Fed Boosts Gold, But We Think The Narrative Is Changing - And This Factor Will Become Its Primary Driver

by: Hebba Investments

.

- Speculative traders sold and shorted gold in anticipation of the Fed meeting, which was the completely wrong move.

- As the Fed did what everybody expected, gold traders bought back previously sold positions in a “sell-the-rumor and buy-the-fact” moment.

- Asian gold premiums remain fairly subdued despite the price move in gold.

- With the Fed's move over, we think gold will now be focused on US fiscal and tax policy which we think will disappoint investors and boost gold.

- As the Fed did what everybody expected, gold traders bought back previously sold positions in a “sell-the-rumor and buy-the-fact” moment.

- Asian gold premiums remain fairly subdued despite the price move in gold.

- With the Fed's move over, we think gold will now be focused on US fiscal and tax policy which we think will disappoint investors and boost gold.

The latest Commitment of Traders (COT) report showed a large drop in speculative long positions leading up to the Federal Reserve meeting, which obviously was the wrong move by speculators as gold popped after the Fed's decision on a "sell-the-rumor and buy-the-fact" moment. We think much of the rise in gold after the Fed meeting was due to this overextended short position by speculative gold traders as evidenced by the surge in shorts (and drop in longs) leading up to the meeting.

In terms of physical gold premiums, in Asia they were mixed last week as Chinese premiums surged due to tightening import restrictions by the Chinese government. In contrast, Indian premiums fell from $2.00 to $1.50 over domestic gold prices, which was attributed to Indians paying advance tax for the fiscal year (India's fiscal year ends in March).

Finally, we think there's a shift in the gold narrative. The focus is shifting from the Federal Reserve and the direction of interest rates being the primary driver to one where the US government's policy and tax positions will be carefully scrutinized by gold traders.

We will get more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three-day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it. What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

