Beware The Next Correction

by: Eric Parnell, CFA

Summary

- Beware the next correction in the U.S. stock market.

- The "buy the dips" strategy that has served investors so well during the post-crisis period may not continue into the future.

- Consider whether the catalysts that sparked the post-correction rallies in the past are still in place in the future.

- The "buy the dips" strategy that has served investors so well during the post-crisis period may not continue into the future.

- Consider whether the catalysts that sparked the post-correction rallies in the past are still in place in the future.

Beware the next correction in the U.S. stock market. Investors have been conditioned to a certain way of thinking during the post-crisis period. Despite any perceived underlying causes, any measurable pullbacks in the stock market are fleeting and are quickly followed by swift and powerful rallies.

Thus, these pullbacks are viewed as attractive short-term buying opportunities. All of this may continue to be true as we continue through 2017 and beyond. This includes, as some have recently been speculating in the days ahead, any potential "Trump dump" in the wake of the "Trump rally."

But before moving to repeat this "buy the dip" trade yet again in the future, it is important to consider whether the forces that have enabled these sharp reversals are still in place or whether new conditions may now be at work that may lead to potential frustration instead.

A Rewarded Strategy

Moving aggressively to buy measurable stock market pullbacks has been a strategy that has gone highly rewarded in recent years.

For an extended stretch from 2012 to 2014, the stock market was impervious to any meaningful corrections at all. Sure, there was the post-election pullback in 2012, the so-called "taper tantrum" in May-June 2013 and the handful of days after Russia (NYSEARCA:RSX) invaded Crimea in early 2014, but all of these corrections were relatively short and none exceeded -10% on the S&P 500 Index (NYSEARCA:SPY). Of course, throughout this entire time period the U.S. Federal Reserve was either gearing up to or actively implementing its QE3 stimulus program, which was the most aggressive in terms of the size and duration of its asset purchases.

It was not until the very end of its QE3 program in late 2014 when we finally saw the U.S. stock market return to showing any sort of reflex to the downside. And since that time, we have seen four distinct pullbacks that have been notable for review in this context.

The Fleeting Foursome

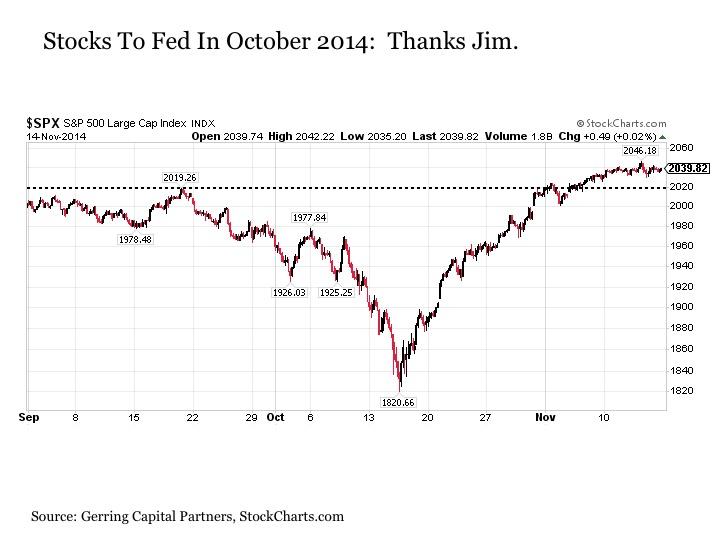

The first of these four recent corrections took place during September-October 2014. The U.S. Federal Reserve was in the process of winding down to the end of its QE3 stimulus program at a time when economic growth prospects remained lackluster and the global energy market was in the early stages of unwinding. And during a less than four-week period from late-September to mid-October, stocks moved increasingly to the downside for a total correction of roughly -10%. In the process, the S&P 500 Index broke below its 200-day moving average at the time for the first time in roughly two years.

