Whatever happened to secular stagnation?

By: Gavyn Davies

A year ago, Lawrence Summers’ perceptive warnings about the possibility of secular stagnation in the world economy were dominating global markets. China, Japan and the Eurozone were in deflation, and the US was being dragged into the mess by the rising dollar. Global recession risks were elevated, and commodity prices continued to fall. Fixed investment had slumped. Productivity growth and demographic growth looked to be increasingly anemic everywhere.

Estimates of the equilibrium real interest rate in many economies were being marked down. It seemed possible that the world economy would fall into a “Japanese trap”, in which nominal interest rates would be permanently stuck at the zero lower bound, and would therefore not be able to fall enough to stimulate economic activity.

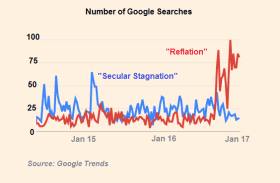

Just when the sky seemed to be at its darkest, the outlook suddenly began to improve. Global reflation replaced secular stagnation as the theme that dominated investor psychology, especially after Donald Trump’s election in November. Why has secular stagnation lost its mass appeal, and has it disappeared forever? Was it all a case of crying wolf?

Lawrence Summers has always made it clear that in his mind secular stagnation was a hypothesis, not a proven reality, especially in the US. He and others have argued that the combination of very low global GDP growth, alongside falling real interest rates, could be caused by two factors: (i) inadequate global demand, stemming from low business investment, high savings rates in Asia, wide disparity in income distribution and rising risk aversion; and (ii) inadequate global supply, stemming from falling productivity growth, and slowing growth in the labour force.

With fears of deflation on the increase until early in 2016, it seemed that the weakness in demand was the more powerful force, although there was plenty of evidence of slowing growth in supply as well. Since inadequate demand growth seemed to be the main problem, and since the efficacy of monetary stimulus was being widely questioned, those economists who believed in secular stagnation frequently argued that fiscal stimulus was needed to rectify the problem.

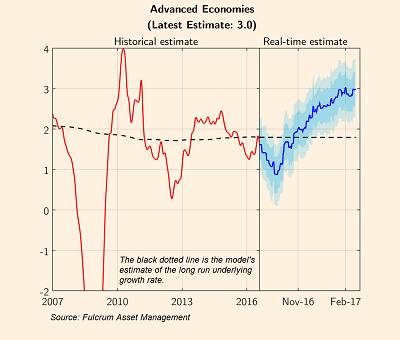

What has happened since to change the market’s level of concern about secular stagnation? The flow of incoming economic data has clearly changed a lot, as shown in our monthly update of the Fulcrum nowcast models, attached here.

Global activity growth has rebounded sharply, and recession risks have plummeted. Growth in real output is now running at higher levels than anything seen since the temporary rebound from the financial crash in 2009/10. Importantly, recent data suggest that the growth rate of fixed investment is beginning to recover, which is a body blow to one of the central tenets of the secular stagnation school, though much of this may simply be due the end of the slump in the commodity sector.

This recovery in real activity has not yet led to any rebound in long run underlying growth, according to the models. There has been no improvement in the growth of the labour force, and little rise in labour productivity growth, in the advanced economies in the last year. It therefore seems reasonable to conclude that the vast majority of the rise in real output growth has been due to improving aggregate demand, not aggregate supply.

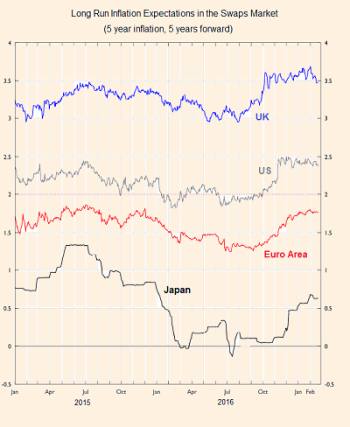

The conclusion that global data have improved because of demand factors is also supported by the rise in inflation expectations that has occurred in all the main economies in the past 12 months. The increases in US and UK inflation expectations are not surprising, since both of these economies are operating very close to full employment. But the increases in Japan and the Eurozone are more impressive. These were the two economies that seemed to be completely stuck in secular stagnation due to excess capacity a year ago. Now, they seem to be escaping.

Up to a point, these escapes seem to be due to the success of macro-economic policies that were aimed to correct secular stagnation. The Fed postponed its plan to raise interest rates, so US short rates are about 75 basis points below the levels threatened a year ago. The Bank of Japan introduced a 10 basis points ceiling on 10 year government bond yields, an initiative that has appeared more successful than some of its earlier efforts to stimulate the economy. The ECB maintained and extended its programme of quantitative easing, and this has succeeded in normalising monetary conditions throughout the euro area.

On fiscal policy, the changes were not huge, but they were definitely in the direction of expansion. According to the IMF, the stance of fiscal policy in the advanced economies in 2016 was 0.7 percent of GDP more stimulatory than planned a year ago. Furthermore, the election of Donald Trump greatly increased expectations of future easing in US fiscal policy, boosting business and household optimism about growth prospects.

All this suggests that stimulatory macro-economic policy may finally be working and that the secular stagnation scare might now be over. But that is probably too optimistic. Although there has been a cyclical improvement in demand in the advanced economies, there is no reason yet to believe that the supply side of the global economy is performing any better than it was a year ago. The secular speed limit on growth in the advanced economies is still much lower than it was in earlier decades. This speed limit has yet to be seriously tested but that may happen soon in the US and the UK.

In any case, the recent spurt in growth in the advanced economies may turn out to be another false dawn, rather than the achievement of “escape velocity”. Even if escape velocity is achieved, and proves sustainable, it would need to prove that it can be maintained in the face of the policy tightening that would surely follow.

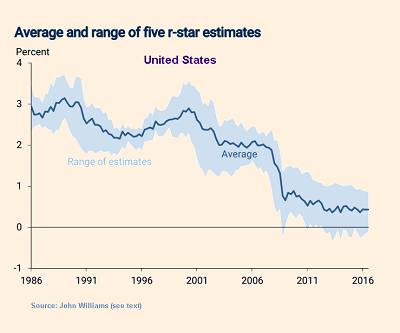

Last week, the President of the San Fancisco Fed, John Williams, released a paper on the decline in the equilibrium real interest rate in the US (r*), the concept that has been at the heart of the secular stagnation debate. This paper concluded that low r-star is a global phenomenon, is likely to be very persistent, and is not confined only to safe assets.

In other words, a cyclical recovery in demand, especially if confined mainly to the US, is unlikely to banish the problem of secular stagnation for very long.

0 comments:

Publicar un comentario