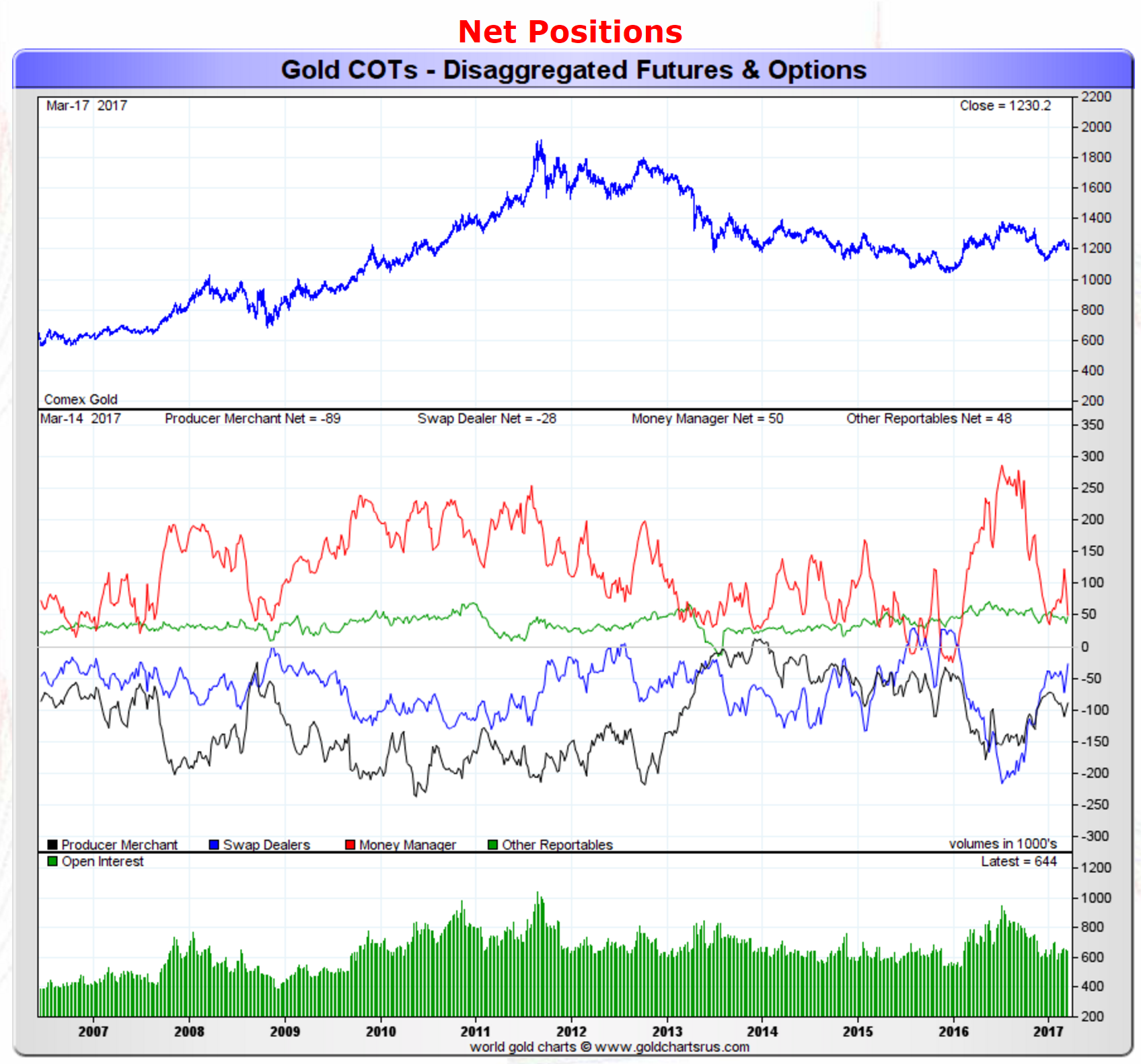

This week's report showed a decrease in speculative gold positions as longs shed 34,066 contracts during the COT week while shorts added 9,992 contracts to the gross speculative short position. This was one of the largest drops in the total net speculative position in months - and it turned out to be dead-wrong.

Moving on, the net position of all gold traders can be seen below:

Source: GoldChartsRUS

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, we saw the net position of speculative traders decrease by a chunky 44,000 contracts to 50,000 net speculative long contracts.

