Buttonwood

Sovereign-bond issuers shrug off downgrades

Bond-market vigilantes have lost their menace

.

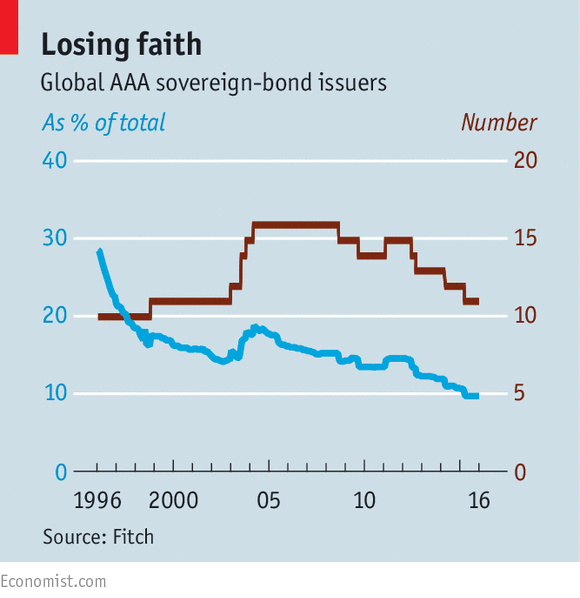

But despite the spending cuts and the tax increases he imposed, Britain was downgraded in 2013. There are only 11 countries with AAA status, according to Fitch, a rating agency, down from 16 in 2009. By value, only 40% of global sovereign debt has the highest rating, down from 48% a decade ago.

Clearly, at the sovereign level, the deterioration has been driven by the global financial crisis, which dented both economic growth and tax revenue. But with bond yields very low, and with central banks willing buyers of government bonds, countries have not paid a penalty for their bigger debt burdens.

Japan first lost its AAA rating in 2001, as its debt-to-GDP ratio soared. But that didn’t stop investors from buying its bonds, especially when the country succumbed to bouts of deflation. A very low nominal yield is still positive in real terms when prices are falling. Even if investors did lose their appetite, the Bank of Japan is a willing buyer; it has a target for the country’s ten-year bond yield of zero and, at 0.08%, the current level is not far off.

It is a similar story in America, which lost its AAA ranking from S&P in 2011. Five years later, the ten-year yield was at a record low of 1.36%.

Clearly the bond vigilantes that spooked politicians in the 1990s have lost their menace. Dealing with the deficit is no longer the most important issue. It is not just central banks. Commercial banks, pension funds and insurance companies all also need to own government bonds for liquidity or regulatory reasons; they are relatively indifferent to the actual level of yield involved.

When markets don’t penalise them for running deficits, it seems rational for governments not to risk the wrath of voters by curbing borrowing and imposing austerity. There are exceptions to this rule—those countries that do not have the luxury of borrowing in their own currency. In the euro zone the most prominent example is Greece, which is still struggling to deal with its debts.

But even the euro zone has got away with less punishment than might have been expected when the Maastricht criteria for single-currency membership were established 25 years ago.

Germany has a debt-to-GDP ratio over 70%, more than ten percentage points above the target level. Its ten-year bonds yield just 0.37%.

The rise of populism means that governments are even less likely to worry about an adverse reaction in the bond markets. Donald Trump has promised a combination of tax cuts, infrastructure spending and the safeguarding of entitlements such as Social Security and Medicare. These plans have to pass Congress, but the Committee for a Responsible Federal Budget, a lobby group, estimated that they would push American debt to 105% of GDP (from 77%) in a decade. Britain has abandoned its target of eliminating its deficit by 2020 (Mr Osborne’s original target was 2015). Facing an insurgent threat from the likes of Marine Le Pen and Geert Wilders, European governments will be wary of raising taxes or cutting benefits.

In macroeconomic terms this is sensible. The main priority for rich countries should be developing a decent rate of growth rather than austerity. But if growth does not pick up significantly, the outline of a future crisis looks clear. Current debt levels are perfectly serviceable at current yields. But if yields rise another two to three percentage points that might no longer be the case, especially as government budgets will be strained by rising pensions and health-care costs from their ageing populations. At that point, bond investors might wake from their slumber and take their revenge.

0 comments:

Publicar un comentario