“Trump-O-Nomics” – An

exploration of the proposals

As readers know, I have been doing a multipart series on the

proposed tax reforms for the last three weeks in Thoughts from the Frontline. My intention is to

finish this week. In part two I talked about what I like about the Better Way

proposal, and in part three I pretty much eviscerated the border adjustment

tax (BAT), which I think has the real potential to create a global recession.

You’ll need to read the series to see why, but a lot of it has to do with

simple game theory, which the measure’s Republican proponents are ignoring. If

you upset the equilibrium, the other partners at the table will change their

strategies, too.

Let me repeat that what I find encouraging about the proposed tax

reforms is that they are fairly radical in the sense that there is not an

obvious constituency for much of what is proposed, and it will require some

real leadership in Congress to get them passed. In the past I have proposed a

series of tax reforms (sometimes with my friend and fellow economist Steve

Moore, in op-eds around the country) that are pro-business/entrepreneur, but we

have always constrained our proposals by what we saw as political reality.

If the Republican leadership thinks they can get the BAT through

Congress, then I’m going to take the constraints off my thinking and propose

something that is even more radical but much more workable and would not come

with the negatives that the current Republican proposal does. (It is also

something that most economists would agree with, at least in theory.) It would

unloose a massive amount of entrepreneurial spirit and free up capital to go

where it can be most productive, AND it will balance the budget. My proposal

will makes the United States heads up more competitive vis-à-vis the rest of

the world world and yet allow other countries to respond in a similar fashion,

making their own economies more competitive but without their having to try to

outcompete with us and thereby hurt global trade. But that’s all for this

weekend…

Today I want to offer as your Outside

the Box an analysis of the current tax proposal from my friend

Constance Hunter, who is the chief economist at KPMG and wicked brilliant. We

spent some time in the Caymans last week talking about these issues, and she

graciously allowed me to send this internal KPMG document to you.

She analyzes the entire proposal and tries to be fair but comes up

with many of the same negatives that I do and a few more besides. One of the

things that Constance and a few readers have noted is that the real, forceful

change that is required to get this reform through Congress will mean that,

without Democratic support in the Senate, there will be an automatic sunset

provision in 10 years that would be devastating to the economy. There needs to

be a real effort to figure out how to create something bipartisan.

Further, in a conversation yesterday at lunch with a large family

farmer, he casually noted how farmers have to borrow money in the spring and

pay it back in the fall. This has been going on for hundreds of years and is

actually a quite well-documented phenomenon of banking cash flows. In the

1800s, New York bankers would game this dollar flow, but that’s a story for

another day.

By not allowing any interest-rate deduction, as the tax-reform

proposal seeks to do, you will simply destroy the family-farming community

nationwide. I think when farm-state Republican Senators realize what this

proposal will do, they will line up to oppose it. Which is good, because I

would really prefer not to see us plunged into a global recession.

One thing that Constance does well is to bring in other economists

and their papers and really get into how the economics community is thinking

about some of the major consequences of this tax plan. Again, it is not that

the current proposal doesn’t have many good features; it is that the bad ones –

which actually allow you to pay for the good tax cuts – go about it in the

wrong way and create serious problems.

Why is this so important? Because if we don’t come up with a tax

proposal that can get through Congress this year, then we’re looking at 2018;

and do you really think the stock market is going to levitate, waiting until

2018 for a tax proposal that’s not even on the table yet? Congress needs to

focus clearly and figure out what they’re going to do – and not do things that

would make the US and global economic situation even worse.

As investors and portfolio managers, we need to be paying

attention to what Congress is saying and doing and figure out how their actions

are going to affect the economy and our portfolios. The right policies and

programs could be very good for the markets. The wrong ones? You’d want to get

out of the way of that train.

