Is The Economy Doing Well?

by: Lawrence Fuller

- Janet Yellen tells us the economy is doing well.

- The stock market followed her lead.

- Other financial market indicators are telling a different story.

- I see more signs that we are nearing the end of the current economic expansion and that the economy is not doing well.

- The stock market followed her lead.

- Other financial market indicators are telling a different story.

- I see more signs that we are nearing the end of the current economic expansion and that the economy is not doing well.

Janet Yellen asserted that "the economy is doing well" in the press conference that followed the Fed's decision to raise short-term interest rates an additional 25 basis points to what is now a range of .75 to 1%. Yellen had no choice but to suggest that a rate hike was affirming the economy's strength. Yet, while the stock market (NYSEARCA:SPY) rallied in response, other financial markets indicators were refuting her assertion.

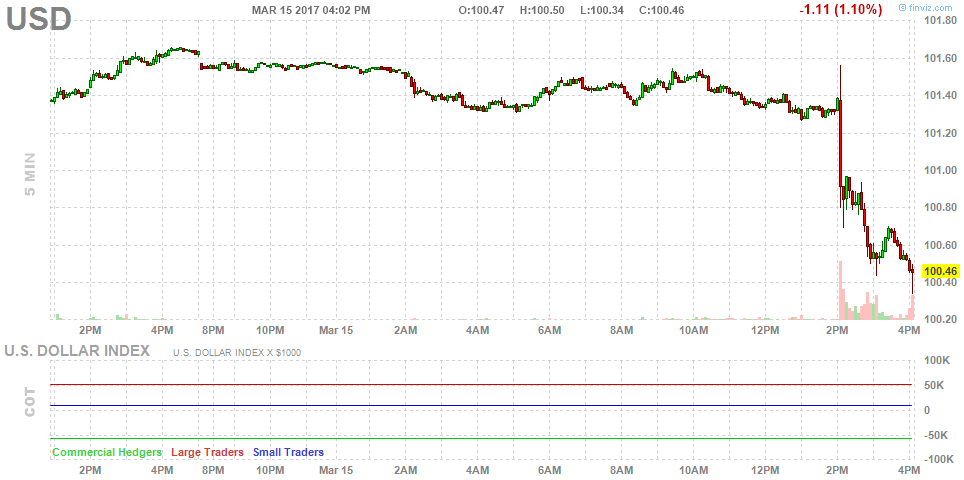

The dollar (NYSEARCA:UUP) plunged after the Fed's rate hike, which doesn't suggest to me that we will see a steady rise in short-term interest rates this year. Nor does it suggest that the economy is on a strong footing either.

The price of gold surged, perhaps in response to the weak dollar as well as the belief that the Fed will allow inflation to run above its target of 2% this year. I have been bullish on gold (NYSEARCA:GLD) and the gold miners (NYSEARCA:GDX) for reasons other than a rise in inflation. I think the outperformance of both this year has as much to do with fear and uncertainty about what lies ahead, given the turmoil we have seen in Washington since the new administration took office.

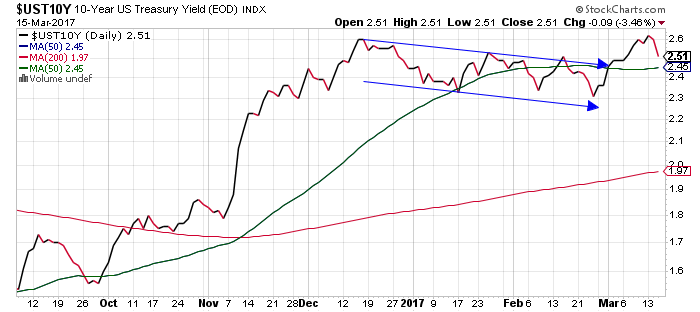

Long-term Treasuries (NYSEARCA:IEF) rallied following the rate hike, which does not indicate an expectation for faster rates of economic growth or inflation in the future. It indicates the exact opposite.

The 10-year Treasury yield was unable to break above its previous high of 2.6% set in December of last year, instead declining 9 basis points to 2.51%.

Wall Street pundits interpreted these market responses to mean that investors had been concerned about a more hawkish outlook for interest-rate policy by the Fed, prior to yesterday's meeting. When there was no change in the Fed's prior forecast for additional interest-rate hikes this year or next, they claimed that investors viewed it in a dovish light. I have a different interpretation of the picture these puzzle pieces make when fit together with a few others.

