The Greatest Fool Is Here

by: Eric Parnell, CFA

- Investors think stocks are expensive.

- Yet investors are as optimistic about future returns as they have ever been.

- This is a combination that does not end well at all.

- The Greatest Fool is here.

- Yet investors are as optimistic about future returns as they have ever been.

- This is a combination that does not end well at all.

- The Greatest Fool is here.

A notable divergence is taking place in the U.S. stock market. A growing percentage of investors believe that stock valuations are too high. Yet a record number of investors also think that stock prices will be higher one year from now. Such is a toxic brew of sentiment that potentially does not end well.

Overconfidence

The Investor Behavior Project at Yale University under the direction of Professor Robert Shiller publishes four different stock market confidence indices for the United States. Two of these four confidence indices are known as the U.S. Valuation Confidence Index and the U.S. One-Year Index.

And the themes implied by the latest data from these indices suggest a stock market filled with investors that are becoming increasingly disconnected from rationale and reality.

That's Rich

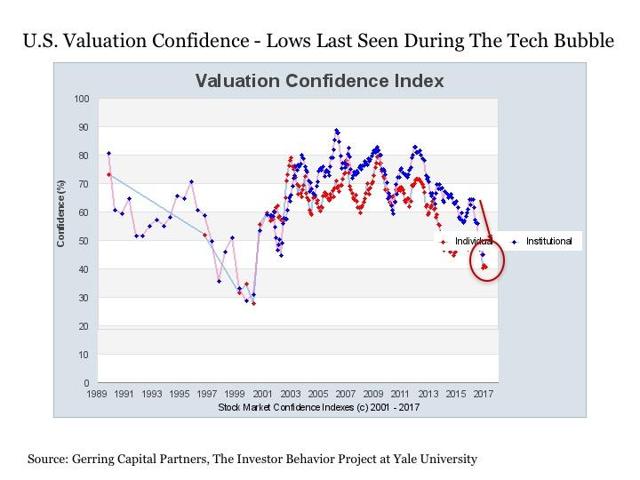

Let's first consider the U.S. Valuation Confidence Index, which is shown the chart below. This index is based on a question asked to both institutional and wealthy individual investors regarding stock prices (NYSEARCA:SPY) and how they are priced when compared to "true fundamental value" or "sensible investment value." The Index measures the percentage of the survey population that thinks the stock market is not too high from a valuation perspective.

Thus, the lower the reading, the more respondents think the stock market is overvalued.

Historically, roughly 68% of institutional investors and 62% of wealthy individuals on average have viewed stock market (NASDAQ:QQQ) values as not too high at any given point in time.

As recently as one year ago in March 2016, a reasonable 64% of institutional investors believed stock valuations were at least reasonable. Wealthy individual investors were notably more skeptical a year ago, but were still evenly split at 50% about stock valuations.

Following the strong run higher in stocks since November, the percentage of institutional and individual investors that think today's stock market (NYSEARCA:DIA) is either attractively valued or simply just reasonably valued has plunged over the past year. Today, only 47% of institutional investors believe stock prices are not too high. And just over 40% of individual investors view stocks as not being too expensive today.

For individual investors, this 40% reading is the lowest the U.S. Valuation Confidence Index has been since April 2000, which was effectively at the peak of the technology bubble. As for marginally more optimistic institutional investors, the 47% reading also is the lowest it has been since the midst of the bursting of the tech bubble in the early 2000s.

Put simply, both institutional and wealthy individual investors view stocks (NYSEARCA:IVV) as about as expensive as they have been in a long time. The last time either group thought they were this expensive, the stock market proceeded to fall into a painful bear market.

Complacency

Now given that a notable majority of both institutional and wealthy individual investors believe that stock prices are currently too high based on valuation, one would reasonably think that these same investors might have a pessimistic or at least a more measured view about the prospects for stock market (NYSEARCA:VOO) returns over the coming year. After all, if stocks are currently expensive in the view of many, a subsequent correction in the year ahead might be a logical conclusion in order to correct for this implied overvaluation. But this is not at all the case. Instead, investors are almost certain that the exact opposite is going to happen.