As much as I enjoy traveling and the Caymans in particular, it is

good to be back in Dallas for a few weeks and trying to catch up. As I’ve been

hinting, we are getting close to announcing our new approach to portfolio

design and management. It will be available to everyone, but we are especially

looking to make it available to brokers and advisers to use with their own

clients. The team we have put together is actually quite large, and there are a

lot of moving parts to handle to make sure we’re ready for what I hope will be

a strong response when we launch. But getting all the materials and contracts

and agreements and compliance done in advance has been a bigger project than I

realized.

But then, that has been the story of my life. My friends and

partners can tell you that I start projects not realizing how huge they are

going to be until I’m in the middle of them. Kind of like my book on how the

next 20 years will look. What I thought was going to be a fairly

straightforward book is now massively complex, and part of the challenge is to

make sure it’s not a five-volume set but is actually a fairly thrifty overview

of the Age of Transformation.

And with that I will hit the send button and try to get back to my

inbox, plus take care of a lot of writing and research that I need to do. You

have a great week, and remember that no matter what the politicians do to us,

we’ll all figure out how to Muddle Through together.

Your appreciating the reality of complexity analyst,

John Mauldin, Editor

Outside the Box

“Trump-O-Nomics” – An

exploration of the proposals

By Constance Hunter and Jennifer Dorfman

KPMG US Economic Update

KPMG US Economic Update

As Donald J. Trump begins the presidency with promises of greater

GDP growth and job creation, this report examines both the cyclical and

structural backdrop that could impact the efficacy of his plans. The report

will also discuss the border adjustable tax proposal and some possible

implications. The analysis takes into account the more than 20 percent of U.S.

imports that are priced in dollars, a unique situation that alters the normal

currency adjustment assumptions economists make when assessing the impact of

such a tax.

It is debatable how much influence presidents can have over

near-term, cyclical, economic growth. Certainly expansionary or contractionary

fiscal policy has some influence, but in the United States, discretionary

government spending is a relatively small percent of GDP so this influence is

minimal. Presidents have more influence over structural aspects of GDP via

changes to regulation, changes to the tax code, and changes to total government

spending and resulting debt levels.

In terms of the cyclical prospects for the UnitedStates, the

recovery appears to be in about the 7th inning. The Federal Reserve Bank (the

Fed) is hoping its policies can create some overtime innings and a soft

landing; however, this is often the hope of central banks, yet few are lucky

enough to achieve such feats. The

largest constraint to the Fed’s goals is apparent tightness in the U.S. labor

market. For example, the National Federation for Independent

Business1 reports that the number of respondents who say there

are few or no qualified applicants for job openings exceeds the long-term

average of 42 percent. This suggests that even if the participation rate rose,

the lack of labor market depth would still pose constraints for business

expansion despite any new incentives from tax changes or other stimulative measures.

In addition to relatively tight labor supply, the Fed has just

raised rates for the second time in the current cycle. Since the election,

long-term interest rates have risen more than short-term ones due to

anticipation of more frequent rate increases in 2017 and some possible increase

in risk premia due to fiscal policy uncertainty. However, we believe the

biggest contributor to higher rates is the stronger U.S. economy that was in

train before the presidential election. In addition to cyclical momentum seen

in jobs and consumption growth, higher oil prices are supporting a return of

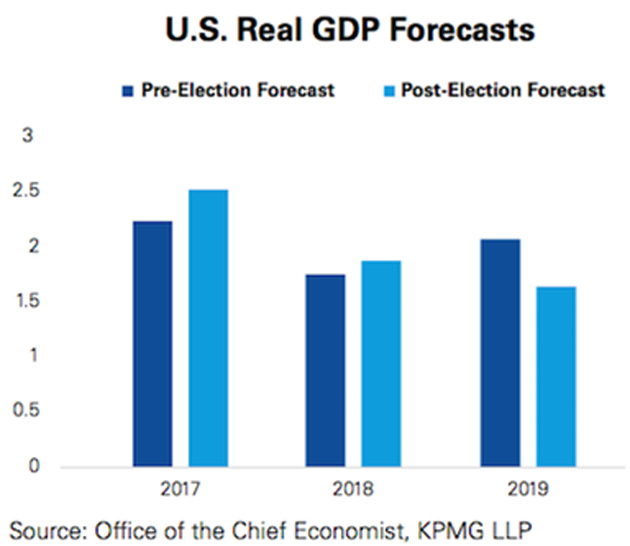

oil and gas investment. Our base forecast for growth in 2017 is now higher than

before the election due to strong growth momentum.

