The Beginning Of The End

by: Eric Parnell, CFA

- Share buybacks have been helping to drive stocks higher throughout the post-crisis period.

- Rampant buyback activity may now be on the wane.

- This has important implications for the sustainability of the bull market in stocks.

- Rampant buyback activity may now be on the wane.

- This has important implications for the sustainability of the bull market in stocks.

- A key driver of stock market gains throughout the post-crisis period is slowly fading away. Who, if anyone, will be the marginal buyer of stocks if this important source of demand continues to fade away?

Buybacks

Buybacks

It has not been individual or institutional investors that have been driving stock market gains during the post-crisis period. In fact, we have seen more than $1 trillion in net outflows from domestic equity mutual funds since the calming of the financial crisis in early 2009 according to data from the Investment Company Institute (ICI). And since last June, when the S&P 500 Index (NYSEARCA:SPY) has increased in value by +17%, we saw another $10 billion in net outflows from domestic equity mutual funds and ETFs. This activity occurred despite all of the talk about the rotation out of stocks and into bonds (NYSEARCA:BND), which notably have received +$145 billion in mutual fund and ETF net inflows over the same time period yet are lower by -3%.

So it has been neither individuals nor institutional investors that are not only the primary sources of demand but instead have been steady sellers on net throughout the post-crisis period.

Who exactly is the marginal buyer of stocks in today's market? A primary source has been corporations, which have been buying back their stock at an increasingly furious pace over the past several years.

Who exactly is the marginal buyer of stocks in today's market? A primary source has been corporations, which have been buying back their stock at an increasingly furious pace over the past several years.

What exactly is the appeal of share buybacks for corporations, anyway? To begin with, it provides a way for companies to reward their shareholders with the return of cash. By buying back their own stock, the company is providing an added source of demand for shares that will presumably help push the stock price higher, all else held equal. Perhaps more importantly, it also has the effect of lowering the number of shares outstanding, which has the effect of increasing earnings per share and helping to improve the appearance of a company's operating performance.

So what has been taking place on the corporate share buyback front in recent years? Since 2011, corporations in the S&P 500 Index have repurchased more than $2.7 trillion of their own stock, comfortably more than offsetting the steady sale of more than stock by individuals and institutions over this same time period. Put more simply, without the massive tailwind of corporate buybacks during the post-crisis period, we may very well have been looking at a stock market that is nowhere close to the all-time highs it is trading at today.

At the same time, it has also created the illusion that corporations are performing better than they actually are, and subsequently that stocks are more reasonably valued than they would be otherwise.

Consider the following. Back on September 30, 2011, the stock market, as measured by the S&P 500 Index, was trading at just over 1,100 and had just generated as reported earnings of $792 billion. This represented an as-reported earnings per share of $86.98 on the index at the time and was providing investors with a generally reasonable valuation of just over 13 times trailing earnings on the broader market.

Now for the most recently completed quarter in 2016 Q3, the S&P 500 Index was trading at 2,168 and had just generated as reported annual earnings of $774 billion for an earnings per share of $89.09. This had stocks trading at a historically extreme premium of 24.3 times trailing earnings.

Here, we have the passage of five years' worth of time. And even with the massive volume of share buybacks that occurred over this time period, corporations were doing effectively no better in late 2016 than they were in 2011. Yet stock prices have now more than doubled since that time.

But let's take a closer look. In 2011 Q3, S&P 500 Index corporations generated annual earnings of $792 billion, which is more than the $774 billion they generated in 2016 Q3. Yet S&P 500 Index EPS in 2011 Q3 was less at $86.98 versus $89.09 in 2016 Q3. Such is the added juice from share buybacks.

It is worth noting that today's earnings look even worse on an inflation-adjusted basis, as the S&P 500 Index would need to generate earnings of $855 billion just to match 2011 earnings on a real basis.

And for those that may think that operating earnings would paint a better picture then as reported earnings in this regard, it is worth noting that all of these readings actually look worse on an as reported basis.

It is worthwhile to take all of this one step further. What if we backed out the positive impact on earnings per share resulting from corporate buybacks that have taken place over the past five years? After all, companies are still earning less today even on a nominal basis versus what they were earning five years ago.

