Chinese finance is storing up trouble for the rest of the world

Given its macroeconomic imbalances, China could unleash global mayhem

by: Martin Wolf

.

Donald Trump, US president, is to meet Xi Jinping, his Chinese counterpart, at Mar-a-Lago in Florida this week. Discussions of economics seem likely to focus on China’s trade and exchange rate policies. This would be a mistake even if the US president’s views of trade were not mistakenly fixated on bilateral imbalances. Far more challenging and important is integrating China into the financial system. US policymakers should worry about China’s capital account, not its current account. That is where danger now lies.

Why does the capital account matter more? The answer is that this is where two interrelated aspects of an economy interact with the world economy: macroeconomic balances between savings and investment; and the financial system. In both respects, the Chinese economy is, to cite the celebrated words of former premier Wen Jiabao, “unstable, unbalanced, uncoordinated and unsustainable”. That was true in 2007, when he said it. It is truer today. As the Chinese authorities realise, but their western counterparts may not, the integration of China’s financial system into the global economy is fraught with peril.

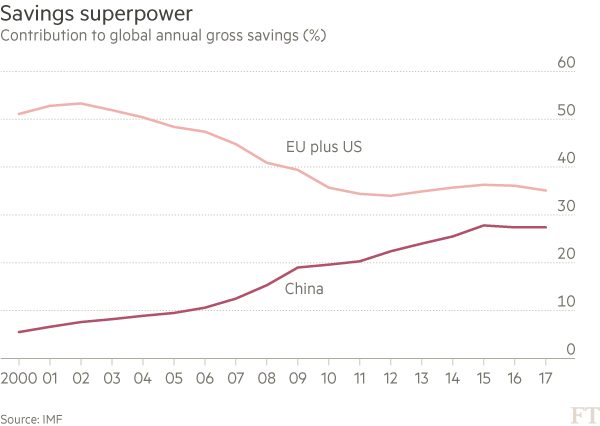

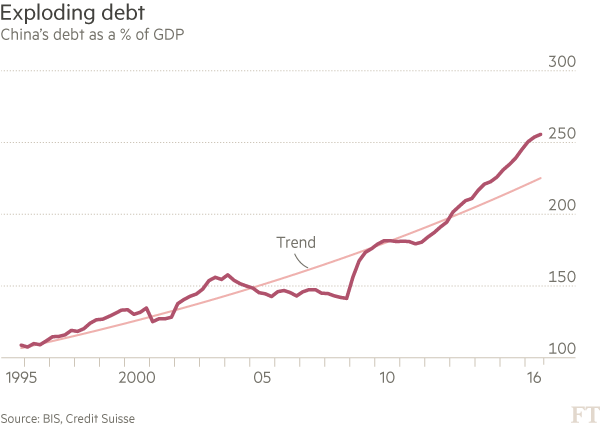

Consider a few facts. Annual gross savings in the Chinese economy amount to 75 per cent of the sum of US and EU savings, at over $5tn last year. China’s gross investment, at 43 per cent of gross domestic product in 2015, was still above its share in 2008, even though the economy’s rate of growth had fallen by at least a third. To sustain such high investment, the ratio of credit to GDP soared from 141 per cent of GDP at the end of 2008 to 260 per cent at the end of last year. The “shadow banking system”, in the form of “wealth management products” and other instruments, has exploded. Interbank lending has also soared. Last, but not least, the banking system is now the world’s largest.

Financially, China is the wild east. Remember what the wild west did over the last century: the Great Depression and Great Recession originated in the interaction between US-led finance and the global economy. In view of its macroeconomic imbalances and financial excesses, China could deliver at least as much global financial mayhem.

I have argued elsewhere that it is essential to understand the interaction of macroeconomics with finance. China’s external accounts already played a significant role in the run-up to the financial crisis of 2007-08. Now the dangers it creates are still greater.

The macroeconomic issue is simple: China saves more than it can profitably invest at home. In 2015, gross national savings were 48 per cent of GDP. World Bank data show that households contributed only a half of this. The rest came from corporate profits and government savings.

International comparisons suggest that economic growth of 6 per cent warrants investment of little more than a third of GDP. This indicates that China’s surplus savings — surplus, that is, to domestic requirements — may be as much as 15 per cent of GDP.

Where might such surpluses go? The answer is abroad, in the form of current account surpluses. That is what happened before the financial crisis. It is likely that this is what would also happen now if the government relaxed exchange controls and brought credit and debt growth to a halt. Capital would pour out, the renminbi would tumble and, in time, a globally unmanageable current account surplus would emerge.

Today’s credit growth and consequent financial fragility are a direct consequence of the desire to prevent this from happening. It has been the way to keep investment up at uneconomic levels. The Chinese authorities are in a trap: either halt credit growth, let investment shrink and generate a recession at home, a huge trade surplus (or both); or keep credit and investment growing, but tighten controls on capital outflows.

Why is the latter essential? With such large and growing stocks of liquid, risky or low-yielding financial assets, plus a huge flow of savings, not to mention the anxieties caused by the anti- corruption campaign, Chinese corporations and individuals have been desperate to take money out.

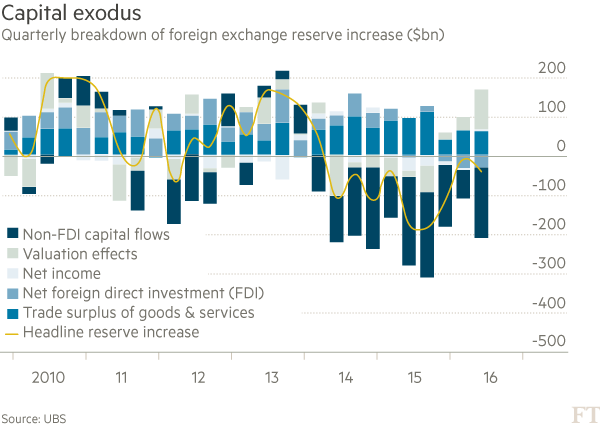

This explains why, despite a persistent trade surplus, the country’s foreign exchange reserves fell from $4tn in June 2014 to $3tn in January 2017. The reserves can certainly fall further. But the Chinese authorities will not wish them to fall indefinitely. Since they also recognise the dangers of allowing the renminbi to fall too far, they have duly tightened controls on capital outflows.

Suppose the Chinese authorities adopted, instead, the alternative policy of rapid liberalisation of both inflows and outflows, while relying on credit expansion to sustain domestic demand. It is possible, but unlikely, that the flow of money into China from abroad would match the outflow, as foreigners and Chinese both diversified their portfolios. Yet that would also cause three headaches. First, the domestic macroeconomic imbalances would persist. Second, the financial sector would become still more fragile. Finally, this vast, complex and fragile financial system would become fully integrated with the rest of the world’s, itself still far from fully stable. Instead of the Chinese financial crisis that many now think imminent, this would enormously increase the likelihood of another global crisis with China, not the US, at its heart.

These are huge challenges that need to be discussed in full between the US and China (and others). They have profound implications for trade, but they are not about trade policy at all.

They require joint consideration of macroeconomic and financial policy. They also demand attention to the management of China’s external account: above all, exchange controls, the exchange rate and foreign currency reserves.

Mr Xi has people in his government who at least understand these issues. Is the same also true for Mr Trump? The stability of the world economy depends on the answer. Alas, I suspect it is no.

0 comments:

Publicar un comentario