The ETF Illusion: An Inside Look

by: The Heisenberg

- Bond ETFs - and especially the high yield variety - should come with a bright, red "buyer beware" stamp on the prospectus.

- But they don't. Which means it's up to you to do the research and understand what the risks are.

- Herein find my most comprehensive look at ETF liquidity to date.

- But they don't. Which means it's up to you to do the research and understand what the risks are.

- Herein find my most comprehensive look at ETF liquidity to date.

Ok, today's the day.

I've been trying to free up some time to write this post for nearly a week, and I keep putting it off because between French election drama and a veritable deluge of new research from analysts looking to quantity the chances of an equity market selloff, there's simply been too much going on for me to refocus on what very well might be my favorite topic: bond market liquidity and the danger posed by corporate credit ETFs.

To be sure, we've been down this road before. Regular readers will recall Heisenberg's Labradors (here and here) and the series of posts that came later.

The thrust of the argument is as follows.

Corporate bond ETFs create what I like to call "phantom liquidity." What you see (or what you think you see) is not in fact what you get. This problem is especially acute in high yield ETFs like the iShares iBoxx $ High Yield Corporate Bond ETF (NYSEARCA:HYG) and the SPDR Barclays Capital High Yield Bond ETF (NYSEARCA:JNK).

In the post-crisis regulatory environment, dealers aren't willing to serve as middlemen - the cost of balance sheet is simply too high. What that means, in the simplest possible terms, is that in a pinch, no one is going to be willing to catch a falling knife or, in market parlance, "inventory" these bonds.

This creates a very real problem that the vast majority of ETF holders do not fully comprehend.

Consider the following excerpt from a 2016 Vanguard report amusingly called "ETFs: Clarity Amid The Clutter":

The creation and redemption mechanisms help ETF shares trade at a price close to the market value of their underlying assets. When rising demand for the shares causes them to trade at a higher price (i.e., at a premium), the AP may find it profitable to create shares by buying the underlying securities, exchanging them for ETF shares and then selling those shares into the market. Similarly, when falling demand for the ETF shares causes them to trade at a lower price (i.e., at a discount), an AP may buy shares in the secondary market and redeem them to the ETF in exchange for the underlying securities. These actions by APs, commonly described as "arbitrage activities", help keep the market-determined price of an ETF's shares close to the market value of the underlying assets.Ok, so this is one of those times when you have to "just step back from it" (to quote Sgt. Jeffrey 'Jeff' Rabin in the "Usual Suspects").

That is, don't get bogged down in the lingo or let yourself be blinded by the technicalities because that's precisely what Vanguard does in the paper from which that excerpt is taken and it's precisely why they don't seem to understand the inherent risk here.

What that passage basically says is that in the event there's a lot of selling pressure in a particular ETF causing the shares to trade below the supposed value of the underlying assets (in this case bonds), broker-dealers are going to arb away that difference by buying the ETF shares at a discount, exchanging them for those underlying assets, and (implicitly) pocketing the spread.

Do you see a conceptual problem with that? I say "conceptual" because again, I'm not an ETF sponsor, so I'm not here to try and do a deep dive into the technicalities of this and/or try and quantify the extent to which this mechanism works on a daily basis. I don't care about that because obviously, I'm not talking about what happens on a daily basis. I'm talking about what would happen should something go wrong. When we start thinking in those terms, what was merely "conceptual" very often becomes reality.

So with that in mind think again about this statement from the Vanguard report (my highlights):

When falling demand for the ETF shares causes them to trade at a lower price (i.e., at a discount), an AP may buy shares in the secondary market and redeem them to the ETF in exchange for the underlying securities.As I put it a few weeks ago in "'How Do You Sell It?' Vanguard Misses The Point On ETFs": "I'm not entirely sure how willing broker-dealers would be to arb this in a panic."

I mean think about it: would you want to try and arbitrage that disconnect if it meant taking on the balance sheet risk associated with exposing yourself to the underlying bonds? Probably not.

So having reviewed the back story here, I want to draw your attention to some new commentary from Barclays, whose analysts penned one of the most enlightening takes on this entire debate way back in June of 2015.

