Consumers and firms see a Trump boom. Most forecasters do not

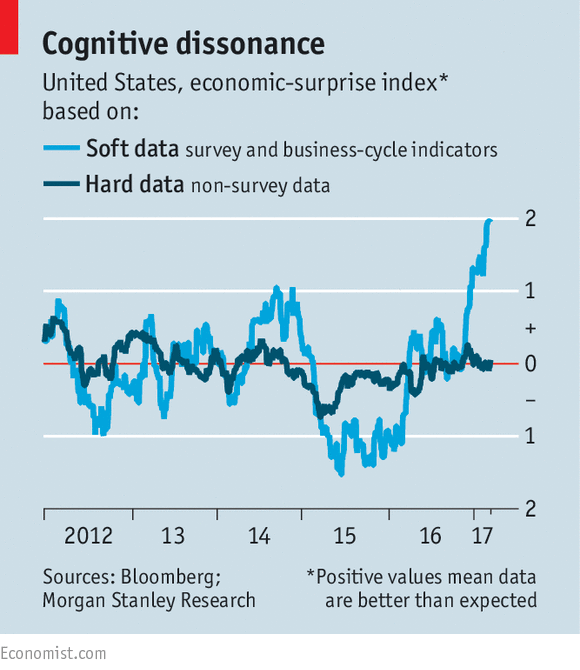

Economic indicators have rarely sent such mixed signals

IS AMERICA’S economy booming? Consumers seem to think so. Their confidence, as measured by the Conference Board, a research group, is at its highest since December 2000, when the dotcom bubble had not fully burst. Yet in both January and February this year, personal consumption fell. The signals from firms are no less mixed. Small-business confidence is so high that relying on this alone to predict annualised GDP growth in the first quarter leads to a staggering forecast of 7.1%, according to Goldman Sachs, a bank. Order books are swelling and jobs are plentiful, firms say. Yet industrial production has been flat since December, and banks have slowed business lending dramatically. Americans seem wildly enthusiastic about the economy, but it is not clear why.

The surge in the so-called “soft” economic data, drawn from surveys, began when Donald Trump won the presidential election in November (see chart). It coincided with a boom in the stockmarket, up 10% since then, as investors began to salivate over the prospect of tax cuts and deregulation. Yet the “hard” economic data, which measure actual economic activity, have trundled along much as expected. The disparity has caused growth forecasts to fall out of sync.

As The Economist went to press, a model at the Atlanta Federal Reserve put annualised growth in the year’s first quarter at 1.2%. A competing forecast at the New York Fed put the rate at 2.9%. . It is tempting to discount strongly upbeat surveys as driven by politics. Owners of small businesses lean heavily Republican. Consumer confidence is up most among over-55s, who are also likely to have voted for Mr Trump. Most economists’ forecasts are closer to the number from Atlanta than the one from New York. Many of them are mindful of the fact that the economy has often seemed to sag in the first quarter of recent years. An attempt by government statisticians in 2015 to purge the growth data of seasonal factors may not have been a complete success. Most important, no tax cut or serious deregulation has happened yet. Instead the Republicans have failed to pass a promised health-care reform, which contained large tax cuts for the rich, on their first attempt. (It may soon reappear, but if it does, its passage, especially through the Senate, is far from certain.) There is reason to wonder whether the party is capable of overcoming the political squabbles that will inevitably accompany tax reform.

Yet even if Mr Trump fails to overhaul the tax code completely, few doubt that Congress will pass a simple cut in rates for him to sign. And confidence in the economy may still prove self-fulfilling.

Republicans have long held that replacing Barack Obama’s chilliness towards business with a warm embrace of commerce would lead to an investment boom (on this, they might cite the support of John Maynard Keynes, who wrote that businesses are “pathetically responsive to a kind word”). Although there was no sign of a recovery in investment in the fourth quarter of 2016, sales of capital goods, such as machinery, have picked up a bit this year.

Whether that trend continues will reveal whether confidence is crystallising or dissipating.

Some conservatives, impatient to trigger what they see as an inevitable surge in investment, want tax cuts, whenever they happen, to be backdated to the beginning of 2017.

Retrospective tax changes are rarely a good idea. For the moment, Republicans should be encouraged that two sectors of the economy—housebuilding and manufacturing—have accelerated tangibly. That should please some of Mr Trump’s blue-collar supporters. In February the trade deficit, which Mr Trump views, strangely, as a barometer for economic strength, was 4.5% lower than it was a year ago. A worldwide economic acceleration has helped this trade and manufacturing revival. The dollar has fallen back almost to where it was on the eve of Mr Trump’s election, making American goods cheaper in other countries.

You’re up, then you’re down

What if the surge in confidence proves fleeting? The stockmarket would surely sink. But it is not as if America was in a funk before Mr Trump won in November. The world economy—and financial markets—have been firming up since mid-2016, partly because of fiscal stimulus in China.

America’s recent growth of about 2% has been enough to eat up much of the slack in the economy, as rising inflation shows. Much more productivity-boosting business investment would certainly be welcome, not least because Americans produced barely any more per hour worked in 2016 than they did a year earlier. But Mr Trump’s promise of 3.5-4% growth has never been a realistic goal, because America’s greying workforce imposes a lower speed limit on the economy than in the past.

As that becomes more apparent, the economic elation may subside. If so, those who have been sceptical about soft data as they have heated up should remember to be equally unmoved as they cool down.

0 comments:

Publicar un comentario