They think Amazon is going to grow faster, longer and bigger than almost any firm in history

EVERY chief executive hopes to lead his company to success. Jeff Bezos, Amazon’s boss, wants something more epic. A prominent wall in the company’s headquarters in Seattle is covered with narratives from historic explorations: excerpts from “The Odyssey”; notes from the journey of Lewis and Clark as they ventured across America; the transcript of the first moon-walkers talking to mission control. At the end, ones and zeroes spell out how far the company has got: “Day One”.

The phrase, reflecting Mr Bezos’s belief that Amazon’s journey has just begun—and begins again each day—is the company’s mantra. At any other firm such grandiosity would invite derision. At Amazon, it makes investors drool and rivals quake.

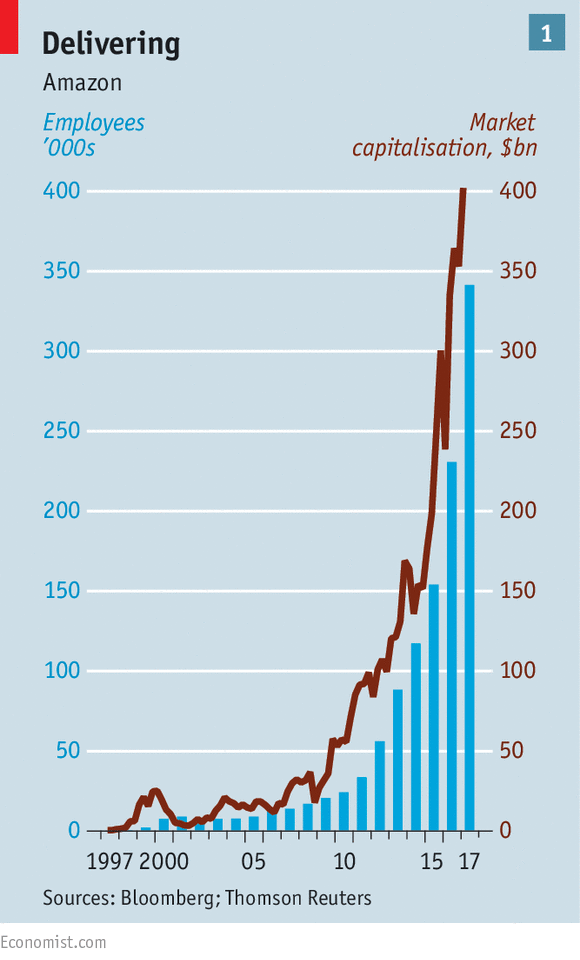

Amazon, which went public 20 years ago, is now the world’s fifth-largest company by value, worth over $400bn (see chart 1). Its e-commerce site accounts for about 5% of retail spending in America, roughly half the share of Walmart, the biggest firm in the sector. It is the biggest online retailer in America, and accounts for over half of all new spending. Its cloud-computing business, Amazon Web Services (AWS), is larger in terms of basic computing services than the three closest competing cloud offerings combined. Since the start of 2015 Amazon’s share price has risen by 173%, seven times the growth of the preceding two years. Operating profits have expanded, too, but at $4.2bn remain relatively small—which is how shareholders like it. Amazon has always emphasised the value of long-term growth (presumably with some bigger profits down the line), and investors have come to accept this.

In February, when Amazon reported higher profits but lower revenue than expected, its share price temporarily dipped. Shareholders worried it might not be set to grow as quickly as they had hoped.

Morgan Stanley, a bank, expects Amazon’s sales to rise by a compound average of 16% each year from 2016 through to 2025: that is higher than its estimates for Google or Facebook. That is a slower pace than Amazon managed over the past decade; but the bigger a company is, the harder it is to keep growing. Amazon’s annual sales of $136bn are almost 50% more those of Alphabet, Google’s parent, and over four times Facebook’s. Credit Suisse, another bank, calculates that only ten firms with sales of more than $50bn have managed to grow by an average of 15% or more for ten years straight since 1950; no company with sales of more than $100bn has done so. If Amazon were to pull it off, it would be the most aggressive expansion of a giant company in the history of modern business.

That raises two questions. The first is how Amazon could possibly achieve this. The second is which industries it might upend in the process.