Let's start with a review of an important concept. I've paraphrased the above mentioned Barclays note (the one from 2015) so many times that I'm afraid we might be subject to the "Chinese whispers" effect, so I went back and dug up the original note.

The excerpts that follow are from the June 2015 Barclays piece. What you're about to read is a lengthy quote. It's lengthy on purpose. It is quite literally impossible to overstate how important this is for high yield ETF investors to understand. I'm not going to highlight anything here because frankly, it should all be highlighted. I strongly encourage you to read every word - maybe twice. To wit:

Are ETFs good or bad for corporate bond liquidity? In our view, the answer depends on the correlation of flows at the individual fund level. Although fund flows have been a major focus of market participants over the past several years, the aggregate flows attract the most attention. This is particularly true in the high yield market, where retail ownership is relatively high and the price swings associated with contemporaneous fund flows have been well documented.

Aggregate flows have effectively become a market signal.

However, fund managers actually have to manage their particular inflows and outflows, not the aggregate flows. From the perspective of an individual fund manager, the risk posed by fund flows and the strategies available to help mitigate that risk depend to a large extent on the correlation of flows across funds. If flows are highly correlated then the risk is relatively high. Funds will have a difficult time selling bonds when they experience an outflow, since other managers would similarly be selling. In this circumstance, managers have a relatively short list of strategies to deal with flows. They can keep increased cash on hand, or (less likely) they can hope that other non-retail buyers step into the market at a reasonable discount to market levels.

On the other hand, if flows are relatively uncorrelated they may, in principle, pose less of a risk - funds with outflows can sell to those with inflows. Funds can exchange bonds (or portfolio products, see below) with other funds, rather than draw down on or build cash. This process may be made more difficult by the decline in liquidity, but the price discount/premium faced by an individual fund with an inflow or outflow could, theoretically, be limited by the existence of investors looking to go in the opposite direction.

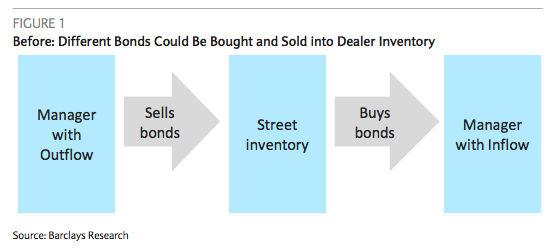

While diversifiable flows limit the risks to portfolio managers in principle, the reality of the high yield market is more complicated. Managers have specific views on tenor, callability, sectors, covenants, and, most importantly, individual credits, such that actually finding buyers for specific bonds can be quite difficult. In the pre-crisis period, dealers ran large inventories that effectively facilitated the netting of flows across funds (Figure 1). A fund with an outflow would sell bonds into the dealer community, and funds with outflows would buy bonds out of the dealer inventory. When inventory is large, the fact that the specific bonds bought and sold did not match was largely irrelevant. Funds with outflows could sell the bonds of their choice, and the funds with inflows could pick investments from the large variety of inventory held by dealers.

The matching problem has become more acute as dealer inventories have declined.

Even if funds can net flows in principle, dealers are much less willing to warehouse bonds, and are much more likely to buy only when they believe they can quickly offload the risk. Under this scenario, the fact that flows can theoretically be netted is of little practical use to fund managers - actually netting individual bonds is extremely difficult, particularly in the short time frame required by funds offering daily liquidity to end investors. This is where portfolio products come in. Investors can use portfolio products to fund outflows/invest inflows immediately and execute the necessary single-name bond trades over time as liquidity in the underlying bond market allows (Figure 2). In this scenario, funds with inflows and outflows simply exchange portfolio products, sidestepping (the immediate need to trade single-name corporate bonds.Do you see what's going on here?

No one is trading the high yield bonds that underpin these ETFs. When your fund manager experiences an outflow, he/she can effectively dodge the underlying bond market by trading ETF shares with another fund manager who is experiencing inflows.

