Inflection Point For The U.S. Economy As This Recession Trigger Now Put In Motion

by: Atle Willems

- Towards the end of QE3, the money-creating burden was once again handed to the Banks.

- Banks reacted positively and lending growth expanded quickly.

- But in recent weeks, bank lending has actually contracted pulling the money supply growth rate into negative territory.

- Typically, these developments signal not only a looming GDP recession, but also increased probability of an economic crisis and a stock market crash.

- Following years of artificial growth, the U.S. economy now therefore appears to be at a major inflection point.

- Banks reacted positively and lending growth expanded quickly.

- But in recent weeks, bank lending has actually contracted pulling the money supply growth rate into negative territory.

- Typically, these developments signal not only a looming GDP recession, but also increased probability of an economic crisis and a stock market crash.

- Following years of artificial growth, the U.S. economy now therefore appears to be at a major inflection point.

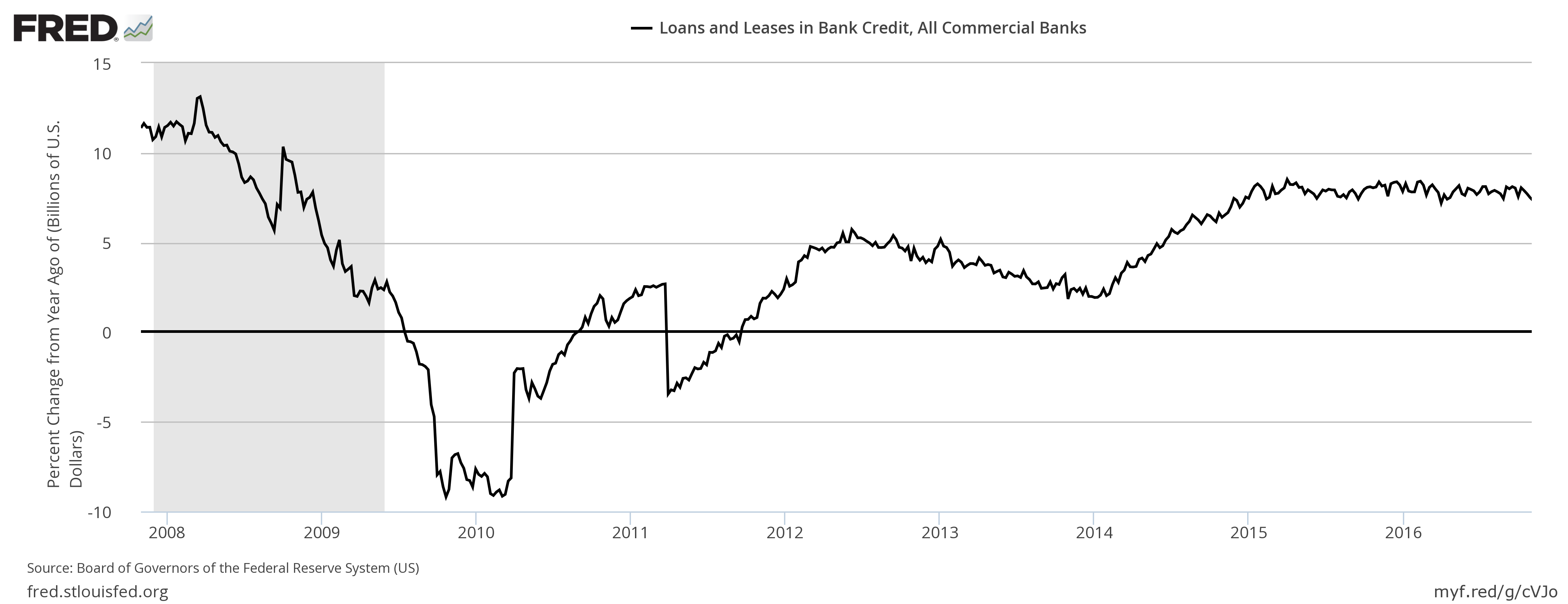

During the QE3 taper, the baton was handed from the Federal Reserve to the banks to put their unfathomable $2.8 trillion in mostly excess reserves "to work" and once again become the chief money creators. Banks, eager to earn higher returns than the 25 basis points offered on their reserves parked in Fed vaults, did what was expected of them and ramped up lending growth to around 8% within months.

The money supply growth rate was held stable as a result and also hovered around 8% on a year-on-year (y/y) basis.

