Buttonwood

Interest rates and investment returns

Low rates usually mean low returns; so why are markets so buoyant?

IF THERE is one aspect of the current era sure to obsess the financial historians of tomorrow, it is the unprecedentedly low level of interest rates. Never before have deposit rates or bond yields been so depressed in nominal terms, with some governments even able to borrow at negative rates. It is taking a long time for investors to adjust their assumptions accordingly.

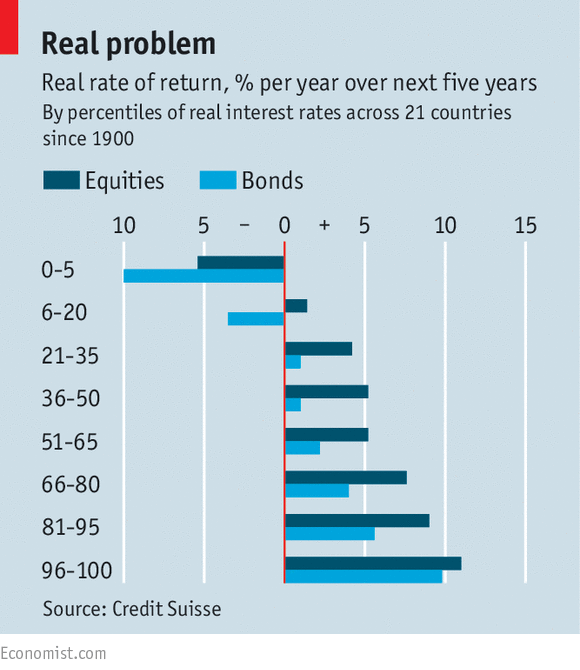

Real interest rates (ie, allowing for inflation) are also low. As measured by inflation-linked bonds, they are around -1% in big rich economies. In their latest annual report for Credit Suisse on global investment returns, Elroy Dimson of Cambridge University and Paul Marsh and Mike Staunton of the London Business School look at the relationship between real interest rates and future investment returns. Very low real rates have in the past been associated with poor future equity returns (see chart).

That may come as a nasty shock for state and local-government pension funds in America.

They have to assume a future rate of return on their investments when calculating how much they need to contribute to their plans each year. Most opt for 7-8%, a level that has prevailed for years. That return looks highly implausible at a time when ten-year Treasury bonds yield just 2.4%.

There is a strong incentive not to change these assumptions. CalPERS, a Californian state pension fund, has cut its assumed return from 7.5% to 7%. But even that small shift will cost the state $2bn a year in extra contributions.

Why should low real rates and low returns be linked? One reason is that very low real rates are associated with times of economic difficulty, and thus periods when corporate profits are under threat. But a low real interest rate also means a low cost of capital for companies, which ought to be good news. Indeed, central banks ease monetary policy to try to drive down interest rates, and thus encourage business investment.

There has been some recovery in business investment since the last recession. But that recovery has not been as robust as might have been expected, given the low cost of capital. In a recent speech, Sir Jon Cunliffe, deputy governor of the Bank of England, noted that “in the 40 years to 2007, business-investment growth averaged 3% a year. In the eight years since the crisis it has averaged 1.5% annually.”

A number of possibilities could explain this decline, including a lack of access to finance. Banks have been boosting their capital ratios in recent years and have been more reluctant to lend.

But another factor relates to the “hurdle rate” companies use before they decide whether to invest. A survey by the Bank of England indicates that firms are still using a hurdle rate of 12%, around the average of the rate of return on investment they have achieved in the past.

In other words, despite the big fall in the cost of borrowing since the crisis, the hurdle rate has not come down. Since the risk-free rate is in effect zero, the bank says British firms are now looking for a 12-percentage-point margin compared with one of seven points before the crisis.

This could be a version of “money illusion”, when people fail to adjust their expectations for nominal returns as inflation declines (in this case, both real and nominal expectations ought to have fallen).