This is what Vanguard means when they say things like this (my highlights):

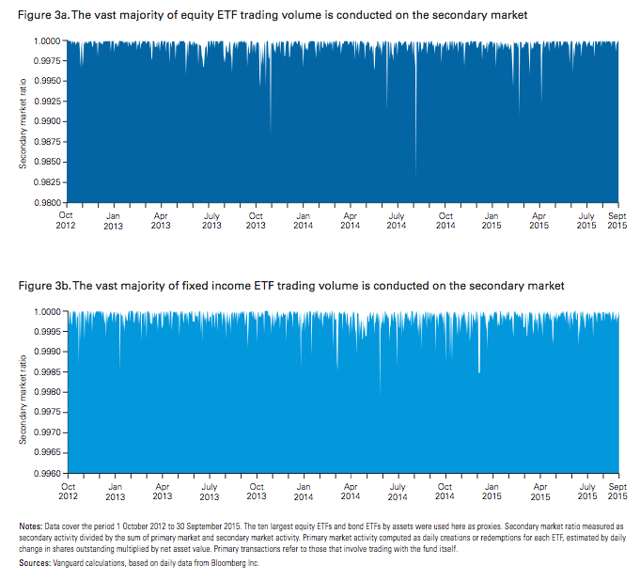

Figure 3a shows the percentage of daily equity ETF trading volume conducted solely on the secondary market. The median ratio was 99%, suggesting that for every €1 in trading volume, only 1 cent resulted in primary market trading. Put another way, 99% of the trading volume resulted in no portfolio management impact and no trading in underlying securities (Figure 3b shows the same analysis for bond ETFs - the median ratio here was also 99%).

Notice how Vanguard is pitching this as a good thing. As I explained in what is now the most read piece in the short history of the Heisenberg Report, it is most assuredly not a good thing.

What it means (again) is that no one is trading the actual bonds. If one day everyone was dumping high yield ETFs, this entire model goes out the window. Recall what Barcalys said in the passages cited above (this time I will use highlights):

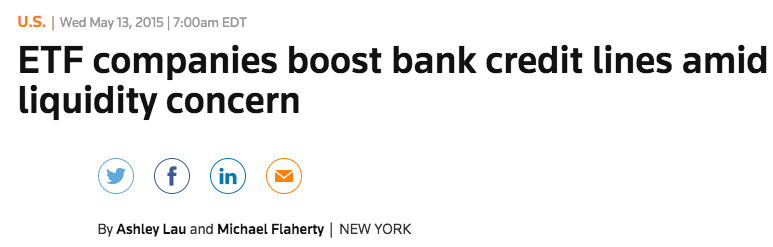

If flows are highly correlated then the risk is relatively high. Funds will have a difficult time selling bonds when they experience an outflow, since other managers would similarly be selling. In this circumstance, managers have a relatively short list of strategies to deal with flows. They can keep increased cash on hand, or (less likely) they can hope that other non-retail buyers step into the market at a reasonable discount to market levels.See the problem? Note the bit about "they can keep increased cash on hand." Consider that, and then consider this headline that Reuters ran back in 2015:

Starting to get the picture? Here's a quote from that Reuters piece:

The biggest providers of exchange-traded funds, which have been funneling billions of investor dollars into some little-traded corners of the bond market, are bolstering bank credit lines for cash to tap in the event of a market meltdown.Ok now, if you're following along, your next question should be something along these lines: "my God Heisenberg, how much of the trading in high yield ETFs is actual investors and how much is just portfolio managers swapping shares around?!"

Or, put differently: "to what extent, when I look at volumes in popular HY ETFs, am I seeing money managers dodging the actual markets for the bonds that underpin the ETF shares?!"

Or, my favorite derivation of the question: "to what extent am I watching portfolio managers sow the seeds of their own destruction?"

For the answer, we go to Barclays again. These excerpts are from a note out last week (my highlights):

On average, 54% of fund flows are "diversifiable," meaning that portfolio managers can reliably use ETFs instead of trading bonds to satisfy a significant share of their own fund flows. Indeed, an analysis of the magnitude of fund flows at the fund level suggests that approximately 25% of the outstanding float in high yield ETFs could be held by portfolio managers with daily liquidity needs.