Amazon’s growth to date has come from following a rather vague mission—becoming “Earth’s most customer-centric company”—with massive investment that takes a long view when it comes to attracting, keeping and making more money from those customers. Year after year, an expanding collection of services sweeps up more customers and creates more cash. The company produced $16bn in cashflow before investment last year, more than four times the level five years earlier. That is thanks to its scale, says Heath Terry of Goldman Sachs, the investments it chooses and its skill at executing them.

The virtuous buzzsaw

The money it has spent on its e-commerce system has set new standards for service and price. Its site and the formidable logistics behind it are an alternative to queues and trekking from shop to shop.

Little wonder that, according to a recent Harris poll, Americans hold Amazon in higher esteem than any other Company.

Having first taught people that it was safe to shop on computer screens, Amazon went on to offer them new ways of buying stuff. The Kindle is not just an easy way of reading e-books; it is a very convenient way of purchasing them. Alexa, a virtual assistant linked to the company’s Echo speaker, makes many sorts of shopping all but frictionless—a consumer can say she needs shampoo and that shampoo will arrive on her doorstep.

The company has also found new things to sell: most notably, computing power delivered as a service. The ability to get the number-crunching, data-storage and development tools they need without capital expenditure has been a blessing for startups and larger customers alike. Netflix, a streaming-video company, uses AWS to serve 94m subscribers; America’s Central Intelligence Agency uses a version customised to its security needs. (The Economist’s website is also hosted by AWS.)

Achieving such successes takes hard work: the company has a reputation for intensity and a demanding culture. It also requires a willingness to spend. “It’s very easy for a large company to get trapped into not wanting to place too many bets and fail too often,” says Jeff Wilke, who leads Amazon’s e-commerce business. It is a trap he is determined to avoid. A massive expansion of Amazon’s e-commerce services has led it to lose money in two of the past five years. It is also pouring $3bn into an attempted expansion into India.

Some bets have failed. The Fire Phone, which Amazon launched in 2014, flamed out. The idea that it could be used to recognise, and find a seller of, any product it saw turned out to be far more interesting to Amazon than to its customers, who preferred simple capabilities available from other phones.

Amazon’s successes have come from finding ways to spend money that bring increasing returns. Both AWS and the e-commerce business benefit from economies of scale. But they are also platforms that benefit from “network effects”—the more people buy from them, the better they get. As more firms use AWS, more developers know how to use it, giving Amazon more data with which to optimise it, which makes it more attractive in its turn. More shoppers on the Amazon site make it more alluring to third-party sellers, which increases the range of goods it can offer, which attracts more shoppers.

Alexa shows some signs of becoming a similar platform, though these are early days. Makers of cars, thermostats and other hardware can build Alexa into their gear. Alexa already has more than 10,000 “skills”, similar to smartphone apps, that turn wishes into commands. The more skills and Alexa-powered devices there are, the more appealing the digital assistant becomes to consumers, which means a bigger market for new skills.

Divisible only by itself

One of Amazon’s most successful offerings has been its Prime subscription. Originally this just offered free shipping, but the company has added more and more new perks—two-hour shipping, for instance, or free and sometimes exclusive streaming video—to encourage people to stump up the annual subscription ($99 in America). The idea, Mr Bezos told investors last year, is to make Prime “such a good value, you’d be irresponsible not to be a member.”

