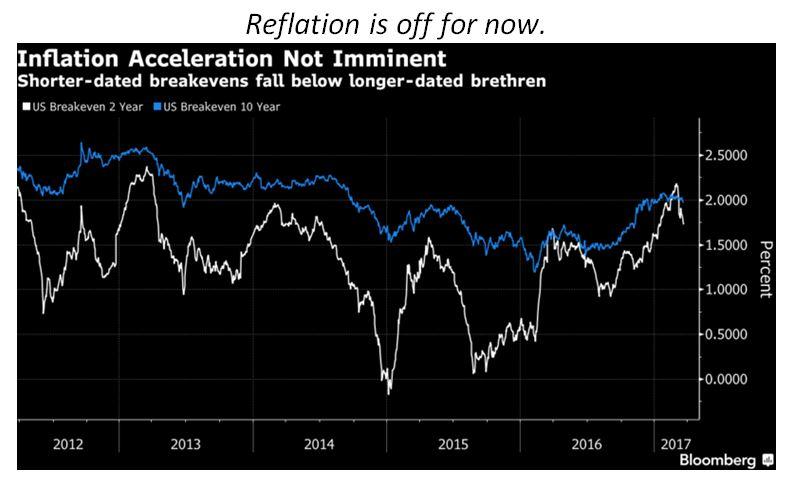

A curious discounting mechanism has come about as a consequence of converging Fed and market expectations. Whilst a great noise was being made about the Fed winning over the doubters about future interest rate increases, this victory has been pyrrhic. Market observers have accepted a swifter pace of rate hikes in 2017, yet they remain skeptical that this will continue into 2018 and beyond. The Fed's GDP Dots therefore seem to be converging upon the market expectations after all. The corollary effect has been interpreted as a thumbs-down to the Trump stimulus impact. A larger question mark is developing over the whole Trump business agenda after the failure of his recent attempts to repeal Obamacare in collaboration with Paul Ryan. Consequently, the bid for American risk assets is predicated upon and sustained by the weaker US dollar outlook that a weak fiscal stimulus and benign FOMC response beget.

Combined with the drop in the risk bid is a growing consensus that the reflation trade is over for now.

The failure of oil prices to sustain any upside has underlined this feeling. The FOMC will therefore need to proceed with caution to avoid tightening into a deteriorating market and an economic backdrop where inflation expectations are becoming subdued. By the same token however, the FOMC must be mindful of President Trump's reaction to his early failures. The passing of his Keystone Pipeline bill, sans many of his promises to get a better deal for US construction interests, was little consolation, and on the contrary was a further example of his legislating impotence.

The failure of oil prices to sustain any upside has underlined this feeling. The FOMC will therefore need to proceed with caution to avoid tightening into a deteriorating market and an economic backdrop where inflation expectations are becoming subdued. By the same token however, the FOMC must be mindful of President Trump's reaction to his early failures. The passing of his Keystone Pipeline bill, sans many of his promises to get a better deal for US construction interests, was little consolation, and on the contrary was a further example of his legislating impotence.

(Source: Business Insider)

The president will now have to pin his hopes and his reputation on enacting his tax reform policy. He will thus have to overcompensate and also to gamble on this outcome. In anticipation of the switch to this new political and economic centre of gravity, Treasury Secretary Mnuchin opined that the president's tax-code plan would face smoother sailing than the push to replace Affordable Care Act.

The stacking of all the president's political and economic chips on this one policy initiative will now frame perceptions of and also reactions to it. Thus far, positive market expectations are still way ahead of the current reality. One will have to catch up with the other. This vector dynamics of this convergence will be driven by what the president is capable of executing.

The last report noted the shift in American trade policy towards a Neo-Mercantilist model. This shift was evident at the recent G20 meeting, where the final communique omitted the traditional commitment to avoid protectionism by all members. The optimists have put this omission down to the fact that the Trump administration is in its youth and has not formulated a concrete trade position. This optimistic view overlooks the fact that the new administration has signaled what it stands against even if it has not articulated what it stands for in detail. This stance was clearly articulated by President Trump to Chancellor Angela Merkel when the two met for the first time in Washington, as the clouds of trade war gathered at G20 in Baden-Baden. After denying his guest a customary handshake, the president publicly rebuked the Germans for getting the better of trade negotiations and vowed to level the score. He then went on to demand reparations from Germany for America's vast expenditure on its historical defence. America clearly is no longer in favor of free trade, but is in favor of controlled and negotiated trade which puts America First.

The IMF was noted in the last report falling into line with American policy by highlighting the problems that the trade imbalances concentrated within a few large nations are creating. The nomination of the institution's biggest critic Adam Lerrick as Treasury Under-Secretary signals that further chastising and policy influencing is on the cards. Christine Lagarde was recently chastened enough to avoid opining on the lack of a free trade commitment at G20.

Instead she indicated obliquely her aversion to protectionism by saying that the current global recovery is at risk from the "wrong" policies without elaborating on what these are. She then committed the IMF to its original narrow remit from when it was established as an extension of US foreign policy rather than the globalist one that it has morphed into when she stated that it will operate "vigorous exchange rate surveillance and analysis of global imbalances." In the future, the IMF may be less of a champion of free trade and more a platform through which to negotiate managed trade.

Instead she indicated obliquely her aversion to protectionism by saying that the current global recovery is at risk from the "wrong" policies without elaborating on what these are. She then committed the IMF to its original narrow remit from when it was established as an extension of US foreign policy rather than the globalist one that it has morphed into when she stated that it will operate "vigorous exchange rate surveillance and analysis of global imbalances." In the future, the IMF may be less of a champion of free trade and more a platform through which to negotiate managed trade.

0 comments:

Publicar un comentario