Could This Time Be Different?

by: Lawrence Fuller

Summary

- It feels a lot like the periods just before the prior two bull-market tops.

- Valuations are extreme and fear is nowhere to be found.

- Yet there are reasons it could be different this time.

- Regardless, I remain positioned for an eventual repeat of the previous two cycles.

- Valuations are extreme and fear is nowhere to be found.

- Yet there are reasons it could be different this time.

- Regardless, I remain positioned for an eventual repeat of the previous two cycles.

As I watch the stock market indices march to new all-time highs, including ten consecutive record-high closes for the Dow Jones Industrials (NYSEARCA:DIA), I am reminded of when I was investing in the late 1990s and mid-2000s. While both periods were very different from each other, as well as from the one we find ourselves in today, I view all three as fearless bull markets, rebuffing any macroeconomic or valuation concerns along the way. What is different for me is that while I was one of the truly fearless in the late 1990s, I was far less so in the 2000s, leading to what I can best describe as extremely cautious, if not fearful, today.

What has fueled my steadfast bearish outlook for the broad market in recent years is apprehension, which has kept my equity allocation below what it otherwise would be. Yet, I have continued to participate in the good times through alternate asset classes and an ever-evolving list of individual stocks and exchange-traded equity funds. Perhaps my caution has been misguided during the last leg up of this bull run, but it is a byproduct of 25 years of experience as an individual and professional investor. The saying is to be fearful when others are greedy, and greedy when others are fearful.

What I fear now is that history will repeat itself, yet I continue to ask myself if this time it could be different.

Historical Precedent

The reason I was so brave in the 1990s is that I never experienced a significant loss. Significant losses are not something you can fully appreciate unless you have experienced them for yourself.

Access to information was very limited compared to what we are inundated with today, even for a financial consultant, and what information I did have was bullish propaganda issued by my Wall Street employers. I rode the wave along with everyone else, growing a portfolio of less than $100k into more than $1 million by late 1999. That wave came crashing onto shore in 2000, and it took the majority of my portfolio with it. It was a painful experience, especially after having ignored the advice of my more-experienced father on multiple occasions, but I was a know-it-all at 29 years old. I had millionaire status to prove it.

I had very little understanding of the real economy back then, living in the bubble that houses the financial world and virtually no grasp of the business cycle. As the forest started to burn, I was lost in the trees. I learned painful, yet valuable, lessons during that period. Perhaps the most important was to balance my focus between macroeconomics and the bottoms-up analysis of individual positions.

As a more experienced and knowledgeable investor during the 2000s, I was well aware that there was a bubble in the housing market. My greatest mistake at that time was in trusting that Fed Chair Bernanke had a full grasp of the severity of the crisis and that he would be able to contain it. I also didn't fully appreciate how interconnected various markets could become, as diversification was no defense when all assets became highly correlated, with the exception of Treasuries. I underestimated how severe the bear market in stocks would be, following the bankruptcy of Lehman Brothers, and I also relied on the egregious "adjusted" earnings provided by Wall Street when judging valuations.

Therefore, I didn't have as much liquidity as I needed to capitalize on what I knew was a once-in-a-lifetime opportunity to buy high-quality stocks in 2009.

While I have had many successes over the years, it is these two experiences that have shaped my investment philosophy over time, led to my tactical approach to portfolio management, and instilled a more macroeconomic focus to my market outlooks. I do not intend to lose sight of the forest for the trees ever again, nor will I rely on private or public institutions to act in what is the best interest of the markets or investing public.

I am not aware of very many investors who were able to successfully navigate through both of these bear markets without sustaining losses. I applaud those who were, but my sense is that they would be just as cautious, if not fearful, today as they were prior to the previous bull market tops. The cast of characters may be different in this play, but the story line is very much the same.

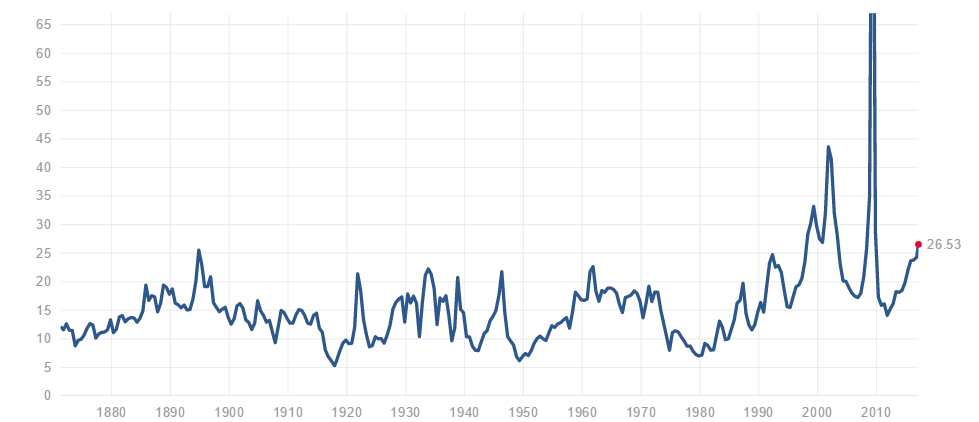

The stock market is expensive on a historical basis by every possible measure. Regardless, the consensus continues to rationalize why valuations are not only sustainable, but can continue to climb. The trailing price-to-earnings multiple, as can be seen below, for the S&P 500 index (NYSEARCA:SPY) has only been higher during the peaks in 2000 and 2007.