Therefore,Trump enters his presidency at the end of a long, if

tepid, expansion with little capacity for faster growth in the near term.

Nevertheless, during

the first 100 days, the Trump administration will want to achieve some quick

wins. One way to start this would be to streamline regulation.

A study from the conservative think tank, Heritage Foundation2 found

the cost of new regulations implemented since 2008 amount to an average of $15

billion a year spent on compliance. The argument suggests this is money not

spent on generating economic activity and it reduces productivity. Even if this

number is off by 50 percent, given that U.S. corporate investment has averaged

$130 billion a year since 2010, even

$7 billion of extra investment could add up to 50 basis points a year to

investment’s contribution to GDP.

In terms of fiscal stimulus from Trump’s tax policies,

it is important to remember that in addition to lower personal and corporate

taxes, there are proposals

that would create offsets to pay for the cuts. At the moment,

Republicans are united in saying that the tax cuts and offsets are part of the

same proposal and cannot be separated. Therefore,

their economic impact must be assessed in concert.

There is a good reason for the insistence by many Republicans that

spending not simply stay the same while tax revenue declines due to tax cuts,

as this would increase our already high 102 percent general government debt to

GDP levels. Here one can turn to a well-established phenomenon in economics,

the Ricardian Equivalence Theorem.3 Ricardian Equivalence

states that the economic outcome between debt financing and increased private

spending is equal.

Or put another way, there is no free lunch. If tax cuts cause the

federal debt to rise, then companies and households spend and invest less than

the amount of the cut. The

greater the debt level at the initiation of the tax cut the smaller the portion

that is spent or invested.

The first offset is a change

to the deductibility of interest. Under the current House Republican proposal,4 interest would no longer be deductible

unless it could be claimed against interest income.

While this is neutral for banks, in isolation it could hurt

heavily indebted industries, many private equity structures, and companies that

rely on debt versus equity financing. Proponents of the tax change argue that

reducing the tax benefits of debt financing would allow better allocation of

capital and would normalize the U.S. tax code with the rest of the world.

Nevertheless, most U.S.

companies will see an increase in their weighted average cost of capital

(WACC). According to outside estimates of the GOP proposal,

this would raise more than $1 trillion in additional tax receipts.5 However,

this change comes at a price. A November 2015 paper by RLG Forensics in

association with the Association for Corporate Growth predicts that “revenue

neutral” in terms of the federal budget is not the same thing as “impact

neutral” in terms of equity valuations or economic impact.6 Proponents

of the change argue that investment expensing and the reduction of the overall

corporate tax rate to 20 percent will offset the increase of the cost of WACC

in many cases. While this may be true eventually, the transition period is

likely to cause lumpiness in investment spending, which could well translate

into some quarters of negative growth.

The second offset, implementing a border adjustable tax, is

estimated to raise $1.2 trillion in tax revenue over 10 years. One main motivation for this

tax appears to be that it would discourage corporate inversions. As A Better Way7 notes,

“Taken together, a 20 percent corporate rate, a switch to a territorial system,

and border adjustments will cause the

recent wave of inversions to come to a halt.” However, other

claims that the change will now favor exports over imports ignores linkages

between imports, exports, and foreign exchange values. Perhaps more

importantly, if the tax

changes did reduce our imports, it would also reduce our standard of living, as

more goods and services would be sent to foreigners while receiving fewer goods

and services from them in return.8

Indeed the fact that in any given year 20–30 percent of U.S.

imports are priced in dollars means the J-curve effects of the currency

adjustment would likely take longer and could be adverse for importers of

commodities in the short term. Additionally, the linkages in global value

chains where many goods are priced in dollars, the long-term nature of

contracts, and general price stickiness throughout the value chain mean the

transition between implementation and complete currency adjustment could

disrupt U.S. and global GDP growth.