But everything suddenly changed one October trading day. For once St. Louis Fed President James Bullard took to the microphone and hinted at the fact that the U.S. Federal Reserve might delay ending its QE3 stimulus program, stocks were back off to the races to the upside.

By the end of the month, stocks had already recovered all of their losses and were soon on to fresh new highs. In short, buying this dip was handsomely rewarded.

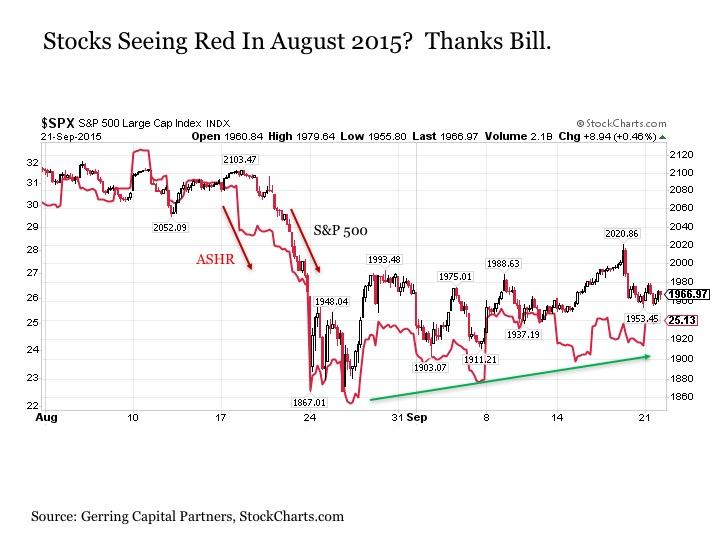

The second pullback took place in August 2015. During that time, the U.S. stock market was holding its own not far from all-time highs when it suddenly began cascading to the downside.

Of course, it was around this same exact time that policy makers in China had taken action to prick the stock market bubble that had formed over the past year into the summer of 2015.

Over the course of just five days, the S&P 500 Index dropped by -12% and gave investors a jarring flash crash along the way.

But after these swift losses, the markets just as quickly bottomed and started to mend. And by the end of the month, stocks had recovered roughly half of their lost value. What helped soothe investor nerves? Up until that point, the market had been expecting that the Fed would be carrying out its second interest rate hike in September. But after a few days of stock market declines, William Dudley, the president of the Federal Reserve Bank of New York, declared that the case for a September interest rate hike had become less compelling. And from the moment these reassuring words were uttered, stocks were headed back to the upside and continued to push forward with fits and starts through mid-September.

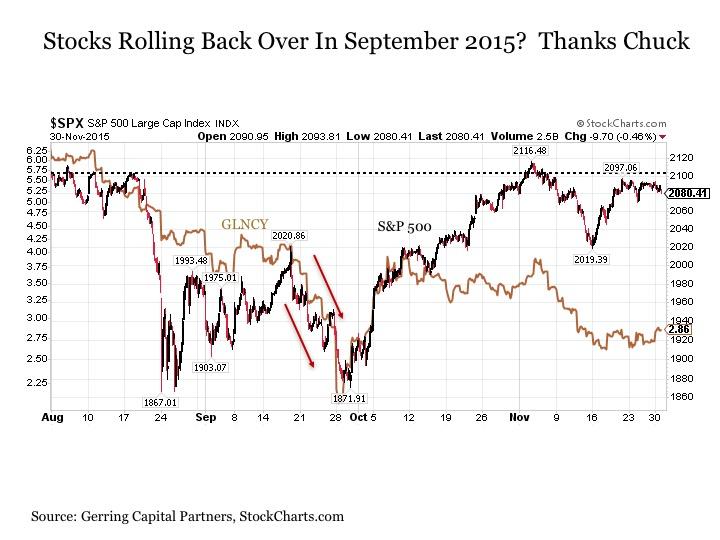

Unfortunately, stocks were not quite out of the woods yet this time around. By mid-September, the People's Bank of China was continuing to withdraw liquidity from the market at the same time that the commodities market was beginning to seize. At the center of the issue at the time was Glencore (OTCPK:GLNCY), the major commodities trader with measurable counterparty risk whose shares were plunging to the downside as the firm was actively engaged in fighting for its survival under difficult market conditions. As a result, stocks were back falling -8% to the downside.

