How Barack Obama rescued the US economy

Given the starting point, and congressional opposition, recovery has been remarkable

By Martin Wolf

How should we assess the economic success or failure of Barack Obama’s presidency?

This is a difficult question to answer. After all, the incumbent of the White House cannot determine the performance of the huge and complex US economy. Indeed, policy initiatives usually have a modest impact. But the story of Mr Obama’s presidency is a little different from the usual, since it began amid the worst financial crisis since the 1930s. If we consider the disaster he inherited and the determination of the Republicans in Congress to ensure he would fail, his record is clearly successful.

This does not mean it is perfect. Nor does it mean the US confronts few economic challenges. Neither statement would be close to correct. Yet it does mean he has laid a strong foundation.

The latest Economic Report of the President analyses the Obama record. It is also the brief for the defence. But Mr Obama’s Council of Economic Advisers does first-rate analysis. This report is no exception to that rule.

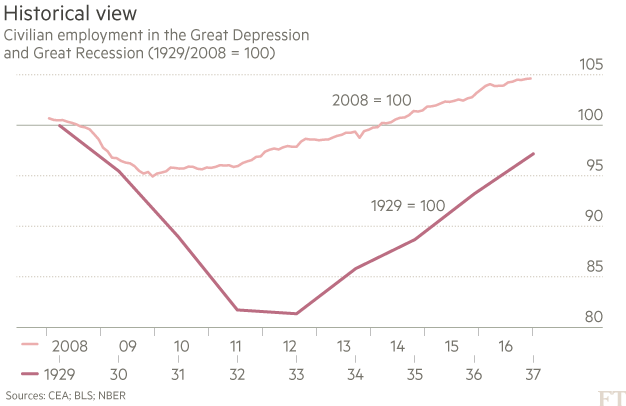

The starting point must be with Mr Obama’s inheritance: the economy was in free fall in early 2009.

As the report notes, perfectly correctly: “It is easy to forget how close the US economy came to an outright depression during the crisis. Indeed, by a number of macroeconomic measures . . . the first year of the Great Recession . . . saw larger declines than at the outset of the Great Depression in 1929-30.”

Responsibility for the successful recovery does not rest with this administration alone: the administration of George W Bush was responsible for the immediate response (though bearing some responsibility for the severity of the crisis); the US Federal Reserve acted effectively; and Congress passed important legislation. Yet, shockingly, most congressional Republicans opposed all significant monetary, financial and fiscal actions taken to deal with the crisis.

The Obama administration implemented a number of important fiscal measures, notably the American Recovery and Reinvestment Act of 2009. It also provided strong moral support for the Fed (including the reappointment of Ben Bernanke, who had been President Bush’s nominee). The administration also restored the financial sector faster than expected and carried out a highly successful rescue of the car industry.

Meanwhile, Republicans decried the fiscal stimulus, complaining about the huge fiscal deficits caused by the crisis. Yet it was as absurd to complain about deficits then as it is to slash taxes now, when the economy seems close to full employment.

Some Republicans claimed Fed policies risked hyperinflation. Most opposed the re-regulation of the financial sector and savaged the bailout of the car industry. Yet President-elect Donald Trump might not be in a position to bully automakers today if they had not been rescued back then.

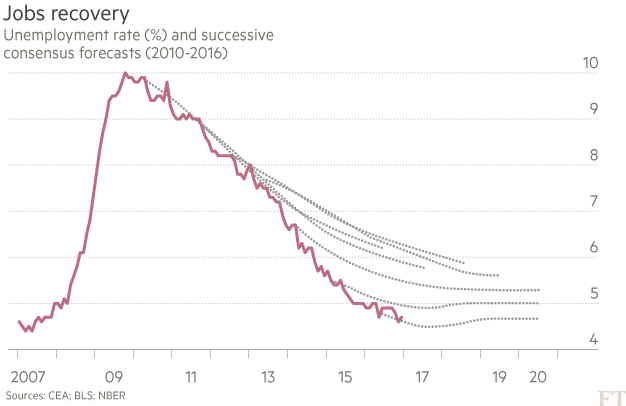

In all, given the starting point, the performance of the economy has been remarkable. The unemployment rate has consistently fallen faster than expected. US business has also added 15.6m jobs since private-sector job growth turned positive in 2010. Real wage growth has been faster in the present cycle than in any since the early 1970s. In the third quarter of 2016, the economy was 11.5 per cent bigger than at its pre-crisis peak and real gross domestic product per head was 4 per cent above the pre-crisis peak, while that of the eurozone was still below it. Household net worth has also reached 50 per cent above its 2008 level.

Yet Mr Obama was interested in more than economic recovery. He tried to move the US closer to the universal health insurance taken for granted in other high-income countries. The Affordable Care Act (“Obamacare”) has added an estimated 20m adults and 3m children to the insurance rolls. Healthcare costs have also grown exceptionally slowly since the law was enacted, relative to past US performance.

These are all genuine achievements. Yet some problems could not be cured.

First, US economic outcomes have become exceptionally unequal, despite a modestly progressive shift in the impact of fiscal policy under Mr Obama. Doing something effective about this was beyond his powers, both because it is difficult and because his opponents had no interest in helping.

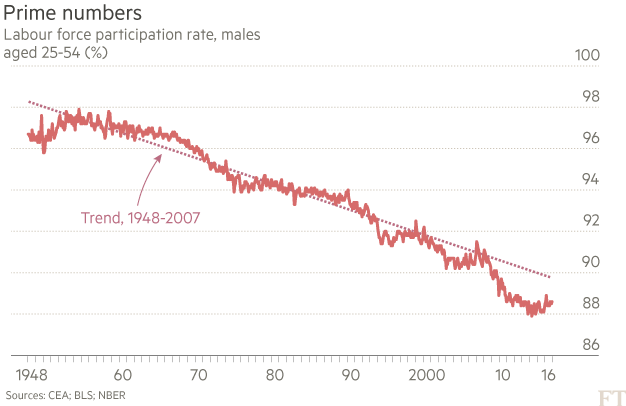

Second, the participation in the labour force of prime-aged males (25 to 54) has been on a 70-year downward trend, while that of prime-aged females has flatlined for three decades. This is a poor performance by the standards of most high-income economies. It is impossible to argue credibly that this is the result of particularly generous US welfare benefits or particularly high minimum wages.

The failure is deeper.

Third, growth of labour productivity has slowed sharply, though it was still higher than in other members of the Group of Seven leading high-income countries between 2005 and 2015.

The reasons for this slowdown are a puzzle. Possibilities include the post-crisis weakening of business investment and a broader post-crisis loss of animal spirits. It is also likely that the underlying rate of innovation is slowing. Some argue that this is the result of excessive regulation.

The next administration is set to test that hypothesis to destruction.

Finally, the US has a key role to play in tackling the threat of unmitigated climate change. In the absence of any consensus on this question in the US, Mr Obama relied on executive actions, which will now presumably be reversed.

In all, the administration rescued the US economy and bequeathed a sound foundation for its successor to build on. But it made a big mistake: it did not go all out to punish those whose malfeasance and irresponsibility blew up the financial system and economy. This sense of injustice is one reason why the US has elected the wrecking crew that is about to take office. Mr Obama could not channel rage.

Mr Trump, alas, can.

0 comments:

Publicar un comentario