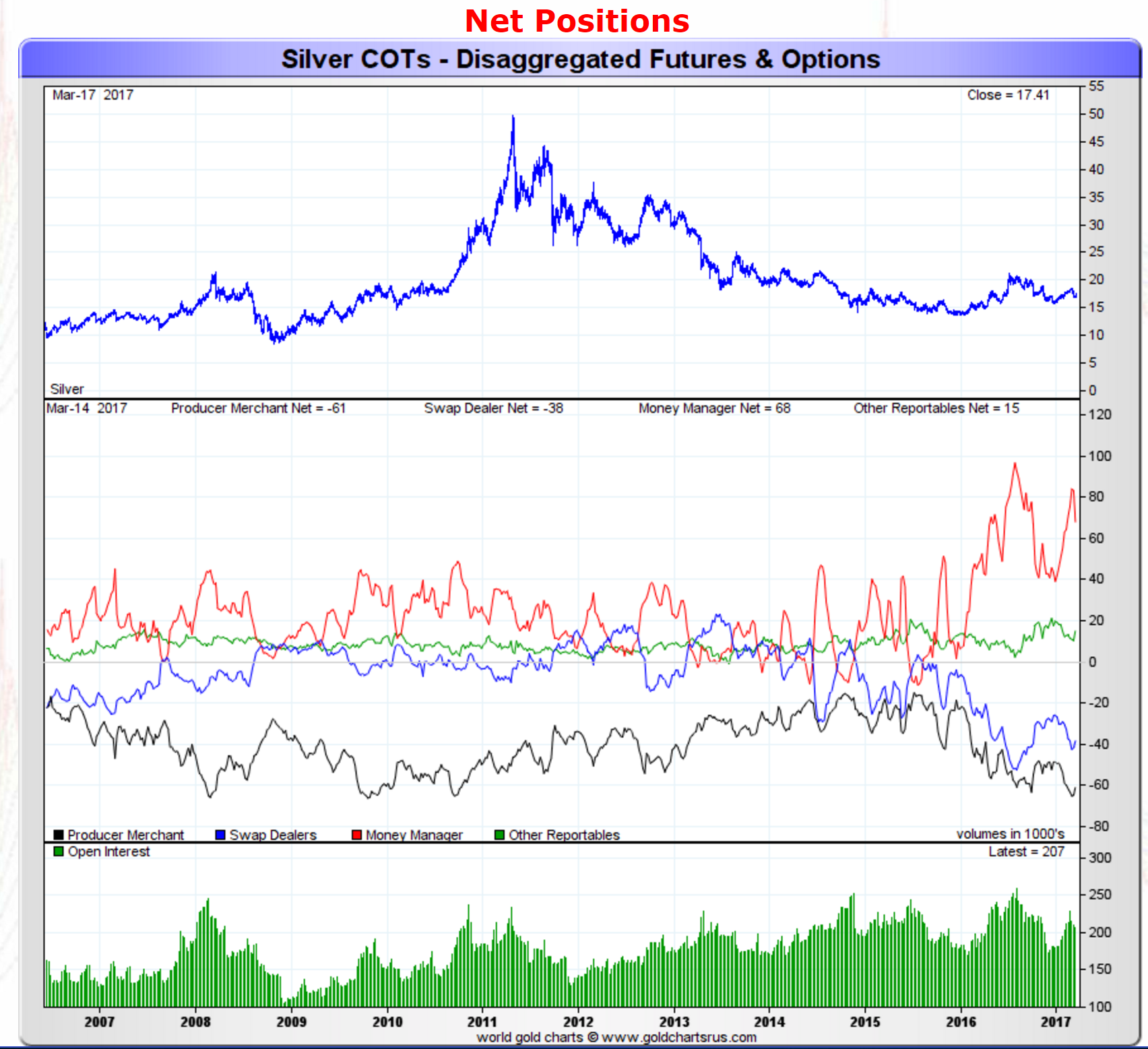

As for silver, the action week's action looked like the following:

Source: GoldChartsRUS

The red line which represents the net speculative positions of money managers, showed a big drop in bullish silver speculators as their total net position dropped by around 15,000 contracts to a net speculative long position of 68,000 contracts. While still high, it certainly is positive for contrarians as we see some of the speculative froth in silver drop.

Asian Gold Premiums Remain Mixed

As we mentioned earlier, Asian premiums remained mixed over the past week. Chinese premiums surged due to tightening import restrictions by the Chinese government as Beijing efforts to control capital outflows continued to restrict gold import licenses. While rising premiums are positive, if they are due to government restrictions we cannot give it as much of a bullish bias as premiums aren't rising to naturally increasing demand, but rather, to artificially decreased supply.

In contrast, Indian premiums fell from $2.00 to $1.50 over domestic gold prices, which was attributed to Indians paying advance tax for the fiscal year (India's fiscal year ends in March).

Meanwhile, premiums in Singapore rose to about $1.20, compared with the 90 cents to $1 range seen the week before, and prices in Japan were at a discount of 50 cents to a dollar, against the 75 cents to $1 levels in the prior week.

Our Take and What This Means for Investors

This week was an excellent example of "sell-the-rumor and buy-the-fact" as speculative traders all rushed to sell and short gold into the Fed meeting, only to be forced to cover and buy back positions as the Fed did exactly what was predicted of it. This should be a very clear lesson for those trading on already priced in news.

But we don't think all the move in gold was due to speculative trading on the Fed meeting - we think there were many traders starting to move in anticipation of US government tax and policy decisions moving forward. While a bit over-shadowed by the Fed, last week we also saw the initial budget proposal by President Trump - and it seems there is a lot of opposition by Republicans.

The budget will certainly be changed by the US Congress as we move forward, but there's a real chance of a US government shutdown in April if compromises are not reached, and with the current contention in Congress, we would not be surprised. If that happens, it would probably be very negative for the stock market and positive for gold (as chaos usually is).

If there is compromise, then we have a feeling it will not be because Congress approves most of Trump's budget (and its cuts), but rather, a big transformation of the bill as Congress approves many of the budget's spending measures but removes most of its budget cuts. Ultimately, watering down cuts and approving spending thus creating a budget which will lead to larger US déficits.

Finally, Goldman Sachs pointed out another very salient aspect of the President's budget that was a bit overlooked - the things it did NOT include:

- It provides no economic or fiscal projections

- It provides no discussion of tax reform or infrastructure plans, which the White House says will be released "in coming months", likely as part of a full budget submission to Congress that we expect to be released around May.

- It also includes no discussion of the Obamacare replacement plan.

The narrative has been that Wall Street has been rising because of President Trump's massive infrastructure spending and tax reform that will boost corporate bottom lines and use fiscal stimulus to boost the economy. Yet no mention at all in the budget - not good in our view for the popular narrative and that would be negative for stocks.

