Buttonwood

Financial markets diverge as central banks start to turn off the taps

As monetary policy tightens, markets are learning to let go of Daddy’s hand

.

INVESTORS are learning to let go of Daddy’s hand. Monetary policy has been very supportive of asset markets over the past eight years but the direction of policy is tilting slowly.

The Federal Reserve has increased rates twice already and is expected to push through another three increases this year. The Bank of England has indicated that the next move in rates could be up or down, but that the former looks more likely, especially as inflation is on the rise. The European Central Bank is scheduled to reduce the amount of bond purchases it makes after the end of March.

Only the Bank of Japan seems committed to keeping the monetary taps on “full”.

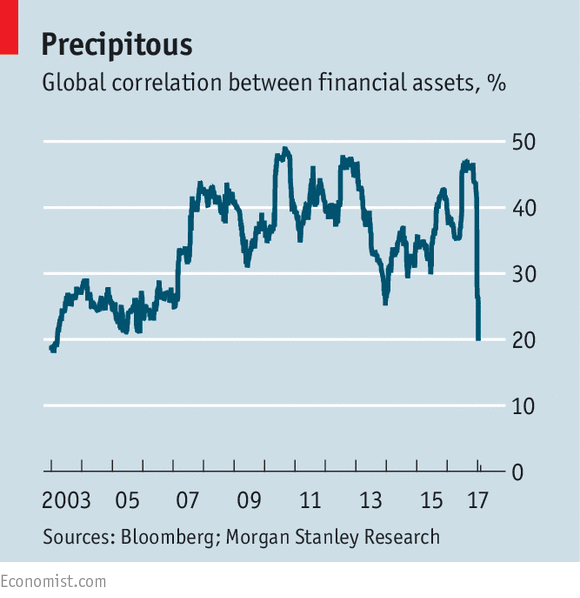

The market impact is already visible. Morgan Stanley says there has been a “crash” in the tendency for assets to correlate with each other in recent months (see chart). Its measure incorporates correlations between different markets (equities and corporate bonds, for example), and between different regions.

The recent fall in correlations takes the measure back to where it was in the run-up to the 2007-08 financial crisis. During and after the crisis, correlations rose sharply. First, many investors sold out of risky assets because of the collapse in the financial system. Then, as central banks started to buy bonds through several rounds of quantitative easing (QE), most financial assets rose in tandem.

Now that central banks are no longer quite so supportive, it may be time for markets to go their separate ways. The actions of central banks swamped the economic fundamentals; those factors can now reassert themselves. In the first few weeks after Donald Trump’s victory in the presidential election, the value of global shares rose by $3trn and that of bonds fell by the same amount, according to Torsten Slok of Deutsche Bank. The Dow Jones Industrial Average passed 20,000 for the first time on January 25th. Emerging markets have underperformed American shares since Mr Trump’s victory.

The rationale behind such differences is that tax cuts in America will improve economic growth (good for equities) but widen the budget deficit and push up inflation (bad for bonds). Mr Trump’s threats of tariffs and border taxes will be good for domestically focused American companies, less so for businesses operating in developing countries.

The tricky question is how long these divergences can last without prompting a reaction. At some point, higher bond yields, by raising the cost of borrowing, can crimp economic growth and thus be bad for equities. Bad news for emerging markets can rebound on the developed world.

Some of these tensions may play out in the currency markets. They too changed after the 2007-08 crisis. Before the crash, the markets were driven by the “carry trade”, with investors tending to borrow in currencies with very low rates and invest the proceeds in countries with higher rates, pocketing the difference, or carry.

Once rates fell towards zero across the developed world, there was less carry to exploit. But monetary policy still played a big role; announcements of QE programmes were seen as a sell signal. For a while, it seemed that most central banks were trying, implicitly or explicitly, to drive their currencies lower.

Now there may be some carry to exploit again. The gap between ten-year Treasury-bond yields and German bond yields has widened to more than two percentage points. America was the first leading economy to scale back QE and the first to start raising rates; as a result, the trade-weighted dollar has risen by nearly 35% since August 2011.

A stronger greenback creates its own feedback loops. It causes problems for companies in emerging markets that have borrowed in the currency. And, over time, a stronger dollar makes American exporters less competitive and developing-country exporters more so.

That thought has already led President Trump to describe the dollar as “too strong”—a remark that, along with his early actions on trade, has prompted the currency to drop back a bit. However, what the president says about the dollar does not really matter. It is the Fed that makes the big decisions that drive the currency.

That might change. Mr Trump may bridle at his lack of control over dollar movements. He could try to bully Janet Yellen, the Fed’s chairwoman—as Richard Nixon dominated an earlier chairman, Arthur Burns. Or he might replace her with someone more pliable. The end of central-bank independence really would create a new and unwelcome environment for investors.

0 comments:

Publicar un comentario