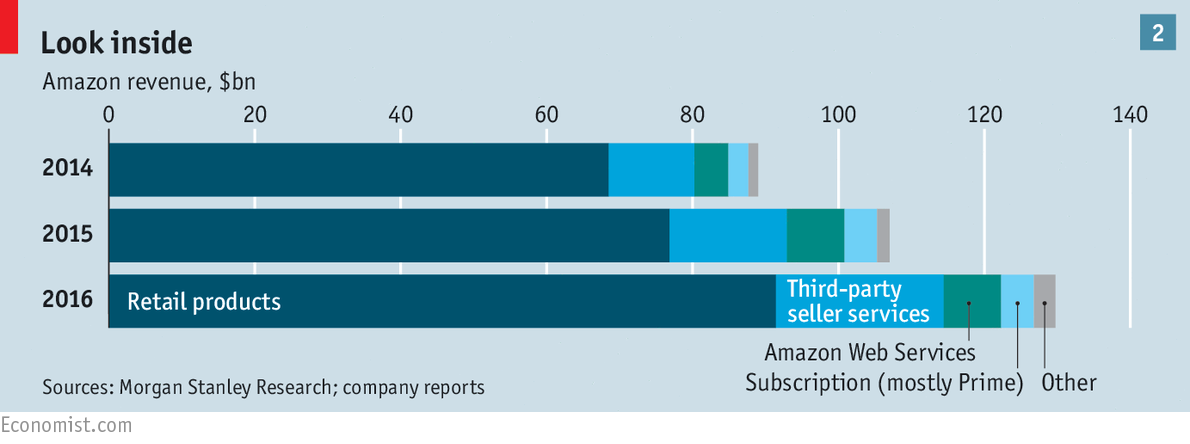

That is costly. In 2017 Amazon is expected to spend $4.5bn on television and film content, roughly twice what HBO will spend. But it has a big payoff. Users who subscribe to Prime spend at least three times as much as Amazon shoppers who don’t subscribe, estimates Brian Nowak of Morgan Stanley. In part this is a selection effect; it makes more sense for heavy shoppers to subscribe. But it also seems that, having subscribed, they shop yet more heavily, knowing that they incur no further shipping costs when they do so. Mr Nowak reckons the company had 72m Prime members last year, up by 32% from 2015. As well as focusing on customers, Amazon has proved rather good at treating itself as one; making something it wants and then selling it to others. Amazon wanted the benefits cloud computing offered, and having provided them for itself, decided to spread the costs by providing them for others through AWS. The customer’s-eye view was a boon; Amazon understood the needs of startups better than established computing firms could. Last year AWS’s revenue reached $12bn, up by more than 150% since 2014 (see chart 2). Allowing others to use the company’s e-commerce platform, warehouses and other services is an even bigger business. Fees from sellers around the world who use Amazon reached $23bn in 2016, nearly twice what they were in 2014.

Some of the company’s current investments may deliver similar benefits. It is testing a grocery in Seattle that lets shoppers buy items without stopping at a cash register. This may prove a model for future Amazon shops. But it seems just as likely that the automatic-checkout technology will be sold to other retailers. It is also planning a $1.5bn hub for cargo planes in Kentucky. At the very least, that will help meet demand in busy periods and give it more bargaining power when dealing with vendors such as UPS and FedEx. But Amazon’s fleet could one day be part of a logistics operation that rivals them.

Such experiments raise a tantalising prospect for shareholders. AWS provides the tools for companies to do business online; Amazon is a dominant online platform for selling digital and physical goods.

Eventually, the company could offer infrastructure for all kinds of commerce, online and off. It already has one of the things that modern business most desires: data. It knows what its customers buy, listen to and watch; it has a good sense of how they respond to prices. The more data Amazon has, the better it can boost sales via its site through recommendations, advertisements, new services, products and more. That would make it ever more difficult for rivals to catch up.

Mr Bezos claims, as a corollary to thinking only of customers, never to think of rivals. However, the list of current and possible competitors that Amazon is required to include in its annual filings is long and getting longer. It ranges from retailers and search engines to film producers and, as of last year, logistics and advertising firms. Sir Martin Sorrell, boss of WPP, the world’s biggest advertising company, might seem to have little to fear from a firm which last year made an estimated $2bn from advertising. But Amazon is a new intermediary between brands and customers, one which could conceivably use its direct relationships and stacks of data to cut out the ad-agencies altogether. “What worries you when you go to bed at night and wake up in the morning?” Sir Martin said in a recent conference call. “It’s Amazon.”

For many retailers Amazon is both a competitor and a way of getting more business. There are more than 100,000 companies, Amazon says, that earn more than $100,000 a year selling through the firm’s site. Many of them are competing with their host in one way or another. Some go up against the company’s own private-label products, which range rather bafflingly from potato crisps to baby wipes to loafers. Many more go up against the stock that Amazon buys and resells.

For anyone selling on Amazon, prominent placement in the “buy box” that appears on screen when something is searched for is a big boost. According to One Click Retail, a consultancy, products in the buy box account for 86% of sales on the website and 93% on the mobile app. By reverse-engineering the algorithm that runs the box, the consultants found that if a seller pays Amazon to handle warehousing and logistics on its behalf, which probably speeds up shipping, it is more likely to win a spot in the box. So on the occasions when Amazon’s retail offering loses the buy box, it still gets a piece of the action.

All good things...

