The Fool And His Money

by: Lawrence Fuller

- Proposals for tax reform and a new healthcare plan have led to a surge in consumer confidence.

- A subsequent rise in investor sentiment has lifted the stock market to new all-time highs.

- Yet there is a massive disconnect between expectations and the fiscal reality, which will have significant ramifications for the economy and markets.

- A subsequent rise in investor sentiment has lifted the stock market to new all-time highs.

- Yet there is a massive disconnect between expectations and the fiscal reality, which will have significant ramifications for the economy and markets.

Under the guise that history repeats itself or at least rhymes, let me share with you the picture below, which hangs framed in my office. It is a full-page cartoon from an 1899 original edition of Puck magazine, which I understand was similar to "The Daily Show" today. The reason that this picture resonates with me now has as much to do with the characters in the cartoon as it does with the caption beneath it. It is titled, "The Fool and His Money." Don't jump to conclusions about who the fool might be today, as I think that has yet to be determined.

The caption beneath the title is a quote from John W. Griggs, who was U.S. Attorney General at that time. He states that "with reference to these large combinations of capital which are now forming, my own judgment is that the danger is not so much to the community at large as it is to the people who are induced to put their money into the purchase of stock." The cartoon depicts elated investors eagerly throwing their money at a stock-peddling promoter, who smiles as he sits atop a ticker tape machine.

I shared this picture in one of my previous writings, in which I compared the stock promoter to the Federal Reserve, inducing investors to buy risky assets with its zero-interest-rate policy. P

erhaps that comparison is still valid today, considering the Fed's unwillingness to raise interest rates any further, despite professing that our economy has near-fully healed.

What I see in this picture today is a new administration that sits atop Washington, but instead of promoting outsized gains on risky financial assets to individual investors, it is promising economic benefits in the form of tax cuts and a new healthcare plan to middle-class Americans.

In turn, the American public is throwing its vote of confidence behind this administration in expectation that it will receive these benefits, and the investing public is following by propelling the stock market (NYSEARCA:SPY) to new all-time highs.

I was very enthused to hear President Trump proclaim that there would be "massive tax cuts for the middle class," as recently as this week during one of his press conferences. I've also been encouraged by Trump's assertion that the Obamacare replacement will "take care of everybody," and that it will do so for less money. He stated that we "can expect to have great healthcare. It will be in a much simplified form, much less expensive and much better." These would both be extremely positive developments for the economy and the market and the majority of Americans are clearly taking him at his word.

Consumer Confidence

We have seen a surge in consumer confidence since the presidential election. According to the University of Michigan's survey, consumers "anticipated the most positive outlook for their personal finances in more than a decade." It was also noted that this elation was "based on political promises, and not, as yet, on economic outcomes." The Conference Board's survey revealed similar results, but what was notable in its report was that the greatest surge in confidence came from the income level of $35-50K, which constitutes a large segment of the middle class. A thriving middle class is a critical component to a strengthening economy that has sustainable growth.

Investor Sentiment

Investors have responded to the President's proposed agenda and the surge in consumer confidence that followed, by lifting the stock market to new all-time highs. There is so much enthusiasm that short-sellers have deserted the marketplace. This is a complete reversal from where we stood nearly one year ago.

