Do smart-beta investment funds work?

As with all investment, it’s a question of timing

A recent survey of institutional investors showed three-quarters were either using or evaluating the approach. By the end of January some $534bn was invested in smart-beta exchange-traded funds, according to ETFGI, a research firm. Compound annual growth in assets under management in the sector has been 30% over the past five years.

But does it work? The danger here is “data mining”. Carry out enough statistical tests, and you will always find some strategy that worked in the past. It may be that stocks beginning with the letter “M” have outperformed other letters of the alphabet; that does not mean they will do so in future.

According to Elroy Dimson of Cambridge University and Paul Marsh and Mike Staunton of the London Business School, researchers have found 316 different factors that might form the basis for a successful investment strategy.

The best-known fall into four groups—size, value (including dividend yield), momentum (buying stocks that have risen in the recent past) and volatility (buying less-risky shares).

Research by Messrs Dimson, Marsh and Staunton shows that the size, value and momentum effects have worked across a wide range of markets over many decades. The low-volatility effect (for which fewer data are available) has worked in America and Britain over an extended period.

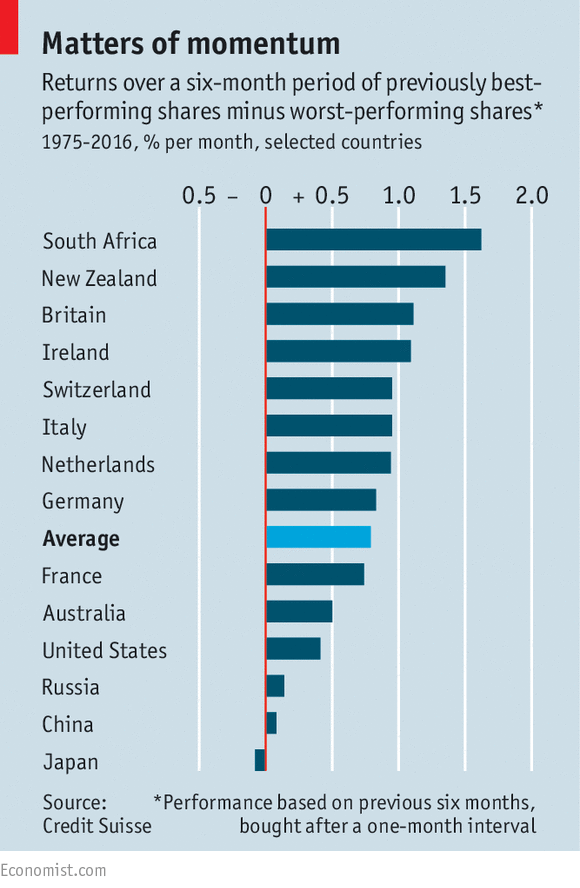

In the case of momentum, the effect is very large. In a theoretical exercise (see chart), an investor identifies the best-performing stocks over the previous six months, buys the winners and sells short the losers (ie, bets that their prices will fall). The exercise assumes it takes a month to implement the strategy each time. In some countries, the return is more than 1% a month; globally, it is 0.79% a month, or nearly 10% a year. That is more than sufficient to make up for any transaction costs.

Similarly, smaller companies and value stocks have beaten the market over the long run.

Nevertheless, there have been times when such shares have been out of favour for years. The returns from such strategies have been much lower than from momentum (2-4% a year): not enough, perhaps, to induce a patient buy-and-hold strategy among those willing to ride out the bad times.

The obvious answer is to select the right factors at the right moment. The obvious question is how to do so. Relying on past performance is risky. A study* by Research Affiliates, a fund-management group, found that a factor’s most recent five-year performance was negatively correlated with its subsequent return. This is probably a case of reversion to the mean. Stocks that perform well over five years are probably overvalued by the end of that period; those that perform badly for the same period are probably cheap.

Indeed, the publicity given to smart beta, and the money flowing into these funds, will lead to upward pressure on shares exposed to the most popular factors. (Add an extra layer of irony when this applies to momentum stocks.) Investors who believe in the beta mousetrap may find that the rodents have already escaped with the cheese.

* “Forecasting factor and smart beta returns” by Rob Arnott, Noah Beck and Vitali Kalesnik

0 comments:

Publicar un comentario