A 'Real Bubble' And A Really 'Big Short'

by: The Heisenberg

- One of 2017's biggest "consensus" trades is under (heavy) fire.

- The Fed's "dovish" messaging on Wednesday appears to have caught a whole bunch of shorts offsides.

- And while, as one trader put it, "there’s no immutable law that says crowded trades can’t work if they’re right," it certainly looks like this one may be decidedly "wrong.".

- Pick your side.

- The Fed's "dovish" messaging on Wednesday appears to have caught a whole bunch of shorts offsides.

- And while, as one trader put it, "there’s no immutable law that says crowded trades can’t work if they’re right," it certainly looks like this one may be decidedly "wrong.".

- Pick your side.

So late Friday, I outlined the two competing narratives on how the Fed views the post-hike rally in US equities.

In one camp are those who think the committee got exactly the outcome they wanted. That is, they squeezed in a hike, but didn't disrupt risk assets. The Fed put is alive and well.

That take on things has one distinct advantage: it conforms to common sense. This year's leg higher in equities has been driven by retail flows trying to catch the wave.

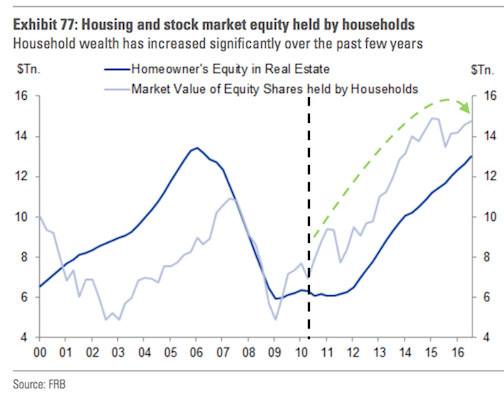

Part and parcel of post-crisis Fed policy has been a desire to improve household balance sheets by inflating the value of stock holdings. Setting aside one rather obvious criticism of that approach (i.e. that financial assets are concentrated in the hands of those who were better off in the first place and thus policies designed solely to inflate those assets will by definition exacerbate inequality), that effort has been pretty successful:

(Goldman)

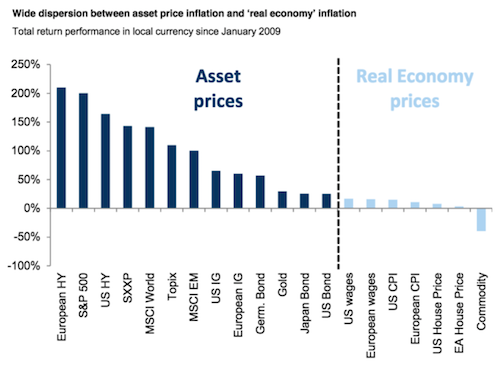

Of course real economy prices have gone nowhere comparatively speaking, but that's a debate for another post.

(Goldman)

The point is, it certainly looks like the ubiquitous "mom and pop" money is finally buying (literally) the "stocks can only go higher" narrative. Or at least that's the message we're getting from ETF flows.

Remember, the day after Trump's address to Congress on February 28, the SPDR S&P 500 Trust ETF (NYSEARCA:SPY) saw $8.2 billion in inflows - the biggest daily inflow since 2014.

Total inflows into equity ETFs sum to $66 billion YTD. As Martin Small, head of U.S. iShares told WSJ earlier this month:

It's unassailable that the retail investor is leading the way this year. If it continues at this pace, ETF growth will smash all previous records.

The last thing you want to do if you're the Fed is undercut that. Confidence is a fragile thing and if you go out and pull the rug out from under billions of retail money that just jumped into an overvalued market, you're likely to do serious damage to sentiment. And let me just tell you, sentiment is running pretty hot:

(BofAML)

Ok, so count me among those who think the Fed was willing to err on the side of caution in terms of putting a decidedly dovish spin on the messaging if that meant keeping risk assets buoyant. If the knock-on effect was to ease financial conditions further (i.e. effectively turn a hike into a cut as the charts below illustrate) then so be it.

