Going Deep

by: The Heisenberg

- We're all fascinated by how markets have reacted to Trump's policy proposals.

- But are we looking at the right markets?

- It may well be that we need to look under the hood (so to speak) to get the real story.

- But are we looking at the right markets?

- It may well be that we need to look under the hood (so to speak) to get the real story.

There are a lot of perks to working from a barstool - most of which are obvious.

But one I didn't fully appreciate until recently was the extent to which operating from a laptop frees me from the tyranny of multiple monitors.

Up until mid-November of 2016, the "number of monitors"/"efficiency" correlation was strongly positive. Sure, the law of diminishing returns kicks in at some point (you wouldn't want to have say, a dozen monitors), but generally speaking, the more screens you have, the easier it is to keep track of markets while simultaneously reading and producing research.

Well, that all changed with the election. As of November 9, the "number of monitors"/"efficiency" correlation turned negative. That is, the more monitors you have, the less efficient you are.

Why? Well, because stocks (NYSEARCA:SPY), bonds (NYSEARCA:TLT), and the dollar (NYSEARCA:UUP) became so highly correlated that it was easy to find yourself watching charts of the 10Y, S&P futs, USD/JPY, and 10Y bunds as though you were watching the latest episode of Homeland. That is, it was tempting to literally sit there and watch them react to the tape in real time.

The reflation trade became (and still is) a running referendum that tracks the market's take on Donald Trump and, by extension, on the prospects for the US economy.

The obsession with these headline-friendly asset classes has led to voluminous output from sellside strategists. The problem - and this goes for me as well - is that the closer you track the numbers, the more sensitive you become to small changes. Eventually, you find yourself reading too much into it.

Every blip is suddenly consequential. You're soon trying to fit the reflation narrative to the tiniest of moves. Once that mentality takes hold, everything you write is by definition out of date by the time you post it.

So it's a blessing to get away from the desk where the multitude of screens conspire to distract me from my work.

The funny thing is, for all the focus on rates, the dollar, and equities, we may actually be looking at the wrong numbers when it comes to getting the market's take on Trump and the prospects for the economy. Put simply: watching bonds, stocks, and the broad dollar might be a decidedly amateurish way to go about things.

It could be that we need to go a bit deeper to get a more nuanced read on whether and to what extent markets are pricing in reflation and/or a return to the dynamics that prevailed pre-crisis.

As you're probably aware, the legacy of 2008 finds expression in a variety of distortions created by policymaker meddling (well intentioned or not). Sweeping regulatory change and a bonanza of central bank easing played havoc with existing market dynamics and, unsurprisingly, there have been unintended consequences.

Over the summer, I used a pop culture reference (the Training Day post) to explain why it's important to discuss the implications of money market reform. A few days later, I used a short vignette (the drunken Albanians) to pique reader interest in a post about how that same money market reform has knock-on effects for seemingly esoteric asset classes. The reason I spent so much effort crafting those posts in a way that would keep readers engaged is simple: money market reform and its effect on LIBOR are extremely important subjects that are often assumed to be irrelevant to the average investor despite the fact that they not only impact markets but also say something about how the best laid plans (i.e. post crisis regulatory reform) can go awry.

Well, now it's time to revisit the notion that everyone (that is, "pros" down to "average" investors) needs to have some familiarity with corners of the market that might, at first blush, seem opaque or otherwise immaterial to our daily reaction functions.

In a new note, Deutsche Bank is out reiterating the very same points I made last summer regarding the importance of staying informed. Here are a few introductory excerpts (my highlights):

The Trump administration hopes to jolt the economy out of its post-crisis mire of slow growth and low inflation with a dose of fiscal spending, tax reform and deregulation. Understandably, markets were enthusiastic, with the dollar rising on expectations of stronger US growth, stocks moving higher anticipating corporate tax cuts and bond prices falling on concerns about higher future inflation.

Even as these marquee markets have settled into a wait-and-see posture in recent weeks, they continue to price in "normalisation" to varying degrees.

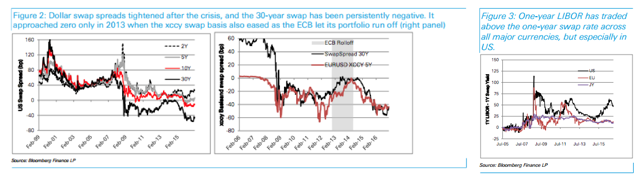

But other important, albeit less well-known, markets remain oblivious to this postelection shift. Long-end US swap spreads are still negative, the cross-currency basis for dollar against the euro and yen remains persistently wide, and the dollar LIBOR/swap spread remains elevated. These levels were hardly the norm before the financial crisis and indicate a banking system still operating far from normal.

These are not niche sectors investors can safely ignore. Rather they are key markers of the health of the banking and financial system.

Those last two sentences could have easily come from a Heisenberg article written in the dog days of summer 2016.

Deutsche Bank's contention is that several of the supposedly "complex" topics I've discussed in these pages over the past eight months (cross-currency bases, swap spreads, and the money market reform-induced rise in LIBOR) are perhaps better indicators of what the market is actually expecting from the Trump administration.