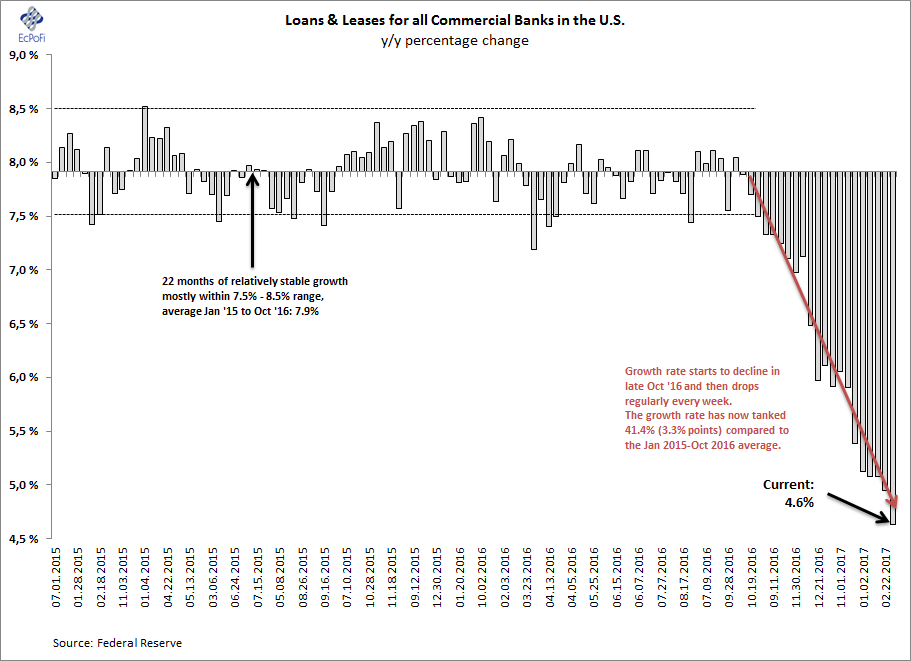

But in late October last year, bank lending growth started declining. It dropped modestly at first, but then started to tank in mid-December. According to the most recent data, the y/y growth rate has now dropped to 4.6%, the lowest reported since June 2014.

Why is this of such great importance? Because the reduction in lending growth will negatively affect the money supply growth rate. Changes in the money supply growth rate are economically important for many reasons, the most prominent being how they affect interest rates and relative prices, and the misdirection of resources that follow.

That is, when interest rates and prices are disturbed, i.e. altered compared to what the level of interest rates and prices would be absent these changes in the money supply, economic imbalances build up as a portion of resources are allocated elsewhere compared to where they would have been allocated absent these disturbances. Essentially, these alterations to interest rates and prices create the business cycle. An expansion of the money supply growth rate fuels inflationary booms, while declines trigger very real busts. In this sense, the business cycle is a reflection of the money cycle.

During the boom phase, undertakings that would not have been possible absent the credit expansion see the light of day and gradually expand. But this expansion is dependent on further credit growth and will hence collapse when the credit flow dries up. Effectively, many undertakings become addicted to further credit expansion during the boom phase, a state which is untenable. Why? because economic expansions are only sustainable when they are based on prior saving. The issuance of new money (which is what actually takes place when banks extend loans) is no substitute for saving.

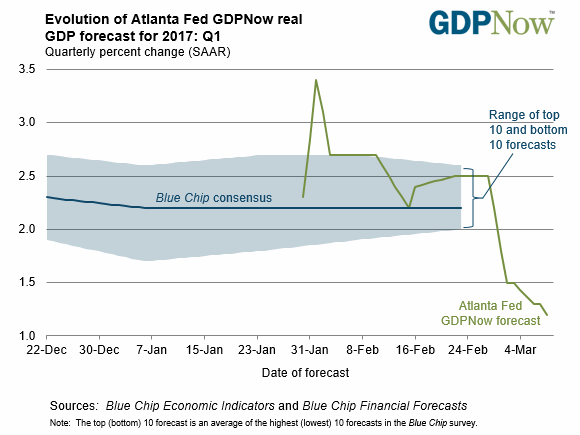

The risk is therefore that the decline in lending growth depicted in the chart above will trigger an economic reaction that brings about sharp corrections in many asset prices, including stock market prices. Since GDP growth is largely a function of money supply growth, GDP will also suffer from a decline in lending growth. The reduction in lending growth in recent months therefore may help explain why the Atlanta Fed GDPNow indicator has declined sharply in recent weeks.

The faster the money supply growth rate falls following a period of expansion, the quicker an economic reaction is triggered. Outright contraction in bank lending is therefore a major warning sign that a reaction of some sort (referred to as a "shock" in some circles) might be approaching.