Nevertheless, many economists make several arguments in favor of a

border adjustable tax system.9

1. It would align more closely with the VAT system in most of our

trading partners where exports are not taxed but imports are.

2. Border adjustments reduce the incentive to manipulate transfer

prices by shifting to lower tax jurisdictions based on tax policy alone.

3. Border adjustments reduce the incentive to shift profitable

production activities abroad simply for tax benefits of lower tax jurisdictions

commonly known as corporate inversions.

4. Proponents argue that border adjustments are not trade policy, but

rather create a level playing field between domestic and overseas competition.

5. Border adjustments do not distort trade as exchange rates should

react immediately to offset the impact of these adjustments.

Many economists agree with most of these points. We concur largely

with points 1-3 and in the long run with point 5, although the implementation

phase could cause disruption that may have a significant near-term impact on

GDP. On point 5, the

reserve currency status of the United States blunts this negative impact. Our

research suggests that the reserve currency status of the United States and

integrated global value chains could slow the rate of currency adjustment with

adverse unintended consequences for world and U.S. growth. The

stronger U.S. dollar will raise prices of dollar priced goods for the rest of

the world which will, at some point, if not immediately, lower demand for these

goods. No immediate adjustment will take place on the 20–30 percent of imports

priced in U.S. dollars, and it will raise prices and lower demand of these

goods worldwide.

Raising $1.1 trillion in taxes means that cost must be borne by

some part of the economy either domestically or by trading partners. In the example below, the

tax law change simply shifts the burden of the tax to different types of

businesses.

Auerbach and Holtz-Eakin assume that the world price of the goods

remains the same and that the dollar appreciates to offset the border

adjustment. They also appear to assume that the good is priced in foreign

currency and no long-term contracts or integrated value chains are in place.

Economic theory suggests that the higher import tax cost in the example below

does not mean that the firm does worse after tax under the new system once the currency adjustment is

completed and the cost of imports falls due to the higher value of the U.S.

dollar. Under the new law, the firm in the example below can

deduct only 20 of its purchases rather than 30 because 10 represents the

imported amount. However, as Auerbach and Holtz- Eakin’s paper explains, the

import costs will adjust to be 8 in dollar terms, rather than 10, if the tax

rate is 20 percent. This means that the firm’s after-tax cash flow will be the

same in the two cases; 80 percent of 15 = 12 under the current system, and 80

percent of 25 = 20 – nondeductible expenses of 8 = 12 under the new system.

We worry that this assumption is a bit too neat and the real-world

adjustment will be less smooth and not immediate. As the home of the reserve

currency, U.S. importers have the significant advantage of never having to

worry about currency price fluctuations (in particular a devaluation of the

dollar) impacting the purchase cost of commodities and many other goods that

are part of the global value chain. There are other advantages such as

significant demand for U.S. Treasuries keeping U.S. borrowing costs lower than

they otherwise would be. But the chief advantage for the purpose of analyzing

the border adjustable tax is that commodities trade in U.S. dollars.

The example put forth by Auerbach and Holtz-Eakin assumes the

exchange rate absorbs the tax change and the cost evaporates in currency

fluctuations. The tax law

change would then encourage investment as its full expensing regime makes this

activity more attractive; it would also blunt the impact from

the import tax. It is implicitly assumed that this greater investment will

translate into greater economic activity and yield a higher growth rate. One

may also assume one has a can opener.10

Over the long term, it seems reasonable that the proposed tax law

change would simplify the code, which in and of itself could allocate scarce

resources to better use thereby improving GDP. However, the transition to the new system as laid out in A Better Way does raise some questions, a few of

which are outlined below.