Several pieces of evidence support this view (alongside anecdotal evidence from money managers and ETF traders). The first is the high concentration of assets among passive high yield funds. The top three passive funds represent 68% of passive high yield assets, while the top three passive government and equity funds represent 39% and 16% of passive assets, respectively. All of the large passive funds in high yield are ETFs, which have the benefit of trading in the secondary market. High concentration leads to larger secondary flows, which is useful for institutional managers trying to use ETFs to manage inflows and outflows. Without sufficient secondary trading, selling of shares is more likely to lead to share destruction, which relies on the liquidity of the underlying market. ETFs mitigate liquidity needs only to the extent that their secondary trading volumes are large relative to primary volumes (ie, share creation and redemption volumes). A large number of thinly traded ETFs would not be useful to institutional managers.

Indeed, the largest four high yield ETFs have secondary volumes of 4-8x primary volumes.

The passive share of high yield fund AUM can therefore be thought of as comprising two different types of owners: retail investors that own ETFs as part of their investment strategy and institutions that use them primarily for liquidity management. Secondary flows from the first group are not replacing corporate bond trading - they are similar to gross flows for an open-end mutual fund, which are netted at NAV. Secondary flows from institutions, however, may be replacing trades in the underlying corporate bonds.

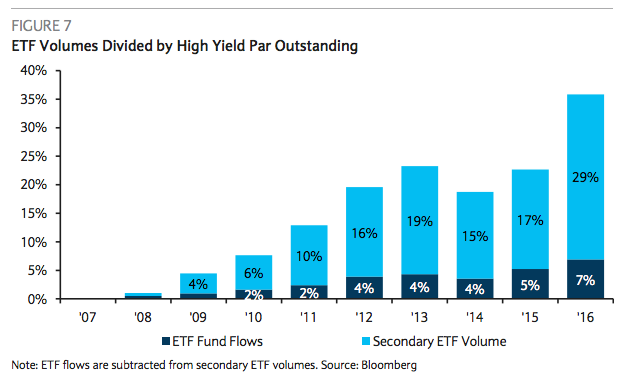

This is an important differentiation, because the overall flows for high yield ETFs are large relative to the size of the high yield market, despite the relatively small size of the funds. Daily TRACE volumes in high yield bonds averaged $12bn last year. Secondary trading in the four largest high yield ETFs, which represent only about 3% of total high yield assets, was $1.6bn daily in 2016. The contrast in turnover is striking: we estimate annual turnover of about 1.4x for high yield, while the ETF numbers imply annual turnover of 10.7x. Secondary ETF volumes are so significant that, if they were fully substituting away from secondary corporate activity, the implications for bond turnover would be substantial. Figure 7 divides total secondary ETF volume by the size of the high yield market to convert those volumes into a turnover-equivalent measure.

Please take a second to think about that.

Fully one quarter of the outstanding float in popular HY ETFs is likely portfolio managers using the ETFs to manage flows. Translation: you are not looking at what you think you're looking at when you assess trading in those vehicles.

As for the last three bolded sentences in the excerpted passages above and the chart that follows them, I truly hope you internalize the message there. If what you're seeing in terms of action in HY ETFs translates directly into what we might call a "migration" from the cash bond market, the effect on turnover of the actual bonds is huge.

Barclays calls it "substantial." They're being polite. Allow me to employ a popular Katt Williams meme to illustrate what your reaction to that last excerpted paragraph should be:

As I've said more times than I care to remember, the problem with all of this (and hence the problem with Vanguard's take) is that when you stop using something (anything really, but in this case we're referring to the actual market for the underlying bonds), it invariably falls into disrepair.

That disrepair, combined with the absence of banks willing to lend their balance sheet (i.e. inventory bonds) in a pinch, means there's no liquidity for the assets that underpin these ETFs.

That lack of liquidity causes fund managers to use those very same ETFs to match flows. That substitution itself exacerbates the very same illiquidity that prompted the substitution in the first place. It's a self-fulfilling prophecy.

This is a textbook example of "caveat emptor."

The problem is, these ETFs don't come with a "buyer beware" stamp on the prospectus. Instead, they come with a BlackRock or a Barclays (an irony of ironies given the analysis above) stamp of approval.

With that, I'll close with a quote from Carl Icahn who spoke about all of the above in the summer of 2015:

Well, BlackRock has a great name, they're sitting with $4.7 trillion. That's pretty good. And we could buy one of their ETFs. OK, woo, that sounds good. Why not?

0 comments:

Publicar un comentario