Source: multpl.com

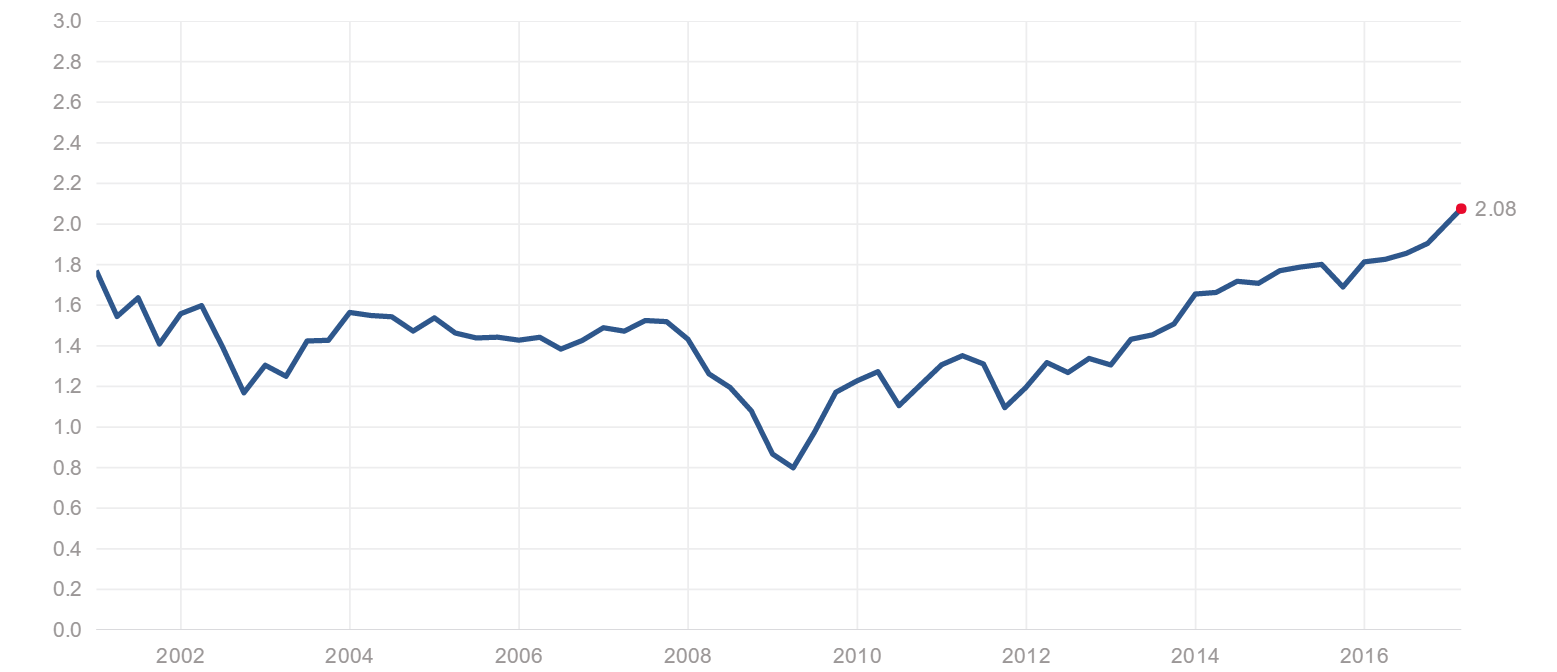

The price-to-sales ratio for the S&P 500, as can be seen below, has surpassed the peaks we saw in 2000 and 2007.

Source: www.multpl.com

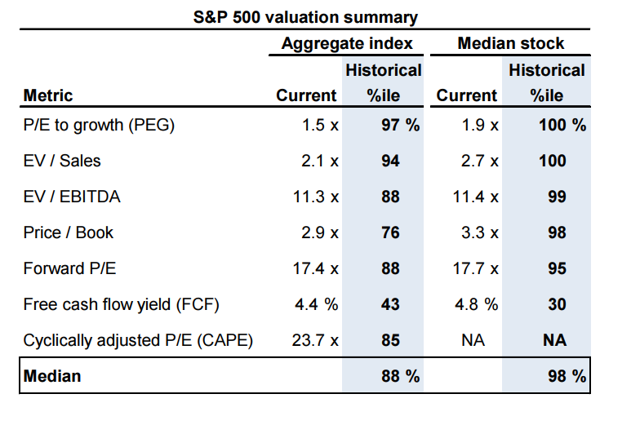

In fact, the stock market is in the most expensive decile by nearly every metric, as can be seen below.