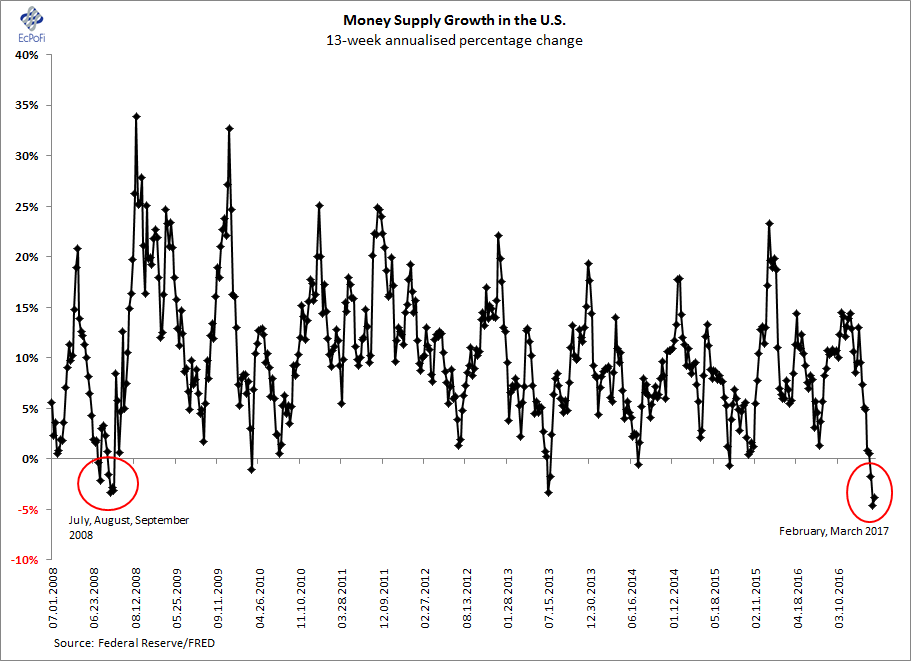

Looking at a shorter-term growth rate than the y/y growth rate depicted above, it becomes clear that lending growth on a rolling quarter (13 weeks annualised) basis is now in fact negative, i.e. lending is actually contracting.

The chart shows that lending on this basis has now contracted for four consecutive weeks. To put this in context, the last time this happened, ignoring the aftermath of the previous banking crisis, was in the run-up to the Lehman collapse in September 2008. In fact, it is highly unusual that lending ever contracts on a 13-week basis.

But when it does, it tends to precede or occur during an economic crisis of some sort. Based on data since 1995, the previous contractions in lending was in 1999 (towards the end of the dotcom bubble), 2001 and 2002 (recession), and eight consecutive weeks ending in early August 2008 (September 2008 banking crisis). The point is that a contraction in lending as we are seeing now is often associated with economic problems.

The highly anticipated Fed rate hike this week could hence hardly be timed more poorly as higher interest rates by itself will exert further downward pressure on lending growth.

Recent credit developments are therefore a major obstacle to a Fed rate hike which is why there is at least a small chance it will not raise rates.

There can be little doubt that the U.S. economy is now at or near a major inflection point. This artificial recovery (artificial because it has been driven by monetary inflation and a relative reduction in savings more than anything else) is now in its ninth year. At the same time, the stock market is valued for perfection.

The crux of the problems is that lending is now contracting while the economy at large and most asset prices depend on further injections of new money and low interest rates. If U.S. banks continue to reduce lending, it is only a matter of time before another major economic crisis hits the U.S. as the money supply growth rate has now also dived into negative territory.

The question then becomes not if but when and how the Fed will once again intervene as banks, at least for now, appear to be handing the baton back to the Fed. Chances are however that the Fed will once again react too late to avert another crisis.

Additional charts:

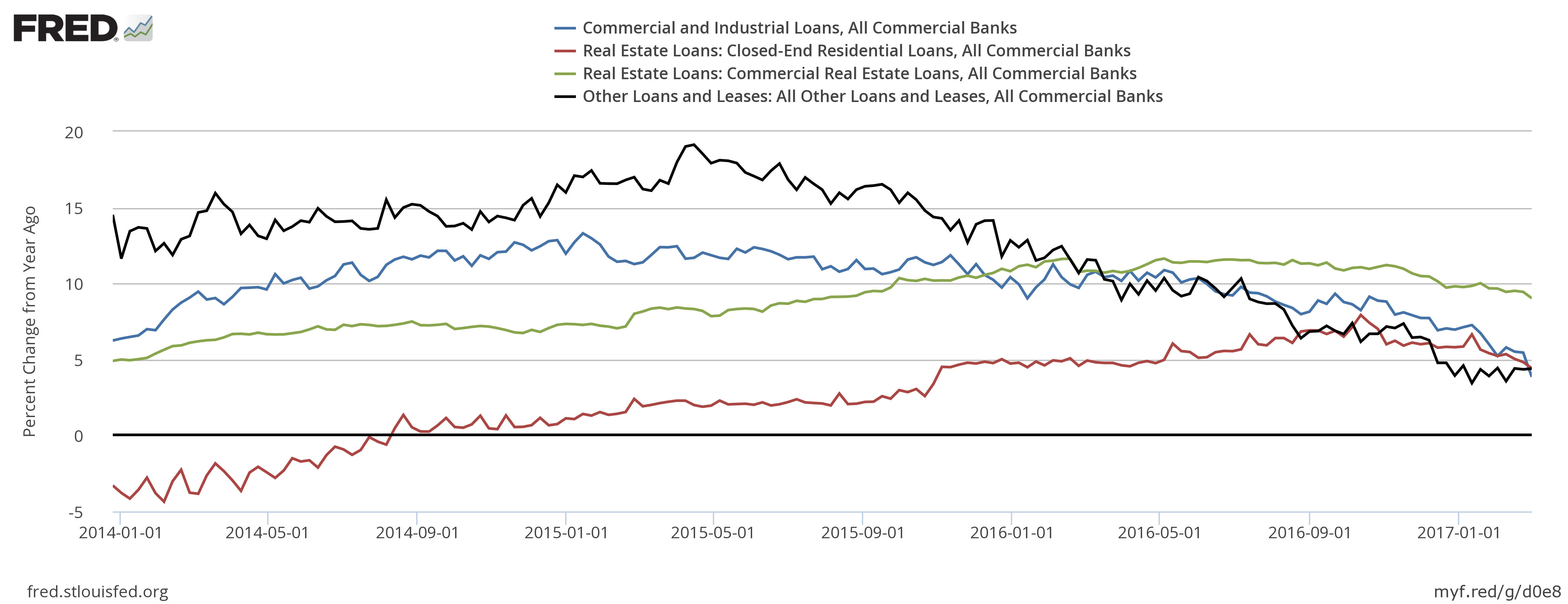

The four biggest components of bank lending (y/y)

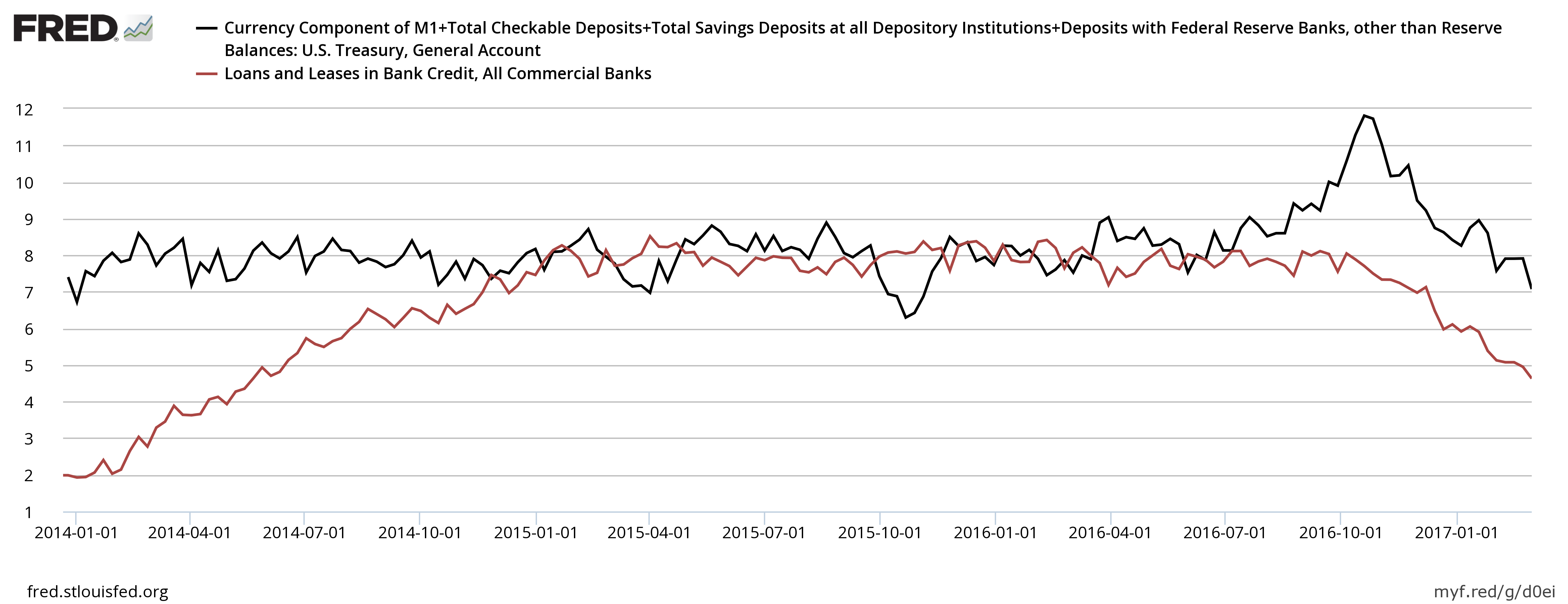

Lending growth and money supply growth (y/y)

0 comments:

Publicar un comentario