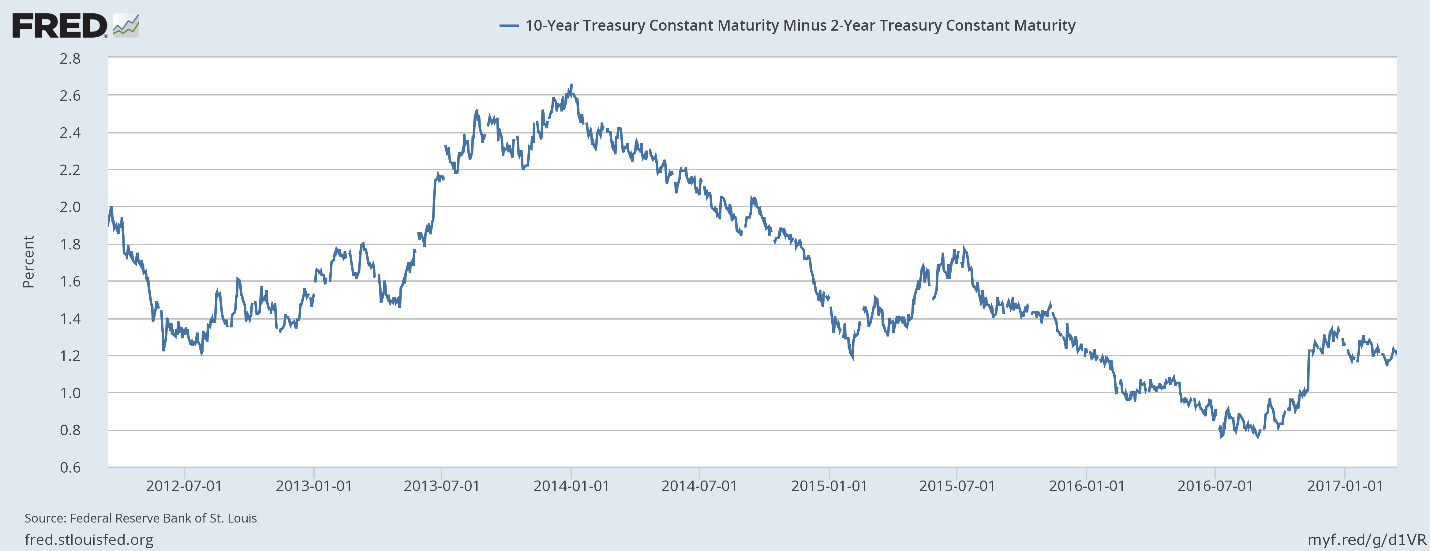

As short-term interest rates have been rising this year long-term rates have been rising at a slower rate, leading to a narrowing spread as can be seen below. This spread was widening late last year in anticipation of a stronger economy. That no longer appears to be the case.

I listened to the market experts on CNBC exclaim yesterday that "wages are up," and that "confidence is through the roof." This is how they were explaining the stock market reaction to the Fed's actions and commentary. It is a simpleton's analysis.

Perhaps the economy is doing well for the investor, but it is not doing well for the average American household and I think that this is what financial markets are telling us outside of the stock bourses.

The Fed may have other reasons for continuing to raise short-term interest rates which may be legitimate, but a strengthening economy is not one of them.