Without share buybacks, the S&P 500 Index would instead have earnings per share as of 2016 Q3 at just $85.07, which is more than -4.5% lower than the official reading of $89.09 thanks to share buybacks.

That's Rich

Of course, the U.S. stock market has spent the past six months since the end 2016 Q3 storming to new all-time highs. What has this meant for current valuations? With the tailwind of share buybacks, the S&P 500 Index is now trading at an extraordinary 26.3 times trailing earnings.

And when backing out the added boost provided by share buybacks, stocks would be trading at an even more astronomical 27.6 times trailing earnings.

And when backing out the added boost provided by share buybacks, stocks would be trading at an even more astronomical 27.6 times trailing earnings.

As I pause to wipe the blood from my nose, it is worth noting that the S&P 500 Index was trading at 19.4 times earnings when it peaked in late 2007 and 29.4 times earnings when the tech bubble burst in early 2000. Put simply, we are well beyond 2007 premiums and quickly closing in on what is remembered as ridiculous valuations from the peak of the tech bubble. Making matters worse for today's market, premium valuations from the tech bubble were largely concentrated in the three segments of technology, media and telecom. Today, it is the entire market.

Of course, corporate earnings are currently on a rapidly improving trajectory that includes S&P 500 earnings that are coming in at $97.68 per share as of its latest reading with more than 80% of companies reporting, which on a buyback adjusted basis looks more like $92.93 per share versus 2011 levels with estimated annual earnings of $845 billion that is still clawing its way back to breakeven versus 2011 Q3 levels on an inflation-adjusted basis. While this earnings improvement will provide some much needed relief on the valuation front, it still has stocks trading at 24.1 times trailing earnings and 25.3 times earnings in a world without buybacks over the past five years.

Thus, while the recent earnings improvement is certainly welcome, companies still have a lot more improving to do on the earnings front before stocks can be considered anything close to reasonably valued.

Looking Ahead

Stock buybacks have been a critical driver of stock market returns over the past five years.

This raises a critically important question - how likely are they to continue going forward?

This raises a critically important question - how likely are they to continue going forward?

To answer this question it is important to note the following. There is no free lunch. Just like artificially inflating asset prices through relentlessly easy monetary policy is not without costs, so too is engaging in aggressive share buyback activity in order to return cash to shareholders and boost earnings per share. This is particularly true when a primary source for the funds to support this rampant buyback activity has been tapping low-cost debt markets in recent years for the purpose of buying back stock and paying dividends to shareholders.

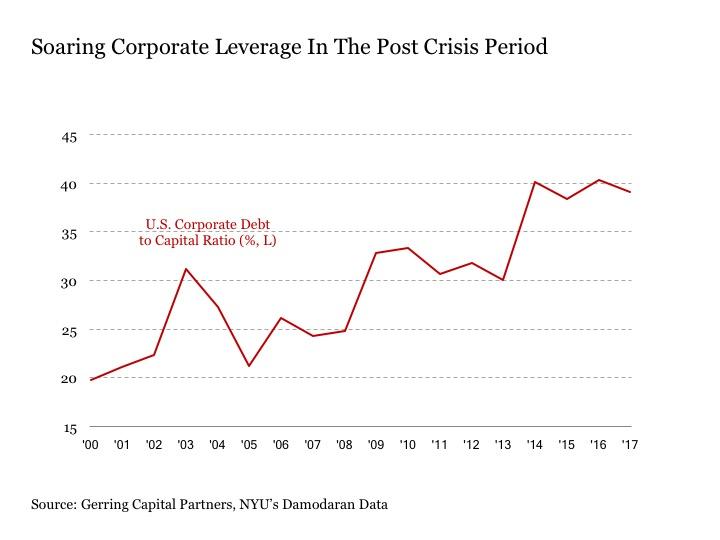

At some point, the amount of debt and financial leverage that a company can take on reaches an upper bound, and it appears that we may be approaching this limit in 2017, if we have not already surpassed it. For example, the U.S. corporate debt to total capital ratio, which was at 20% at the turn of the millennium and 25% in 2007 heading into the financial crisis has skyrocketed in recent years to over 40%. This is having a steadily eroding effect on corporate credit quality, with rating agency Fitch recently stating that some corporate credit issuers may be facing downgrades if current buyback programs continue into 2017. Thus, from a corporate finance perspective, the cost of capital benefits that might once have been derived from such buyback activities are now becoming drawbacks.