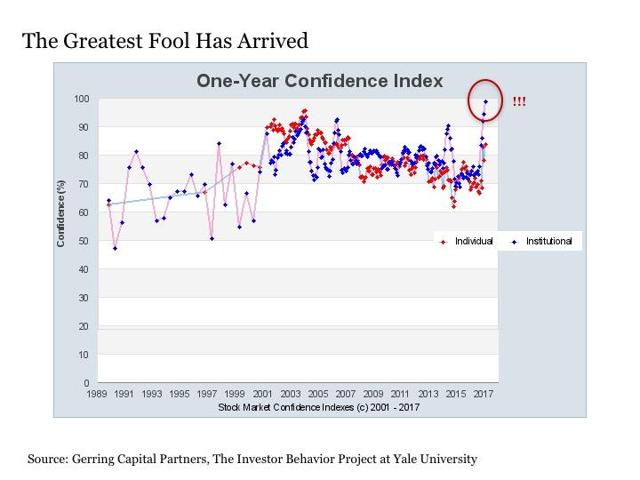

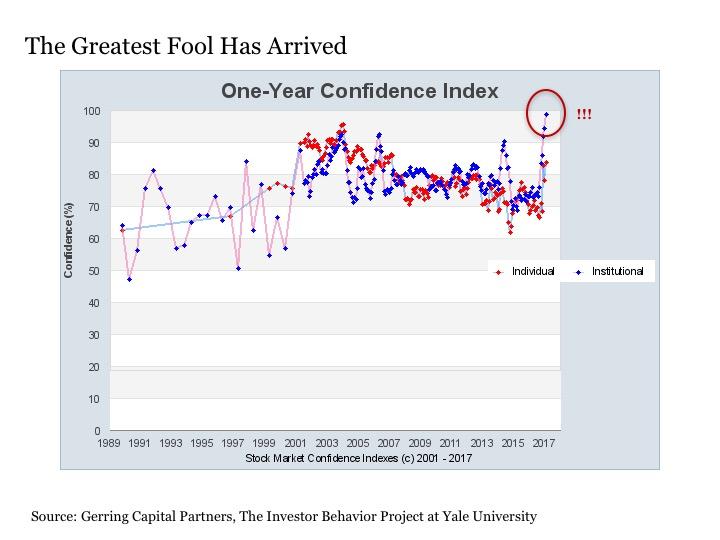

Consider the U.S. One-Year Confidence Index, which is shown in the chart below. This index is based on a question asked to both institutional and wealthy individual investors that effectively determines the percentage of survey respondents that believe that stocks will be trading higher one year from now. Thus, the higher the reading, the more confidence among respondents that the stock market will be higher a year from now.

Stock investors are a famously optimistic lot, which is shown in the historical average data.

Overall, 78% of institutional investors and 79% of wealthy individual investors on average believe that the stock market will be trading higher one year later at any given point in time.

But where we are today is absolutely remarkable.

Among wealthy individual investors, nearly 84% of respondents believe stocks will be trading higher one year from now. This is the highest reading on the individual side since March 2007 just before the outbreak of the financial crisis.

What about the institutional side? Hold onto your hats. As of February 2017, an incredible 99% of survey respondents declared that the stock market would be trading higher one year from now. This is a reading that implies near unanimity among the institutional investor community. Needless to say, this is the highest reading in the history of the index by a healthy margin.

No More Fools

First, let's debunk a notion that I repeatedly hear expressed in the financial media. It is a common perception that investors remain shell shocked from the financial crisis, with many still hiding out in their bunkers surrounded by a stockpile of cash. Maybe this is true on an anecdotal basis, but based on the U.S. One-Year Confidence Index numbers, both institutional and wealth individual investors got over the financial crisis a while ago. Heck, I'm guessing many don't even remember it anymore if they were even participating in the markets back then nearly a decade ago.

Now, let's consider what the data is currently saying. Put simply, if ever I needed a single data point to express my bearish view on the U.S. stock market, the U.S. One-Year Confidence Index for institutional investors would be a very good candidate. Why? Because this reading alone is showing in data form that the institutional market has effectively run out of buyers. After all, if an institutional investor thinks that stocks are going to be trading higher a year from now, they will be invested accordingly. And if 99% of already investors feel that way, who is the institutional investor that is not already in the market that is going to come in and buy more to keep stock prices moving higher?

In short, the greatest fool has effectively arrived for the institutional stock investor marketplace.

Perhaps the remaining wealthy individual investors can fill the remaining gap in the very near term, but the fact that this group is already historically optimistic in their own right suggests that they may also be all in at this point as well.