Thus, to the extent these "esoteric" concepts were important before, they're even more important now. Here's Deutsche again:

Beneath the surface less visible but essential markets have yet to respond in a material way to what might happen in the next year or so. Since the crisis, the cross-currency swap and interest rate swap markets and term LIBOR have traded at dislocated levels relative to long-standing pre-crisis norms - and continue to do so. While lacking the headline power of equities and government bonds, these are not niche markets; on the contrary they are deep, liquid and global. And now more than ever, all investors need to pay attention to these markets because they will likely provide a litmus test for the success of the new administration's policies.

Again, that sounds like something I would write.

I have been over and over the global dollar shortage (see here for the latest), how money market reform exacerbated it, and how it manifests itself in widening cross-currency bases.

Here's Deutsche Bank's take (my highlights):

Here's Deutsche Bank's take (my highlights):

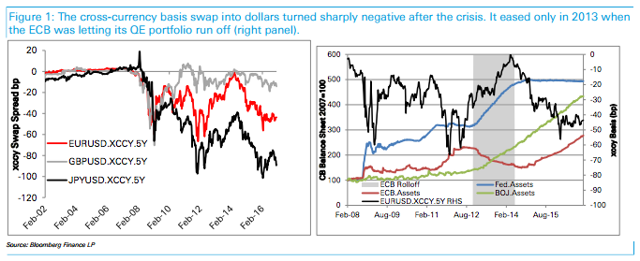

Before the crisis the cross-currency basis swap from euros, pounds and yen into dollars (lend currency X; borrow dollars) traded in a narrow band near zero (Figure 1).

During the crisis the xccy basis (or cost of borrowing dollars) turned sharply negative due to a lack of dollar funding and heavy demand for dollars. But rather than return to normal as things settled down it remained negative and traded in a much broader range. Today, the euro-dollar xccy swap (lend euro/borrow dollars) is about minus 44 basis points; the yen-dollar basis is about minus 89 basis points.

There are all kinds of things that have contributed to the widening out of cross-currency basis swaps, many of which you can read about by starting with the piece linked above and working your way back through my previous posts (each successive piece links to the ones before it).

There are all kinds of things that have contributed to the widening out of cross-currency basis swaps, many of which you can read about by starting with the piece linked above and working your way back through my previous posts (each successive piece links to the ones before it).

The thing to note for our purposes here is that the phenomenon shown in the right pane above is at least in part attributable to regulation and central bank intervention in markets. That's the common thread between distortions in cross-currency bases, swap spreads, and LIBOR/swap spreads. To wit, from Deutsche again (my highlights):

The primary explanation for negative swap spreads in the US is strong demand for duration in a falling interest rate environment. Another factor may be more rigorous collateral requirements in the post-crisis period that ameliorate much of the credit risk factor. And again, balance sheet constraints have kept banks from taking the other side of these trades as they did before the crisis. Still that leaves open the question of why swap spreads haven't turned less negative during the recent bond market sell-off following the election result.

The recent significantly wider LIBOR/swap spread in the US is a direct consequence of money market reforms introduced in October 2016. Under these regulations, US money market funds can guarantee a $1 redemption price only if they invest in short maturity government securities. 6Other so-called prime money market funds can invest in a broader range of securities but are now are subject to mark-to-market requirements. As result about 1tn dollars (or three-quarters of mid-2015 balances) moved from prime money market funds to government funds beginning in late 2015.

Prime funds had been a key source of funding for banks, mostly by buying bank commercial paper and certificates of deposit. As this source of funding evaporated, the rates on unsecured loans to banks (LIBOR) rose sharply, especially for longer maturities, reflecting the scarcity of term funding.

Now whether or not you fully understand all of that is largely immaterial for this particular post, and as I said, those interested in tracing all of this back to previous posts of mine can readily do so.

Now whether or not you fully understand all of that is largely immaterial for this particular post, and as I said, those interested in tracing all of this back to previous posts of mine can readily do so.

The salient point for our purposes here is that Trump has promised to roll back the regulations that have in some cases facilitated and exacerbated the distortions highlighted above and there's also a sense that central banks will be better able to normalize policy in a world where growth is "great again" thanks to Trumpian fiscal policy.

"In short, the standard explanations for dislocations in all three markets (xccy basis swap, term US interest rate swap and term LIBOR) revolve around some combination of central bank policy, supply and demand forces, and constrained bank balance sheets that cannot offer the degree of liquidity they did before the crisis," Deutsche Bank says, summing up.

But there are problems. Lots of them. Not the least of which is the very real possibility that the divergence between Fed policy and policy at the ECB and BoJ leads to still more demand for USD assets.

Additionally, the repatriation of dollars under a Trump tax holiday could suck more dollar liquidity out of global markets as could a reduction of imports from Asian economies.

The key then, is whether the positive effects of a potential rollback of regulatory constraints (e.g. banks become market makers again) end up being sufficient to offset the potentially negative impact of Trump's other policy proposals. To the extent cross-currency, rate swaps, and term LIBOR markets don't begin to show signs of normalization soon, we may be able to infer that the market actually doesn't have much faith in Trump's ability to mitigate the dynamics that have created distortions.

So if you're looking for a real referendum on the extent to which the market believes a return to normalcy is imminent under Trump, you may have to lift up the hood or "go deep" - as painful as that may be.

I'll give the last word to Deutsche Bank:

If it become apparent that whatever reforms are destined to bypass these obscure but vital markets we have to wonder how far the Trump market can run - whether up in equities and down in bonds.

0 comments:

Publicar un comentario