America’s disproportionate weight in global stockmarket índices

Japan dominated the index in the late 1980s. That didn’t end well

,

THE aims of a stockmarket index are threefold. First, to reflect what is actually going on in the market; second, to create a benchmark against which professional fund managers can be judged; and third, to allow investors to assemble well-diversified, low-cost portfolios. On all three counts, there are reasons to worry about the MSCI All Country World Index, one of the most widely used gauges of the global stockmarket.

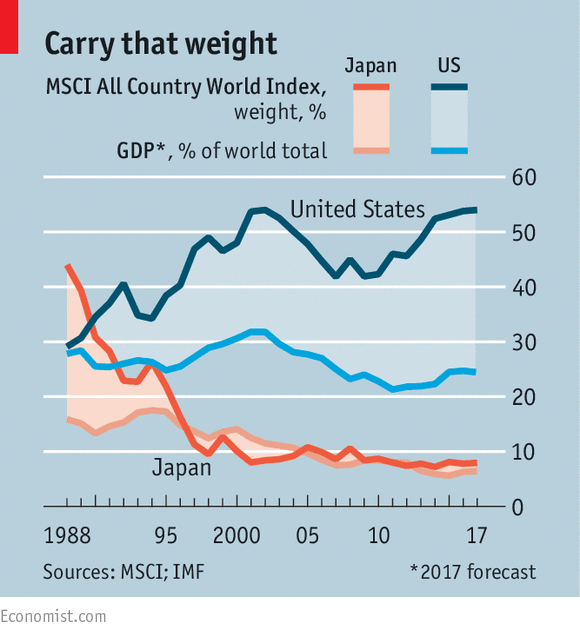

That is because the American market has a weighting of 54% in the index, as high as it has ever been (it reached the same level in 2002). In other words, anyone using the index to monitor the market is seeing a picture heavily distorted by Wall Street. The relative performance of international fund managers against the index will largely depend on how much exposure to America they are willing to take on. And anyone buying a tracking fund is making a big bet on the American market. Things are even worse if investors track the MSCI World Index, which covers only developed markets. In that benchmark, America’s weight is 60.5%.

There is nothing wrong with the way that MSCI calculates its indices; the weights reflect how America dominates global markets. With world index funds having fees as low as 0.3% a year, they look a tempting option. But there are worrying parallels with the way that Japan dominated the index in the late 1980s.

At its peak, the Japanese market was 44% of the MSCI index. That was far more than double the Asian economy’s share of global GDP at the time (see chart). Investors were enthusiastic about all-conquering Japanese multinationals like Toyota and Sony; the talk then was of the rest of the world needing to learn from the Japanese model. Japan’s companies were free from the threat of takeover and able to pursue long-term expansion plans without worrying about short-term profits. . The American stockmarket’s index weight is also more than double the country’s share of global GDP. The gap has widened since the start of the millennium, because America’s share of world GDP has been on a downward trend. Today’s investors are wildly enthusiastic about America’s all-conquering technology groups, such as Google, Facebook and Amazon. They, too, are either shielded from the threat of takeover by special shareholder structures, or in the case of Amazon, have persuaded investors that long-term growth is more important than short-term profits. Other countries only wish they could create technology giants with the same reach as one of America’s titans.

Do such parallels mean that America is doomed to follow the same path as Japan, whose stockmarket weight steadily dwindled until it fell back in line with its contribution to global GDP? Not necessarily. A country’s stockmarket is less likely to be an exact replica of its domestic economy; only around a half of the profits made by S&P 500 companies are earned at home. The weight of American firms in the global index has been given an extra boost by the recent strength of the dollar.

Still, investors may grant a higher valuation to a country’s stockmarket because they perceive it to have attractive fundamentals. The American market is nothing like as highly valued as Japan’s was in the late 1980s, when sceptics were told that Western valuation methods did not work in Tokyo. Still American companies trade on a multiple of 21 times last year’s earnings, compared with 18 for Europe, 17 for Japan and 14 for emerging markets. On a cyclically adjusted basis (averaging profits over ten years), the ratio of the American market to earnings is as high as it was in the bubble periods of the late 1920s and 1990s. And it is worth remembering that those corporate profits are still very high, relative to GDP, by historical standards.

Perhaps all these things can be justified. America may have better prospects for economic growth than the rest of the developed world, not least because of its favourable demography. Its technology giants may be less vulnerable to competition than the Japanese multinationals of the late 1980s because they benefit from “network effects”, or natural monopolies. And profits may have shifted to a higher level in a world where trade unions are weak, the cost of capital is low and business is very mobile.

Nevertheless, an investment in the MSCI indices is an implicit bet on three things: the importance of the American stockmarket; the valuation placed on American companies; and the robustness of profits as a proportion of American GDP. This is not the kind of lower-risk option which those buying an index-tracker probably have in mind.

0 comments:

Publicar un comentario