Champs or chumps?

China and currency manipulation

The government has been pushing the price of the yuan up, not down.

SINCE his election as president, Donald Trump has not softened his criticism of China over its alleged meddling to control the value of its currency, the yuan. On the contrary, he has called China “the grand champion” of currency manipulators. The kindest interpretation of this is that Mr Trump is out of date, as his own government could tell him.

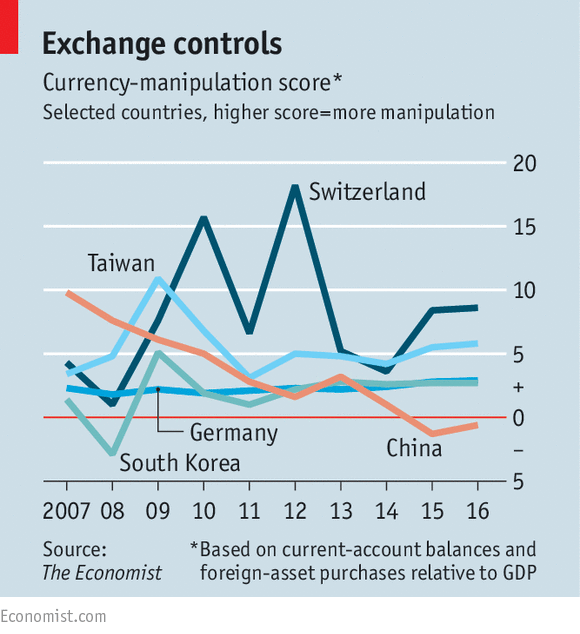

America’s Treasury makes a six-monthly assessment of the foreign-exchange policies of its big trading partners. The criteria it uses to identify currency manipulators are regarded by many economists as inadequate. They do not include, for example, the domestic purchasing power of a currency. Nevertheless, even by those flawed criteria, China is far from the champion. Indeed it seems to have quit the tournament altogether.

The Treasury uses three measures: whether the country runs a sizeable surplus in trade with America; whether its current-account surplus exceeds 3% of GDP; and whether it spends more than 2% a year to buy foreign assets to suppress the value of its currency. Over the past year, no country has checked all three boxes. China, in the latest report, only met one condition (running a big bilateral surplus in its trade with America).

The Treasury, does not publish a league table of its trading partners. If it did, it would illustrate just how slippery the idea of currency manipulation is. The Economist has used the measures to develop a crude scoring system, to establish which countries would be in Mr Trump’s firing line if his government’s measures were applied consistently (see chart).

Using the current-account metric, we award one “manipulation point” to countries with surpluses at the 3% threshold, two points to economies with surpluses at 6% of GDP, and so on. Similarly, we award one manipulation point for each 2% of GDP spent buying foreign assets to depress the value of its currency. We do not include bilateral trade with America in the scoring: the value of currencies affects trade globally, and some countries such as Mexico run hefty trade surpluses against America but have deficits with the rest of the world.

Awkwardly for America, two of its friends in Asia have recently scored more highly than China: South Korea and, most clearly, Taiwan. But the highest score of all goes to Switzerland, by dint of its whopping current-account surplus and its hefty foreign-currency purchases. This illustrates one of the method’s flaws: in terms of the goods and services that it can actually buy, the Swiss franc is in fact among the world’s most overvalued currencies.

As for China itself, it has been fighting to prop up the yuan in the face of capital outflows, and its score is in fact negative: it has, in other words, raised the price of its currency, not lowered it. Over the past decade, the scoring system shows that China has done progressively less to distort the yuan’s value. That is reflected in the International Monetary Fund’s verdict that the currency is “no longer undervalued”. Or, as Mr Trump might put it: Loser!

0 comments:

Publicar un comentario