(Goldman)

But as you're no doubt aware, guarding against a risk-off move had consequences for yields and the dollar. Specifically, Treasuries (NYSEARCA:TLT) rallied hard following Wednesday's hike and needless to say, the dollar plunged as falling yields undercut the rate differentials argument that supports the structurally strong dollar narrative.

This has created what I've called a tug-of-war between two competing narratives on rates.

The debate between those who argue that Wednesday's post-Fed plunge in yields has more room to run and those who are sticking with the short Treasurys reco is far more important than any discussion about whether and to what extent the Fed is happy with the reaction the committee got in stocks.

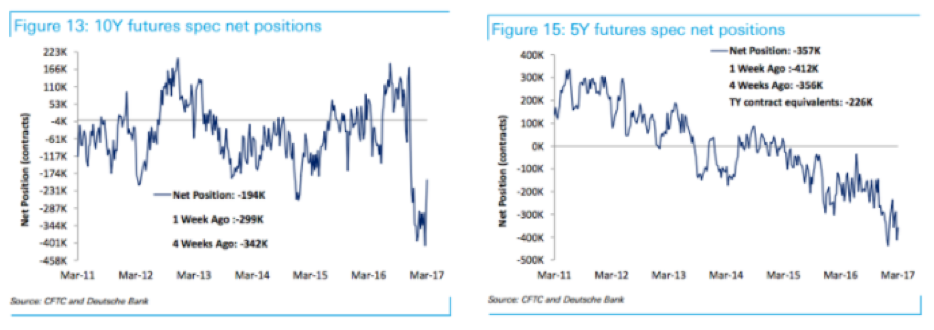

Short USTs was one of the consensus trades heading into 2017. And make no mistake, this is one "big short." As Deutsche Bank writes, in positioning data through Tuesday (so before the Fed), speculators "trimmed their net shorts in aggregate Treasury futures by 14K contracts in TY equivalents led by short covering in FV and TY of over 54K and 104K contracts, respectively."

(Deutsche Bank)

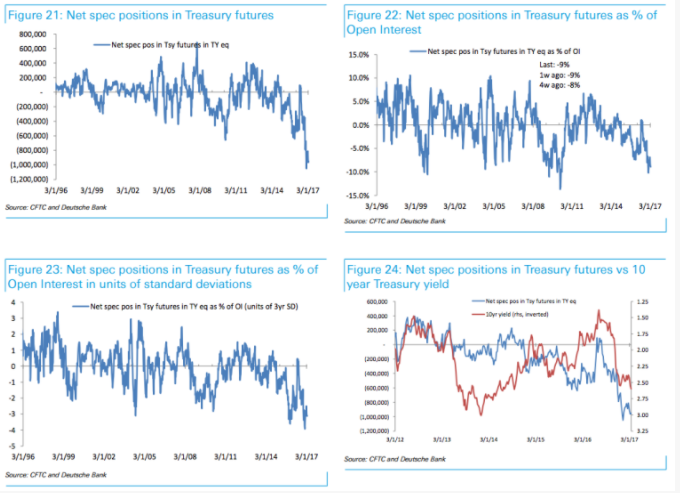

But as you can see, spec positioning is still one-sided. And indeed, as Deutsche goes on to note, "spec shorts as share of open interest was little changed [through Tuesday] at -8.9% and remained at about -3.1 standard deviations away from neutral."

(Deutsche Bank)

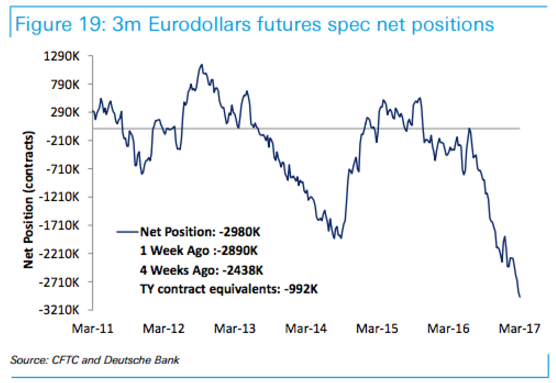

Additionally, specs also added to shorts in Eurodollar futures, taking the net position to new record of 2,980K contracts.