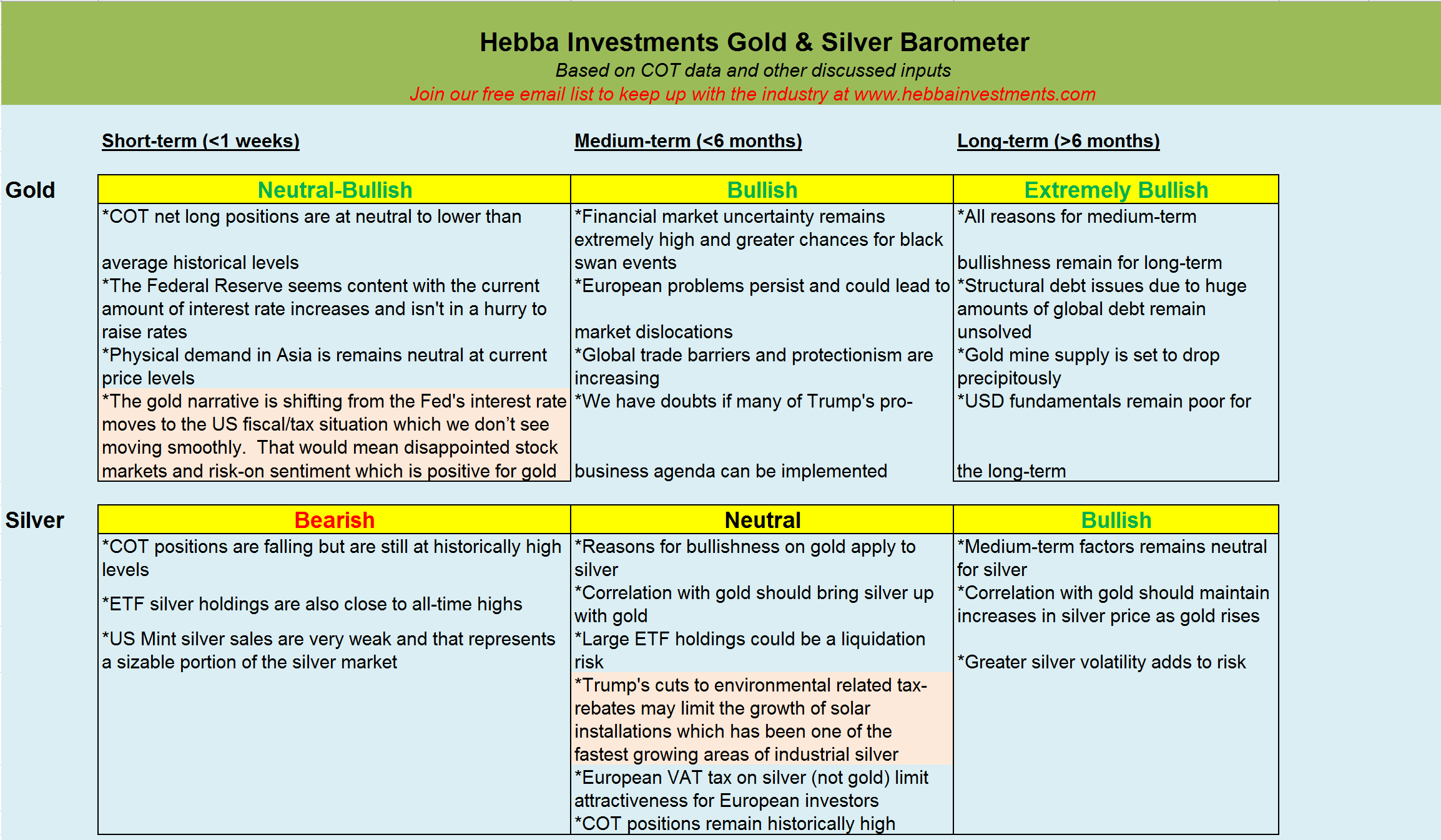

Last week we changed our short-term picture of gold from bearish to neutral, and this week we continue that positive shift from NEUTRAL to NEUTRAL-BULLISH on gold as the narrative changes from the Fed to the US government's budget and policy moves. We see a lot of friction and a lack of conviction by policy makers to implement the current budget and make any significant tax or infrastructure-spending moves. Since Wall Street has been rising in anticipation of that, we see the possibility of a major correction in stocks - and we think that would be positive for risk-off assets like gold.

The only reason we aren't going to BULLISH for the short-term gold picture is because we feel the new US-government focused narrative will take some time to sink in for traders. That means we could see a corrective drop in gold, but we would view that as a buying opportunity.

We remain bearish on silver for the reasons outlined last week as we see the risk-return much better in gold, but if we continue to see some of those speculative traders lower their net-long position in silver or a big drop in the price, we would be buyers of silver too as its correlation to gold would be much more attractive as a primary driver.

In summary, we are continuing to buy back some of our previously sold gold positions and we are starting to look to purchase some of our previously sold miners especially if we see a corrective drop next week. Thus we think investors should considering increasing their positions in the miners and gold ETFs, like the SPDR Gold Trust ETF (NYSEARCA:GLD), and ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL). For silver, we are still not ready to really begin aggressively adding to our positions in the ETF's like the iShares Silver Trust (NYSEARCA:SLV), ETFS Silver Trust (NYSEARCA:SIVR), and Sprott Physical Silver Trust (NYSEARCA:PSLV), as gold simply has a better risk-reward profile at the current time but with a further drop in silver we may consider buying back some of our previously sold positions.

0 comments:

Publicar un comentario