ECB bond buying slide raises taper questions

Investors puzzled after central bank bought just €4bn in corporate debt in December

by: Thomas Hale

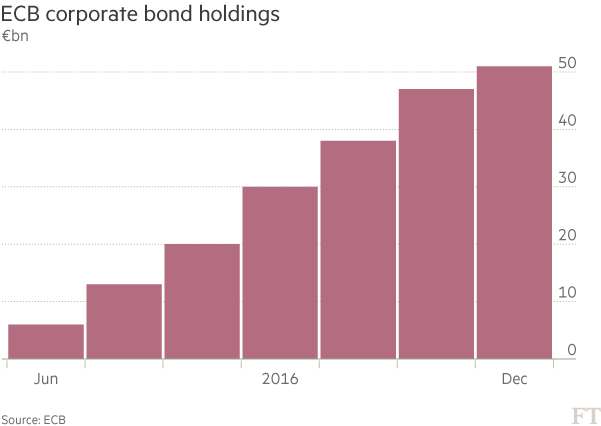

In December, the European Central Bank bought just €4bn of corporate bonds, the lowest amount in any month since its purchases began last summer.

The depressed levels of buying were clearly linked to a Christmas hiatus, but they also prompted speculation over how the scale of future purchases might play out.

The central bank has indicated it will reduce its overall purchases, across all asset classes, from €80bn to €60bn at the end of March, though its buying will continue until the end of 2017.

For investors already grappling with the prospect of rising inflation and political uncertainty, one of the most pressing questions is how a tapering process might play out specifically for European corporate bonds. The ECB has been buying corporate credit since June last year as part of a broader attempt to stimulate the continent’s economy.

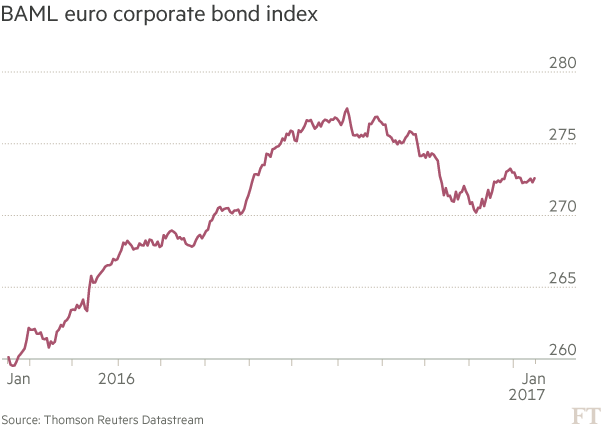

“In terms of pricing, there’s no question [the extension of bond buying to corporate paper] has had a material positive impact,” says Adam Bothamley, global head of debt syndicate at HSBC.

The ECB has bought €54bn of corporate bonds so far, according to the latest data, as part of over €1.5tn of ECB asset holdings in total.

The size of the potential fall in corporate purchases, as part of an overall reduction in buying, is a puzzle for markets. Analysts at JPMorgan this month suggested the low purchases in December “fell by more than would be expected from seasonality alone”, though they added it was likely to reflect a relative decline in credit markets over the festive season.

The ECB’s reduction in overall purchases comes in a context in which markets have complained of a scarcity of high quality assets. Minutes from last month’s ECB meeting showed that the decision to trim bond purchases came partly because of concerns over the amount of assets available to buy.

In December, the central bank initiated a programme to lend out government bonds, which followed concerns from Europe’s repo markets that there was a shortage of collateral to back short-term loans.

As such, many market participants believe sovereign bonds could be downsized more rapidly than other sectors.

“We put the bulk of reduction in asset purchases in government bonds,” says Michel Martinez, the chief euro economist at Société Générale. The bank’s main scenario is the ECB will announce a €10bn reduction in asset purchases in June.

Zoso Davies, a credit strategist at Barclays, agrees that the point on scarcity is “very specific to government bond markets”. He argues that data from the month ahead will provide clues as to the future trajectory of ECB corporate tapering, and that in March monthly corporate bond purchases will go from €8bn to €6bn a month.

“The January numbers are going to be important to give us a view on what the asset purchase split is — any deviation from that will be very interesting,” he says.

The debate around ECB bond purchases has come at a pivotal moment for European markets. This week, Larry Fink, chief executive of BlackRock, pointed to a series of flaws in Europe’s bond markets, which have struggled to catch up to the US.

The ECB’s purchases, aside from their positive effect on pricing, have been seen by some as a factor that helps unify the continent’s markets.

“They have accelerated a trend that was already in place which is a maturation of the euro market, a greater depth of the euro market,” says Mr Bothamley.

“A lot of issuers who come to the euro markets do access maturities that are not as readily available in the US, such as 7 years or 15 years,” he adds, pointing out that in some areas there is more innovation and flexibility in Europe than across the Atlantic.

Tapering in corporate bond buying could therefore have an unintended impact on broader trends in the evolution of Europe’s capital markets, especially when placed in the context of the impact of Brexit on European financial services.

Whatever the ECB decides to do when it comes to reducing bond purchases, there is little question that their decisions stand to have a significant impact on pricing.

Even though spreads have underperformed relative to US credit, and rising inflation has provoked concern among investors, bonds are still trading at elevated prices. When news broke last week of emissions allegations directed at Fiat Chrysler, the company’s euro-denominated senior bonds fell several percentage points, but were still trading significantly above par.

The sheer amount of focus on ECB decisions highlights the extent to which pricing in European credit markets has become heavily dependent on the actions of one central authority. This has created an environment in which the most unnerving risks are linked to the very policies that were introduced to provide stability.

“It is undeniable that there is a chance they maintain it — there is even a tail risk that the corporate bond purchase programme is upsized,” says Mr Davies.

“I genuinely think that’s an extremely unlikely outcome,” he adds, “but we can’t discount anything, given the world we live in.”

0 comments:

Publicar un comentario