What makes this greatest fool risk all the more disconcerting is that it is playing out at a time not when stock valuations are perceived to be reasonable if not attractive. Instead, it is occurring at time when a historically high majority of both institutional and wealthy individual investors believe that stocks are too expensive.

All of this implies a toxic combination. Nearly everyone is bullish, thus leaving nobody new to join the game to take on the hot potato of already expensive stock prices. And given that a majority of participants in the game know that the stocks they are holding are already too expensive, they at some point may decide to seize the first mover advantage in dumping their shares ahead of the rest.

Such is the danger of the momentum trade that has carried the stock market to such great heights in recent years. Unlike rising stock prices based on fundamentals, once the momentum trade fizzles out, the subsequent downside is painful and relentless. Those who remember the technology bubble, you know exactly what I am talking about. For just as momentum can cause stocks to overshoot wildly to the upside, so too can it cause stocks to overshoot crushingly to the downside.

The key question for stock investors is when. But with the greatest fool potentially having arrived at a time when the Fed has suddenly found its long lost swagger to storm in and steal away the punch bowl, such an inflection point for the momentum trade may finally be coming sooner rather than later.

Strategy Implications

Does this mean sell stocks today? No. But what it does mean is to not get complacent. Stocks may continue to run to the upside in the near term. And there is still a healthy percentage of stock investors who are dying to buy the first solid dip in stock prices after so many months of relentless gains. This buyer is likely to come from the institutional side - the U.S. Buy-On-Dips Confidence Index is running at the high end of the historical range for institutional investors at 64% but at the low end of the historical range for wealthy individual investors at just 52% - but they will give those who are long and currently riding high on the momentum trade a window of opportunity to scale back equity allocations if needed.

With this in mind, the key to emerging largely unscathed from any future market downturn is to avoid becoming complacent. For those who are standing ready and aware with a risk control action plan in place should fare just fine if not capitalize. Those who are complacent and not paying attention to the downside risks, on the other hand, are those who likely will find themselves trapped in the clutches of the next bear market wondering in retrospect how they possibly could have ever seen it coming.

Overconfidence

The Investor Behavior Project at Yale University under the direction of Professor Robert Shiller publishes four different stock market confidence indices for the United States. Two of these four confidence indices are known as the U.S. Valuation Confidence Index and the U.S. One-Year Index.

And the themes implied by the latest data from these indices suggest a stock market filled with investors that are becoming increasingly disconnected from rationale and reality.

That's Rich

Let's first consider the U.S. Valuation Confidence Index, which is shown the chart below. This index is based on a question asked to both institutional and wealthy individual investors regarding stock prices (NYSEARCA:SPY) and how they are priced when compared to "true fundamental value" or "sensible investment value." The Index measures the percentage of the survey population that thinks the stock market is not too high from a valuation perspective.

Thus, the lower the reading, the more respondents think the stock market is overvalued.

Historically, roughly 68% of institutional investors and 62% of wealthy individuals on average have viewed stock market (NASDAQ:QQQ) values as not too high at any given point in time.

As recently as one year ago in March 2016, a reasonable 64% of institutional investors believed stock valuations were at least reasonable. Wealthy individual investors were notably more skeptical a year ago, but were still evenly split at 50% about stock valuations.

Following the strong run higher in stocks since November, the percentage of institutional and individual investors that think today's stock market (NYSEARCA:DIA) is either attractively valued or simply just reasonably valued has plunged over the past year. Today, only 47% of institutional investors believe stock prices are not too high. And just over 40% of individual investors view stocks as not being too expensive today.

For individual investors, this 40% reading is the lowest the U.S. Valuation Confidence Index has been since April 2000, which was effectively at the peak of the technology bubble. As for marginally more optimistic institutional investors, the 47% reading also is the lowest it has been since the midst of the bursting of the tech bubble in the early 2000s.

Put simply, both institutional and wealthy individual investors view stocks (NYSEARCA:IVV) as about as expensive as they have been in a long time. The last time either group thought they were this expensive, the stock market proceeded to fall into a painful bear market.

Complacency

Now given that a notable majority of both institutional and wealthy individual investors believe that stock prices are currently too high based on valuation, one would reasonably think that these same investors might have a pessimistic or at least a more measured view about the prospects for stock market (NYSEARCA:VOO) returns over the coming year. After all, if stocks are currently expensive in the view of many, a subsequent correction in the year ahead might be a logical conclusion in order to correct for this implied overvaluation. But this is not at all the case. Instead, investors are almost certain that the exact opposite is going to happen.