There is an alternative explanation for the failure of expectations to shift. Both businesses and investors, realising that the economic outlook is uncertain, may be demanding a higher risk premium for starting new projects or buying shares. That explanation is a little hard to square, however, with the repeated new record highs being scaled by stockmarkets or with the high valuations afforded to American equities.

Since the market low in March 2009, dividends have risen by 48% in real terms and real share prices have risen by 167%, according to Robert Shiller of Yale University. The cyclically-adjusted price-earnings ratio (or CAPE), which averages profits over ten years, is 28.7, its highest level since April 2002. In the past, very high CAPEs have been associated with low future returns.

Indeed, having analysed the data, Messrs Dimson, Marsh and Staunton reckon global investors are expecting a risk premium of 3-3.5% relative to Treasury bills—a level that is lower, not higher, than the historic average. So something does not add up. American pension funds are optimistic.

Businesses are cautious. Shares are trading on very high valuations. Not all these assumptions can be proved right.

Real interest rates (ie, allowing for inflation) are also low. As measured by inflation-linked bonds, they are around -1% in big rich economies. In their latest annual report for Credit Suisse on global investment returns, Elroy Dimson of Cambridge University and Paul Marsh and Mike Staunton of the London Business School look at the relationship between real interest rates and future investment returns. Very low real rates have in the past been associated with poor future equity returns (see chart).

They have to assume a future rate of return on their investments when calculating how much they need to contribute to their plans each year. Most opt for 7-8%, a level that has prevailed for years. That return looks highly implausible at a time when ten-year Treasury bonds yield just 2.4%.

There is a strong incentive not to change these assumptions. CalPERS, a Californian state pension fund, has cut its assumed return from 7.5% to 7%. But even that small shift will cost the state $2bn a year in extra contributions.

Why should low real rates and low returns be linked? One reason is that very low real rates are associated with times of economic difficulty, and thus periods when corporate profits are under threat. But a low real interest rate also means a low cost of capital for companies, which ought to be good news. Indeed, central banks ease monetary policy to try to drive down interest rates, and thus encourage business investment.

There has been some recovery in business investment since the last recession. But that recovery has not been as robust as might have been expected, given the low cost of capital. In a recent speech, Sir Jon Cunliffe, deputy governor of the Bank of England, noted that “in the 40 years to 2007, business-investment growth averaged 3% a year. In the eight years since the crisis it has averaged 1.5% annually.”

But another factor relates to the “hurdle rate” companies use before they decide whether to invest. A survey by the Bank of England indicates that firms are still using a hurdle rate of 12%, around the average of the rate of return on investment they have achieved in the past.

In other words, despite the big fall in the cost of borrowing since the crisis, the hurdle rate has not come down. Since the risk-free rate is in effect zero, the bank says British firms are now looking for a 12-percentage-point margin compared with one of seven points before the crisis.

This could be a version of “money illusion”, when people fail to adjust their expectations for nominal returns as inflation declines (in this case, both real and nominal expectations ought to have fallen).

There is an alternative explanation for the failure of expectations to shift. Both businesses and investors, realising that the economic outlook is uncertain, may be demanding a higher risk premium for starting new projects or buying shares. That explanation is a little hard to square, however, with the repeated new record highs being scaled by stockmarkets or with the high valuations afforded to American equities.

Since the market low in March 2009, dividends have risen by 48% in real terms and real share prices have risen by 167%, according to Robert Shiller of Yale University. The cyclically-adjusted price-earnings ratio (or CAPE), which averages profits over ten years, is 28.7, its highest level since April 2002. In the past, very high CAPEs have been associated with low future returns.

Indeed, having analysed the data, Messrs Dimson, Marsh and Staunton reckon global investors are expecting a risk premium of 3-3.5% relative to Treasury bills—a level that is lower, not higher, than the historic average. So something does not add up. American pension funds are optimistic.

Businesses are cautious. Shares are trading on very high valuations. Not all these assumptions can be proved right.

0 comments:

Publicar un comentario