(Deutsche Bank)

Again, that's how positioning looked the day before the Fed. So it stands to reason that a whole lot of that money was caught offsides by the sharp repricing lower in yields following the Fed decision. As I politely reminded readers on Wednesday, I told you this was probably going to happen.

So that's what the short Treasury thesis looks like in practice. Now let's take a quick look at how some analysts and traders justify it. First is Bloomberg's Richard Breslow (my highlights):

Active traders are short bonds. I'm warned, therefore, to be careful of some massive rally. I'm skeptical. A market of this size will require a change of perceptions to be bullied for more than a very short amount of time by some short- covering. If people begin to think 10-year Treasuries are going north of 3%, do you really think there aren't enough longs to fill in the bids?

Crowded trades may indeed have structural buffers built in, may even have short-term corrections from panics, but there's no immutable law that says they can't work if they're right.

That's true. And at least as far as real rates go, Deutsche Bank certainly seems to agree. Here are some excerpts from a piece out Friday called "The 'Real' Bubble" (my highlights):

We see real rates as extremely misvalued if not in a bubble. Real rates are far below (-2pp) levels implied by prevailing GDP growth rates, which have historically provided an anchor. Monetary policy has been the key driver of this divergence. If monetary policy had been set in keeping with its historical reaction function, prevailing growth and inflation would have policy rates at 3.5% today.

The key to a normalization of real rates is higher market expectations of the speed and eventual level to which the Fed will hike policy rates. Market expectations remain well below the Fed's guidance. But this is typical, with past hiking cycles seeing significant repricings and average price losses on the 10y of -11% (at current duration 120bps on the 10y). The Fed simply sticking to its guidance should see market expectations move up, but this will take a few hikes and is more likely around the June meeting. We expect a more clearly apparent upward trajectory in core inflation later this year to make the Fed more anxious and reiterate or up its guidance. This is more likely around the September or December meetings. Our asset allocation remains underweight duration.

You can add (rumored) ECB tapering/rate hikes, fiscal stimulus expectations in the US, and a Marine Le Pen loss in the French elections to the list of possible catalysts for rising rates. Here's SocGen:

You can add (rumored) ECB tapering/rate hikes, fiscal stimulus expectations in the US, and a Marine Le Pen loss in the French elections to the list of possible catalysts for rising rates. Here's SocGen:We think the bear-steepening dynamic may find further support from a scenario whereby Trump starts to pivot decisively toward a pro-growth agenda, the outcome of the French elections proves positive for risk sentiment and the March ECB meeting keeps the door open to our economists' 2H tapering scenario.

So that's all fine and good, but as I wrote on Friday, this all depends on your outlook. To wit:

Essentially it comes down to this: do you think the outlook for global growth and inflation supports higher yields or do you not? And if you do, do you think it's at least possible that your outlook, even if correct, could be undercut by a short squeeze because there's a … ummm… let's just call it 3-sigma… short in the belly of the curve that's just waiting to be screwed by huge rallies like we saw on Wednesday.

Which brings us to the counterargument. Here's Bloomberg's Wes Goodman (my highlights):

Two-year break-even rates and oil prices are plunging, underscoring concern the Fed has yet to end the risk of disinflation.

Benchmark 10-year yields have failed to hold above 2.6 percent, the level bond market guru Bill Gross said will signal the start of a bear market if sustained on a weekly basis. Instead of breaking to higher levels, rising yields are drawing demand.

Treasuries offer a growing premium over their peers. U.S. two-year notes yielded as much as 223 basis points over like-maturity German securities earlier this month, the biggest spread since 2000 and another reason to favor U.S. debt.

There will be many different issues to focus on from this meeting - the dot plot, the phrasing around the balance of risks, and any mention of balance sheet management - so the short-term reaction may be volatile. Don't be scared off by any initial yield spike.