1. The assumption that all traded goods are priced in foreign

currency is a key part of most exchange rate models that one can apply to this

situation. Examples such as the Bickerdike-Robinson-Meltzer Model assume the

supply and demand schedules shift downward by the same proportion as the

appreciation.11 It also assumes the good is priced in foreign

currency terms, which for the United States is not the case for 20–30 percent

of its imports in a given year.

2. The demand elasticity is not the same for each imported product so the currency adjustment on a good-by-good basis may not be

equal to the tax change. Therefore, some importers would be more or less

advantaged as would some exporters.

3. With no offsetting tax cut, a

rise in the value of the dollar would hurt exports. With the

reduced corporate tax, exporters would presumably have room to lower the price

of their goods in line with the amount of the appreciation of the currency.

However, this transition is likely to be “lumpy” and could reduce exporters’

revenues during the transition period and beyond.

4. Not all importers are engaging in corporate inversion or are

importing goods because of tax reasons. Global

value chains (GVCs) have become increasingly integrated. In 2011, nearly half of world trade in goods and

services took place within GVCs, up from 36 per cent in 1995.12 This

is due in part to labor cost differentials, in part to sourcing of raw materials,

and in part to expertise in certain products and services. Thus, changing the

way imports are taxed for U.S.-domiciled companies is likely to cause

disruption to globally linked supply chains many U.S. multinational companies

have in place.

5. The J-curve effect means that there is a lag between when a

currency change takes place and the physical change in imports or exports is

realized in the current account balance. Usually orders that existed before the

currency move have yet to be paid for, thus the J-shaped change in the trade

balance immediately following a substantial currency move. A stronger dollar should increase the

current account deficit over time as U.S. dollar exports become more expensive

to our trading partners. Additionally, the immediate effect

would be a reduction in the current account deficit. This would be an addition

to GDP but it would also correspond to a significantly smaller capital account

surplus and would likely negatively

impact the U.S. equity market and increase U.S. interest rates, all other

things equal.

6. The idea of wanting to stimulate exports, reduce imports, and

reduce our current account deficit ignores the other side of this accounting

identity, the capital account. As Ruddy Dornbusch wisely noted, “The flow of

investment and the changes in the value of real capital potentially dominate

the effects of current account imbalances. A good week on the stock market

produces a change in wealth that is several times the magnitude of an entire

year’s deficit in the current account. Although it is true that the current

account is important because persistent current imbalances accumulate, exactly

the same argument can be made for investment.” A persistently lower current account deficit would equal a

persistently lower capital account surplus and over time higher interest rates

and lower stock market returns. Conversely, a high current

account deficit means there is a higher capital account surplus and an

abundance of capital in the U.S. market. This is also a function of our reserve

currency status; foreign holders of U.S. dollars need to invest their holdings

in U.S. assets. Therefore,

one can argue that the benefit to the economy overall of running a current

account deficit and a capital account surplus not only outweighs the costs, but

is a corollary to reserve currency status.

7. While it is commonly known that commodities trade in U.S. dollars,

it is likely less widely known that much of the global value chain of

intermediate goods also trades in dollars. This is in part because the U.S.

consumer base is the largest in the world which reinforces the United States’

reserve currency status. If at the margin a border adjustable tax caused fewer

goods to be priced in dollars, it could have the unintended consequence of pushing

the U.S. dollar further from reserve currency status.

There are of course other aspects of the A Better Way blueprint that

could have unintended consequences. The list above is meant to stimulate

thought and improvement of the plan and its implementation.

While some theory does support the idea that it would improve U.S.

GDP, there are a lot of assumptions that cannot be counted upon. It cannot be

overstated that while a major tax overhaul of this kind could in the long run

benefit the U.S. economy, the

transition is likely to be lumpy and could even see some quarters of negative

growth as adversely impacted firms or industries suffer or go

out of business.

The comprehensive and sweeping nature of the proposed tax changes

and the fact that they will be much more effective if they are permanent means

that the GOP will want to

be strategic in the way they pass the bill.