Bigger competitors do not want to work through Amazon. Some will not use AWS because they don’t want to subsidise a rival. Large retailers are seeking to match Amazon’s standard of fast, cheap shipping on their own. But that lowers the margins for their online sales and risks cannibalising sales from their stores. The competition thus threatens to make many of them permanently less profitable.

Last year Walmart made a particularly expensive bid to fend off Amazon, paying $3bn for Jet.com, an e-commerce startup. Marc Lore, Jet.com’s boss, has history when it comes to competing with Amazon. “The Everything Store”, a book about Amazon by Brad Stone, a journalist, tells the story of Quidsi, a previous startup of Mr Lore’s that sold nappies through a site called Diapers.com. When Amazon was building a nappies business, the bigger company cut prices so rapidly that Quidsi reckoned that matching them would lose it $100m in three months. Quidsi agreed to be bought in 2010.

Other competitors are worried, too. In December Amazon challenged Netflix by expanding Prime Video to more than 200 countries. “I feel like we’re competing with an unusual person,” Reed Hastings, Netflix’s boss, has admitted. “Because Jeff’s there, it’s kind of scary.” This is not a winner-takes-all contest; two-thirds of American Prime subscribers also subscribe to Netflix, according to Cowen, a financial-services firm. But as Prime Video’s offering improves, some Netflix viewers might drop their subscription.

Netflix hopes to keep them by spending on its exclusive shows; like Spotify in music, it also has the advantage of an established brand and a customer base. But competition is hotting up. Disney, Fox, NBC Universal and Time Warner have beefed up a streaming competitor of their own, Hulu.

The other tech giants have their own reasons to be worried about Amazon—though they may also have the best defences. Apple faces the risk that Amazon, not iTunes, becomes the default platform for streaming and buying content; but it has the diversified revenue needed to fight its corner.

Google, for its part, does not want shopping through Amazon, and particularly Alexa, to cut it out of the loop, jeopardising its advertising revenues; nor does it want Alexa to be the platform people chose for running their homes. In February Google said its new assistant—called, simply, Assistant—would not only power a device called Google Home, but roll out to smartphones using Android, its mobile operating system. Their strength in mobile phones gives both Apple and Google an edge over Amazon.

Tech giants will also be fighting Amazon in the cloud. Microsoft is its strongest competitor, but Google and IBM are formidable, too. All four are fighting to lower prices and provide better technology, with billions now being pumped into AI. If competitors fail to halt Amazon’s whirl of activities, antitrust enforcers might yet do so instead.

This does not seem an imminent threat. American antitrust authorities mainly consider a company’s effect on consumers and pricing, not broader market power. By that standard, Amazon has brought big benefits.

Two perils lurk, however. One, for now, is theoretical. In a recent article in the Yale Law Journal, Lina Kahn argued that, among other things, the scope of Amazon’s activities may make it impossible for competitors not to end up relying on it. If regulators paid more heed to market power, that could be a red flag—especially as Amazon continues to grow and provide its services to competitors ever more widely. A second threat is real. Donald Trump does not care for the Washington Post, a newspaper Mr Bezos owns. In 2016 Mr Trump said Mr Bezos was using the Post to attack him because Amazon has “a huge antitrust problem”. If Mr Trump believes that—or even if he doesn’t—his administration might favour action.

For now, though, Amazon’s rivals must fend for themselves. They can hope Mr Bezos makes a mistake, or gets wrong-footed by some startling new trend—but though both are possible, they are hardly a strategy. Instead, the best defence is simple: sell something that customers want and Amazon does not have. Exceptional merchandise and service helps. In America big, bland bookstores are struggling, but the number of independent booksellers has climbed. The threat from Amazon has forced Walmart to improve its stores, with easier checkout and more helpful staff; it has seen a bump in sales. Amazon’s investments in television have helped fuel a bidding war for good programming—Hollywood’s studios are producing the best television for generations. And thanks to AWS, and its competitors, there has never been a better time to start up a web-based or data-centric firm.

For decades, consumer giants mostly grew slowly and comfortably, with only occasional bursts of innovation. Now Amazon’s epic journey is forcing companies to lower prices and to improve products or to suffer. Many may, as a result, become less profitable; many will instead improve.

And all the while, as Mr Wilke puts it, Amazon’s “pioneers wander the world with divine discontent and say, ‘how can I make that better today?’” Companies on its ever larger roster of rivals settle for mediocrity at their peril.

0 comments:

Publicar un comentario