Well Wes needn't have worried. Those comments hit the wires on Wednesday morning and as noted above, there was no "initial spike." Indeed, yields did exactly what they did following the last two rate hikes:

Some of what you saw following Wednesday's "dovish" hike was undoubtedly short covering (which, you're reminded, wouldn't show up in the CFTC positioning data cited above). Here's what Barclays (who has a long duration view) said on Thursday:

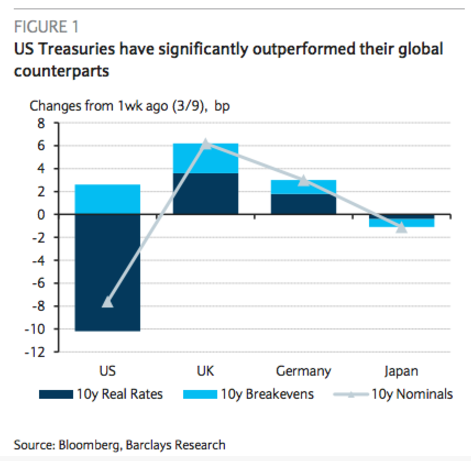

The Treasury market outperformed its global counterparts over the week despite a Fed hike and reduced political uncertainty in the euro area. The March FOMC meeting was perceived as dovish as investors were likely looking for the Fed to signal the possibility of four hikes this year or at least indicate the possibility of balance sheet reduction later in the year. Short covering also likely exacerbated the rally.

"The Dutch elections resulted in a Eurofriendly outcome with preliminary results showing the incumbent VVD party significantly outperforming Geert Wilder's PVV [causing] the market-implied probability of Marine Le Pen winning the French elections to decline," the bank goes on to note, adding that "Figure 1 shows that real yields fell sharply in the US while rising in the UK and Germany, reflecting these developments."

So again, we see the tug-of-war, and those comments underscore the point made above by SocGen. That is, as political risk wanes in Europe, you'll see long-end rates rise (underpinning underweight duration positions). But the Fed's message pushed in the opposite direction. That is, the dovish slant pushed US yields lower. This juxtaposition is reflected in the chart above.

Here's a bit of further color on why the short Treasurys thesis might be misguided, from Bloomberg's Mark Cudmore (my highlights):

[I] argued that long-end yields would fall after the Fed hike. An 11 basis-point drop in 10-year Treasury yields on Wednesday might seem significant, but it's not in the context of what happened at the meeting.

Apart from lower commodity prices, solid but not exceptional economic growth, and a lack of runaway inflation, much of my anticipation of a dovish market reaction was based on the fact that the market was very much positioned the other way.

But Yellen didn't just disappoint the extremely hawkish hopes - she genuinely wasn't hawkish at all. Not only did the median dot plot not rise above 3 hikes in 2017, but the average barely rose. Four hikes weren't even a near miss - it wasn't even on the radar of the majority.

Everything about this meeting that could surprise dovishly, managed to do so. U.S. yields and the dollar have much further to fall as a result.

If that's true, the 3-sigma Treasury short depicted in the CFTC positioning charts shown at the outset will be caught wrong-footed. And by "wrong-footed" I mean badly offsides.

Bloomberg's Richard Breslow may be right. That is, a market the size of the Treasury market may simply prove too large to be pushed around by some short-covering. But remember how Breslow kind of tries to hedge his comments by saying "if people begin to think 10-year Treasuries are going north of 3%."

Wednesday's Fed messaging made that a big "if".

If the market's underlying assumption about the trajectory of yields gets calibrated lower, well then a short squeeze will simply exacerbate a rally.

At the end of the day this is pretty simple. This is either a "real bubble" (as Deutsche Bank puts it) and thereby a great opportunity to capitalize on a sharp repricing higher of yields by the "big short" we're seeing in the positioning data, or this is a crowded trade that is going to turn into a veritable blood bath if there's a sustained bid for US paper or worse (for the shorts) a flight to safety bid triggered by some kind of risk-off event.

0 comments:

Publicar un comentario