Consider the U.S. One-Year Confidence Index, which is shown in the chart below. This index is based on a question asked to both institutional and wealthy individual investors that effectively determines the percentage of survey respondents that believe that stocks will be trading higher one year from now. Thus, the higher the reading, the more confidence among respondents that the stock market will be higher a year from now.

Stock investors are a famously optimistic lot, which is shown in the historical average data.

Overall, 78% of institutional investors and 79% of wealthy individual investors on average believe that the stock market will be trading higher one year later at any given point in time.

But where we are today is absolutely remarkable.

Among wealthy individual investors, nearly 84% of respondents believe stocks will be trading higher one year from now. This is the highest reading on the individual side since March 2007 just before the outbreak of the financial crisis.

What about the institutional side? Hold onto your hats. As of February 2017, an incredible 99% of survey respondents declared that the stock market would be trading higher one year from now. This is a reading that implies near unanimity among the institutional investor community. Needless to say, this is the highest reading in the history of the index by a healthy margin.

No More Fools

First, let's debunk a notion that I repeatedly hear expressed in the financial media. It is a common perception that investors remain shell shocked from the financial crisis, with many still hiding out in their bunkers surrounded by a stockpile of cash. Maybe this is true on an anecdotal basis, but based on the U.S. One-Year Confidence Index numbers, both institutional and wealth individual investors got over the financial crisis a while ago. Heck, I'm guessing many don't even remember it anymore if they were even participating in the markets back then nearly a decade ago.

Now, let's consider what the data is currently saying. Put simply, if ever I needed a single data point to express my bearish view on the U.S. stock market, the U.S. One-Year Confidence Index for institutional investors would be a very good candidate. Why? Because this reading alone is showing in data form that the institutional market has effectively run out of buyers. After all, if an institutional investor thinks that stocks are going to be trading higher a year from now, they will be invested accordingly. And if 99% of already investors feel that way, who is the institutional investor that is not already in the market that is going to come in and buy more to keep stock prices moving higher?

In short, the greatest fool has effectively arrived for the institutional stock investor marketplace.

Perhaps the remaining wealthy individual investors can fill the remaining gap in the very near term, but the fact that this group is already historically optimistic in their own right suggests that they may also be all in at this point as well.

What makes this greatest fool risk all the more disconcerting is that it is playing out at a time not when stock valuations are perceived to be reasonable if not attractive. Instead, it is occurring at time when a historically high majority of both institutional and wealthy individual investors believe that stocks are too expensive.

All of this implies a toxic combination. Nearly everyone is bullish, thus leaving nobody new to join the game to take on the hot potato of already expensive stock prices. And given that a majority of participants in the game know that the stocks they are holding are already too expensive, they at some point may decide to seize the first mover advantage in dumping their shares ahead of the rest.

Such is the danger of the momentum trade that has carried the stock market to such great heights in recent years. Unlike rising stock prices based on fundamentals, once the momentum trade fizzles out, the subsequent downside is painful and relentless. Those who remember the technology bubble, you know exactly what I am talking about. For just as momentum can cause stocks to overshoot wildly to the upside, so too can it cause stocks to overshoot crushingly to the downside.

The key question for stock investors is when. But with the greatest fool potentially having arrived at a time when the Fed has suddenly found its long lost swagger to storm in and steal away the punch bowl, such an inflection point for the momentum trade may finally be coming sooner rather than later.

Strategy Implications

Does this mean sell stocks today? No. But what it does mean is to not get complacent. Stocks may continue to run to the upside in the near term. And there is still a healthy percentage of stock investors who are dying to buy the first solid dip in stock prices after so many months of relentless gains. This buyer is likely to come from the institutional side - the U.S. Buy-On-Dips Confidence Index is running at the high end of the historical range for institutional investors at 64% but at the low end of the historical range for wealthy individual investors at just 52% - but they will give those who are long and currently riding high on the momentum trade a window of opportunity to scale back equity allocations if needed.

With this in mind, the key to emerging largely unscathed from any future market downturn is to avoid becoming complacent. For those who are standing ready and aware with a risk control action plan in place should fare just fine if not capitalize. Those who are complacent and not paying attention to the downside risks, on the other hand, are those who likely will find themselves trapped in the clutches of the next bear market wondering in retrospect how they possibly could have ever seen it coming.

0 comments:

Publicar un comentario