Adding to the mounting headwinds on the buyback front is the fact that borrowing costs may be on the rise. Many have been quick to proclaim the death of the bond market in recent months. And while rumors of its passing may ultimately prove greatly exaggerated, borrowing costs are still higher today than they were last summer and may potentially rise further in the months ahead with the U.S. Federal Reserve pounding the table as of late about potentially raising interest rates sooner rather than later and more rather than less in 2017.

Of course, the much ballyhooed corporate tax reform and profit repatriation are supposed to provide a welcome offset to these negative forces and encourage further buyback activity in 2017. That is, of course, if it actually happens in 2017. Proving once again that the laws of unforeseen consequences have not been repealed, markets are slowly waking up to the fact that the pro-growth hopes and dreams from the day after Election Day in November 2016 where everything would be magically implemented on January 20 are giving way to the reality that it is far more complicated than that to first legislate, then implement, then realize the positive pass-through effects from whatever sausage riddled final rules are finally put into place. Put more simply, it's going to take a whole lot longer for corporate tax reform to play out and may end up looking a lot different than expected at the end of the day. And even if it happens in 2017, it may not be until 2018 at the earliest until we start to see the effects of it.

The Beginning Of The End

Stocks need continued corporate buybacks to keep the current rally afloat. But headwinds are mounting that may increasingly curb this activity going forward. And it may already be too late for any future legislative changes to fill the gap that is now forming on the corporate buyback front.

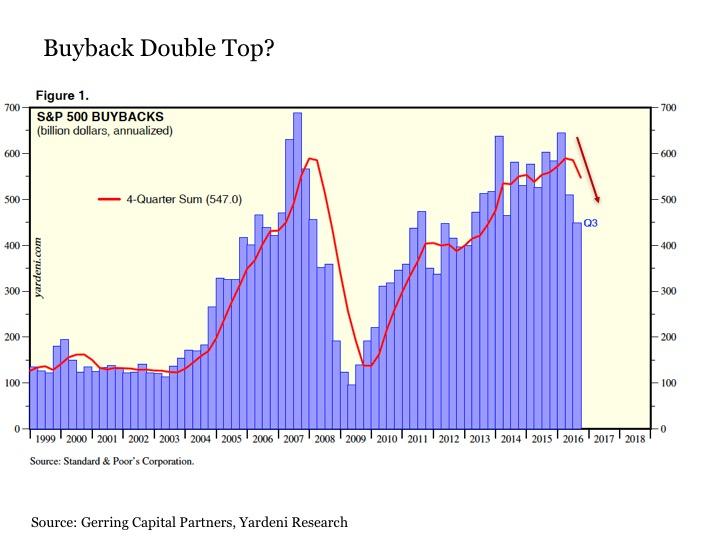

After peaking at the start of 2016 at levels seen during the summer of 2007 at the onset of the financial crisis, corporate buybacks have been sharply declining on an annualized basis over the past two quarters. And in 2016 Q3, the annual rate of buybacks fell to their lowest level since early 2012. While still early, this is an ominous new development that warrants close attention in the months ahead. For if corporate buyback activity continues to decline at its recent pace, particularly with individual and institutional investors remaining largely on the sidelines with domestic equity inflows totaling a negligible $1.5 billion in 2017 despite stocks surging to new all-time highs, it may eventually start to take the broader stock market down with it.

The Wrap

The already historically expensive stock market is increasingly losing a critically important tailwind in the form of corporate buybacks. While it is too soon to declare the bull market in jeopardy, particularly given the fact that stocks cannot seem to be kept lower for hours much less for a trading day or more in recent weeks, this is an important indicator that warrants close attention in the months ahead. For if corporate buyback activity goes the way of the individual and institutional investor circa 2008, stocks may struggle to hold on to their increasingly lofty valuation perch.

0 comments:

Publicar un comentario