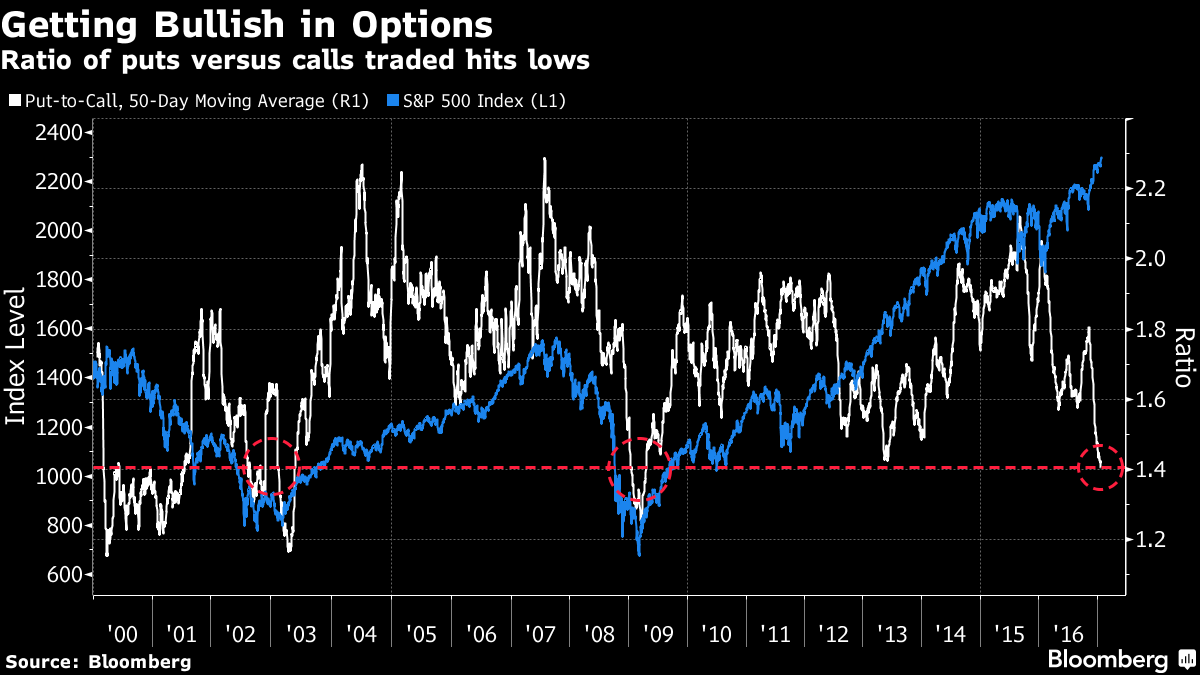

Additionally, speculators are using call options to bet on a continued rise in the S&P 500 index relative to the number of put options being used to make bearish bets at a rate not seen since 2009. In other words, the number of bearish bets being made on the S&P 500 index relative to the number of bullish bets has fallen to a level seen only after the tech bubble burst in 2000 and at the height of the financial crisis in 2008. Yet, the market was bottoming during those periods, whereas it is at all-time highs today.

This put-call ratio could be interpreted as either an extremely bullish sign, based on historical precedent, or as extremely bearish, considering that we are at the opposite end of the spectrum today in terms of the valuation of the S&P 500 index, as well as the stage of the business cycle.

What is clear is that very few investors are concerned about downside risk at this point. I think that what transpires moving forward will depend on whether or not the surge in confidence for the vast majority of American households is validated by legislative outcomes that benefit them in the months ahead. This is where I have grave concerns.

Fiscal Reality

In every statistical analysis from either side of the aisle of proposed tax reform that I have reviewed, whether it be from the Trump administration or the Republican leadership, I see no meaningful tax cuts for the middle class. In some cases, taxes increase for single parents with dependent children and married couples with at least three children. The vast majority of the tax relief goes to the wealthiest households and corporations. Irrespective of whether this is good policy or not, today's consumer confidence numbers will likely plummet if this is the fiscal reality.

Furthermore, it is impossible to provide "great healthcare" that covers everyone for less cost.

My suspicion is that the replacement plan will offer access to great healthcare if you can afford it. A family of five with $50,000 in household income which is currently covered by the Affordable Care Act is probably receiving a subsidy that covers 80% of the premium charged by the healthcare provider. If these subsidies are eliminated or reduced, it will serve as a tax increase on those middle-income households that choose to retain their insurance. Irrespective of whether this is sound policy or not, it will be a rude awakening for the millions of lower-to-middle income households that are expecting to have "great healthcare" at a lower cost.

This is not about politics. It is about a gargantuan disconnect between investor sentiment, the consumer confidence that this sentiment is partly based upon and the economic reality that the majority of middle-class American households face moving forward. We just learned this morning that the rate of year-over-year wage growth in January declined from 2.8% to 2.5%.

In two weeks we will likely learn that inflation-adjusted wages are now declining even further. I don't see current tax or healthcare reform remedying this situation.

Market Implications

If you believe that the success of the overall economy is dependent on a rising tide that lifts most boats, then you can see that we may have a problem. Corporate revenues and profits are largely dependent on the rate of US economic growth, and this will be even more pronounced under the new administration's trade policies. The rate of economic growth is largely dependent on consumer spending. That spending is fueled by income growth. If the majority of the benefits of tax reform go to corporations and wealthy households, that money will be saved, invested or used to repurchase stock and pay dividends. This does not spur economic activity.

Furthermore, the Affordable Care Act may have been a disaster in the making, but it was a form of fiscal stimulus. Any replacement that reduces existing benefits will serve as a form of fiscal restraint, slowing the rate of economic growth. It will be particularly painful for the millions of households that lose their benefits or are forced to pay more for what they have now.

So who is the fool? Or better yet, who is being fooled? My fear is that it is the typical middle-income household, expecting as dramatic an improvement in its economic situation as current confidence measures indicate. If that is so, then investors are also being fooled, because they are investing on the basis that this confidence will translate into much faster rates of economic growth and corporate profitability.

0 comments:

Publicar un comentario