If this doesn't flash a warning sign, I don't know what does, but the consensus continues to grasp for potential catalysts which could push valuations even higher.

Source: Goldman Sachs

Source: Goldman Sachs

This does not mean that stock market valuations will decline today, tomorrow or this year.

Instead, they could continue to rise. Yet history has shown that forward returns from these levels are far below average, as the potential for downside risk grows. As a result, given my investment experience over the past 25 years, I am more inclined to focus on what is going wrong now, or could go wrong in the future, than to rely on what could go right in order to justify even higher valuations.

As I grapple with the potential benefits for the market from tax cuts, deregulation and infrastructure spending, I see offsetting macroeconomic headwinds such as declining real incomes, excess capacity and tightening financial conditions. We are at the end of the business cycle, as opposed to its beginning. What disturbs me the most, yet receives no attention at all from the punditry, is that the primary source of those last two crises was never extinguished. In fact, it continues to grow.

The bubbles we saw in 2000 and 2008 were the result of tremendous excess that built up in the economy. That excess came in the form of debt, which was merely transformed and transferred from corporate to consumer to what is now government balance sheets. What is different this time is that the federal government, with the assistance of the Federal Reserve, has been able to pretend and extend year after year, unlike corporations and consumers were able to do in the prior two decades.

So long as the federal government can continue to run deficits and grow the debt in order to finance consumption, perhaps this bull market can continue.

Worse yet is that as government debt has exploded, corporations and consumers continue to accumulate debt, which has once again surpassed record levels. This debt steals forward demand, slowing the potential for future growth, until it ultimately must be extinguished in one way or another. So long as the rest of the world is willing to finance our fiscal irresponsibility, the party can continue. But when our credibility is called into question, our cost to borrow could increase dramatically over a very short period of time and another crisis will ensue.

Still, could it truly be different this time?

What is Different

I see three major differences between today and the prior two bull markets, difference which could prolong the current one. The first is the emergence of computerized trading. Algorithmic trading has accounted for a growing percentage of the volume on our exchanges over the past ten years. I view this practice, which has absolutely nothing to do with investing, as a virus that has infected our markets. The problem is that this virus has now consumed the host and regulators have no way of eradicating it without destroying the host in the process. Nothing will change until there is a full-blown crisis.

It is my view that this dominant force suppresses volatility and maintains an upward bias on prices.

These programs are largely insensitive to longer-term macroeconomic developments, as they begin and end every day in cash, focusing solely on the current day's events. It is conceivable that they could bid up prices well beyond anything that the fundamentals can substantiate. Of course, if all of the machines decide to shut down at the same time, look out below.

Another consideration is how wealth is more concentrated today than it was ten or twenty years ago.

In fact, over the past thirty years the share of wealth held by the bottom 90% has declined from 35% to 22%, while the wealth held by the top 0.1% has gone from 5% to 22%. This can be seen in the chart below.

This could be having a measurable impact on stock prices that prolongs the current bull market. In my view, if stocks were held more broadly by the investing public, then prices would be more sensitive to any deterioration in the macroeconomic landscape and corresponding market fundamentals. The stock market would act more like the voting machine that recently upended the political establishment of both parties.

Lastly, the debt accumulation in the current cycle is being held by the federal government, which seemingly has an unending line of credit from the Federal Reserve. So long as the federal government can continue to borrow and spend to support the very modest levels of aggregate demand we have in our economy today, it could prolong the bull market.

My Bottom Line

Bulls may look at my experience as an investor and deduce that I'm twice burned, thus a third time shy. That is hardly the case, as I continue to hold stocks like Apple (NASDAQ:AAPL), Intel (NASDAQ:INTC), Time Warner (NYSE:TWX) and others that I have purchased during this bull market. I have also taken new positions in names like Unilever (NYSE:UL) and Qualcomm (NASDAQ:QCOM) since the beginning of the year. I am simply taking smaller positions, hedging my exposure through a variety of strategies, and holding much larger cash reserves given the macroeconomic headwinds that I now see.

I am not the same investor that I was in the 1990s or the 2000s. My priorities have shifted from fast cars and fun times to my oldest daughter, who will be attending the University of North Carolina at Chapel Hill next year, and with her two siblings, who are not far behind. My tolerance for risk continues to wane as I approach the age of 50, focusing on what I will have saved for retirement.

I can no longer put my faith and trust in a market structure that has failed miserably two times in just the past twenty years. I don't trust the intelligentsia on Wall Street, in Washington or at the Fed to do the right things, no matter how many times they claim to have everything under control. It is important to recognize that very little has changed since the last financial crisis, as we now begin to tear down the good regulations, along with the bad ones, that were designed to prevent another crisis from occurring. Therefore, I recommend investors stay vigilant in their pursuit of gains as the longest bull market on record continues and the macroeconomic headwinds gather. Ultimately, it will not be different this time.

0 comments:

Publicar un comentario