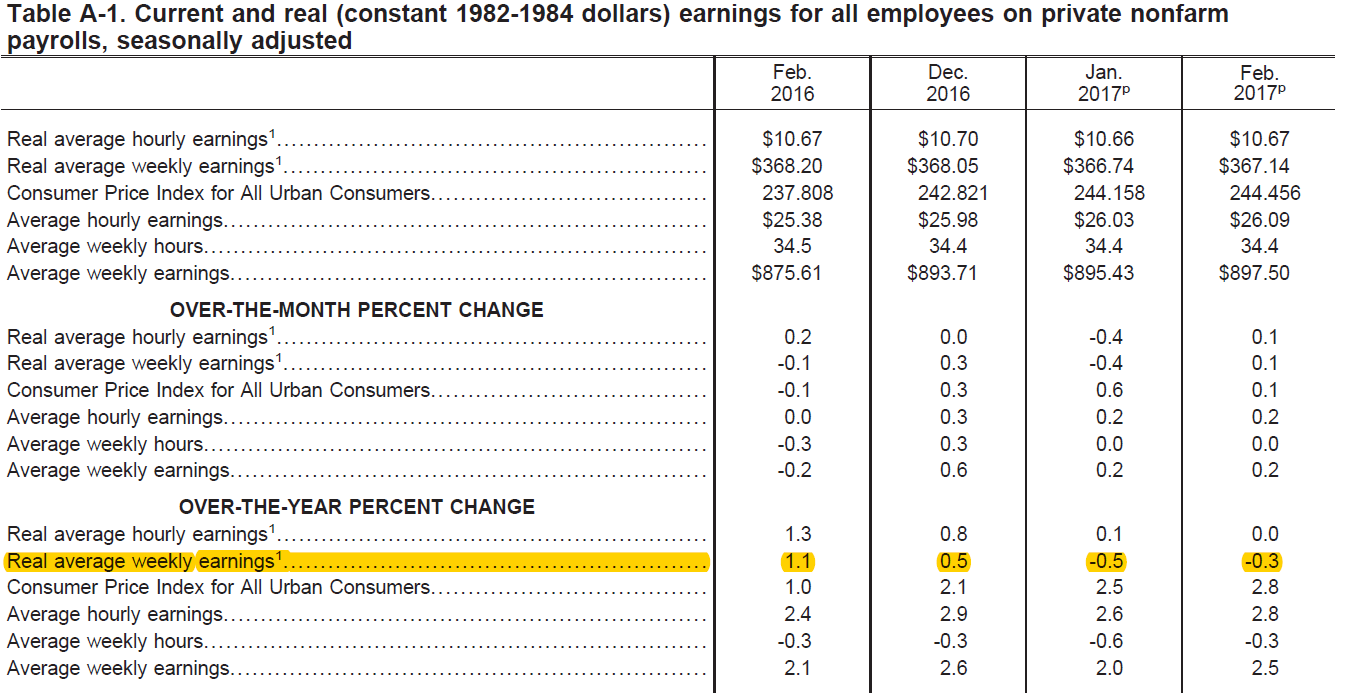

Yesterday we learned that real incomes for all employees declined on a year-over-year basis for the second month in a row. This report received NO coverage from the financial press.

Changes in real average hourly earnings are one of the most effective tools we can use to forecast changes in real consumer spending, which is what fuels two-thirds of our economic growth. As the consensus of economists and market pundits continues to focus on monthly job creation, I have been pointing out for months that we would eventually see a decline in real wages as the rate of inflation rose with easier year-over-year comparisons for energy prices.

This is also why I have been forecasting a steady decline in the rate of economic growth over the past two years.

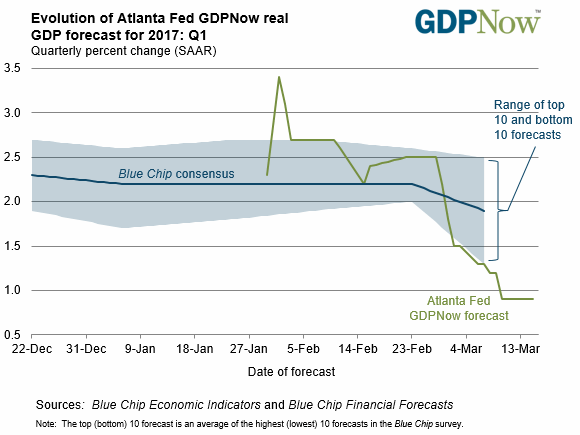

The Atlanta Fed lowered its forecast for first-quarter economic growth from 1.2% to just 0.9%, after yesterday morning's retail sales report led it to lower its expectations for consumer spending growth in the quarter to just 1.5%. I believe the decline in consumption is a direct result of the decline in real wages.

How can this be after two supposedly powerful months of job creation to start the new year?

Because income growth is the primary driver of consumer spending, rather than jobs, as the pundits and the main-stream media continue to erroneously purport.

In my view, the economy is not doing well. It is gradually weakening. The Fed is doing its best to normalize interest rates, so that it is better prepared to address any future shocks to the economy. It has no option other than to suggest that the economy is strong as it does so, for fear of roiling the stock market and undermining the wealth effect that it worked so hard to create.

It is walking a fine line between building ammunition for the next economic downturn and tightening financial conditions in a weakening economy, which may instigate that downturn.

The stock market continues to levitate on promises of infrastructure spending, regulatory reform and massive tax cuts, but Washington is mired in a battle over healthcare and other political absurdities, both of which are likely to undermine confidence moving forward. The stock market's ability to serve as a discounting mechanism was undermined by monetary policy many years ago and it has yet to regain that competence, despite the end of quantitative easing and zero-interest rate policy in the US. I think it is still inebriated by the liquidity being provided by foreign central banks. Therefore, I think it is better to focus on the price action in bond, currency and commodity markets for indications of domestic economic health and what lies ahead.

0 comments:

Publicar un comentario