There are two

options that would eliminate

the need for a sunset provision. The first would require at

least eight Democrat senators to sign on. This means that compromise will alter

the current proposal. It also means that passage before the end of 2017 will be

difficult. Reagan’s 1986 tax law change took three years to negotiate and this

tax bill will take time as well. The second way the GOP could make the law

permanent is the so-called reconciliation process. This is only possible if the

law does not increase the deficit in any year beyond the official 10-year

budget window. Some believe this is their current plan—to construct the bill in

such a way to be revenue neutral or positive in years 11 and beyond. This too

would require significant changes to the current law. The Tax Policy Center assumes the

current plan adds to current deficit levels by $3.3 trillion over the first

decade.

In the meantime, it is expected the U.S. dollar to be the most

immediate asset to anticipate this change in policy over the course of 2017.

Any move in the dollar will be buttressed by the interest rate differential

between the U.S. and other high- grade government debt markets. Higher interest

rates will put pressure on Trump to achieve GDP wins early as it will reduce

U.S. exports, increase imports, and have a negative effect on GDP. Therefore, as stated above, regulatory

changes are expected to be sweeping withinTrump’s first 100 days.

However, even this is not a panacea as many of these changes will be seen in

the energy space where the

value of a barrel of oil will be just as important in determining investment

levels as regulatory changes. Remember, a stronger dollar

reduces the demand and price for oil in foreign currency terms, all things

being equal.

Therefore, it is fair to say that Trump’s 4 percent growth target

faces challenges from both structural and cyclical factors. Streamlining regulation is

Trump’s best bet for a quick win on increasing GDP.

__________

1 NFIB, Haver Analytics

2 Gattuso & Katz, (2016) “Red Tape Rising,” Heritage Foundation

3 Buchanan, James M. (1976) “Barro on the Ricardian Equivalence Theorem,” Journal of Political Economy

4 A Better Way (2016) Better.gop

5 Nunns, Burman, Page, et al (2016) An Analysis of the House GOP Tax Plan, TaxPolicyCenter.org

6 Morris, (2015) Eliminating the CIT Deduction: Valuation Implications for Middle Market Enterprises. RLG Forensics

7 A Better Way (2016) Better.gop

8 Viard,(2009) Border Tax Adjustments Won’t Stimulate Exports, AEI.org

9 Auerbach and Holtz-Eakin, (2016) The Role of Border Adjustments in International Taxation, AAF.org

10 A can of soup washes ashore. The physicist says, "Lets smash the can open with a rock." The chemist says, "Let's build a fire and heat the can first." The economist says, "Let’s assume that we have a can opener.” Crickets.

11 Bickerdike-Robinson-Meltzer (1975), Vol 65, no 5 American Economic Review

12 Trade in value-added and global value chains: statistical profiles, WTO, wto.org

2 Gattuso & Katz, (2016) “Red Tape Rising,” Heritage Foundation

3 Buchanan, James M. (1976) “Barro on the Ricardian Equivalence Theorem,” Journal of Political Economy

4 A Better Way (2016) Better.gop

5 Nunns, Burman, Page, et al (2016) An Analysis of the House GOP Tax Plan, TaxPolicyCenter.org

6 Morris, (2015) Eliminating the CIT Deduction: Valuation Implications for Middle Market Enterprises. RLG Forensics

7 A Better Way (2016) Better.gop

8 Viard,(2009) Border Tax Adjustments Won’t Stimulate Exports, AEI.org

9 Auerbach and Holtz-Eakin, (2016) The Role of Border Adjustments in International Taxation, AAF.org

10 A can of soup washes ashore. The physicist says, "Lets smash the can open with a rock." The chemist says, "Let's build a fire and heat the can first." The economist says, "Let’s assume that we have a can opener.” Crickets.

11 Bickerdike-Robinson-Meltzer (1975), Vol 65, no 5 American Economic Review

12 Trade in value-added and global value chains: statistical profiles, WTO, wto.org

0 comments:

Publicar un comentario