But once again, a group of Fed members were dispatched to deliver reassuring messages of monetary policy patience to the market. Some such as Chicago Fed President Charles Evans declared that the Fed should delay further and wait until 2016 to raise interest rates. Others such as St. Louis Fed President James Bullard cast doubt on the urgency for the Fed to raise interest rates while those still striking more hawkish tones like William Dudley issued these statements with the caveat of data dependency focused on data like inflation that was still below the Fed's target. Thanks once again to the parade of Fed officials emerging from their respective phone booths to save the day at the end of September, stocks were once again off to the upside. And after a tremendous October 2015, stocks had recovered all of the losses first inflicted just two months earlier in August. Once again, investors showing the courage to buy the dips were rewarded.

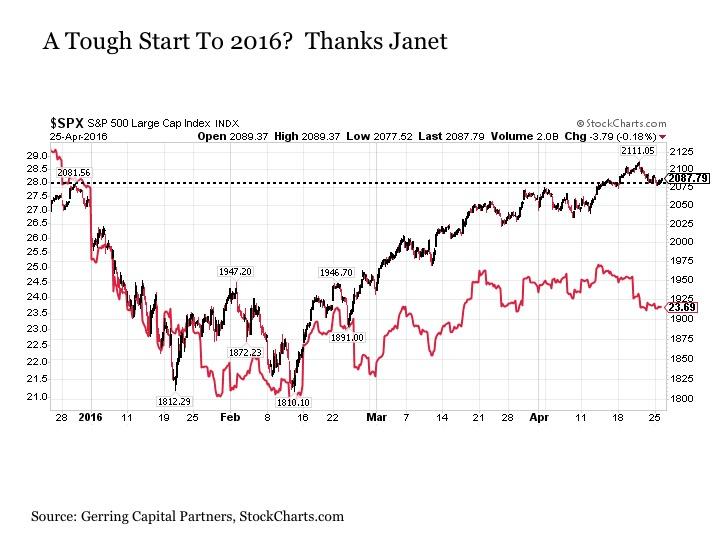

The fourth and final correction during the post QE3 period came with the flipping of the calendar to 2016. At the time, the People's Bank of China was completing the measurable contraction of its balance sheet and the Chinese stock market was undergoing its final unwind from its short but epic bubble that had burst just a few months earlier. In the process, stocks lost -13% of their value in just three short weeks into January and revisited these lows a few weeks later in February.

But starting in late January and continuing into early February, the Federal Reserve led by Janet Yellen that had declared just a few weeks earlier its intention to raise interest rates as many as four times in 2016 was issuing repeatedly reassuring tones that the Fed was backing off from this anticipated rate hike pace. Once the China stock market unwind had run its course and the market was sufficiently pacified that the Fed would not be acting on rates any time soon, it was off to the races one more time to the upside. By mid-April, stocks had once again quickly recovered all of its correction losses and the "buy the dip" traders were rewarded once again.

We have had four notable corrections over the past two plus years since the end of the Fed's last QE3 stimulus program. And in each case, it was the vocal intervention of the U.S. Federal Reserve that saved the day and rewarded those intrepid investors who had the courage to step in and buy when the market was quickly spiraling to the downside.

Will The Fed Continue To Save The Day?

It has been roughly a year now since we have seen the last measurable correction in the U.S. stock market. Sure we have seen a few soft pullbacks along the way, but these have either been lightning fast (post-Brexit) or have seemed more like consolidation (mid-August to early-November) than anything of note.

But a lot has changed both at the Fed and across Washington in the past year. A LOT. Put simply, the political cage has been rattled both in the U.S. and around the world by the dramatic shift toward more populist and nationalist policies as voters increasingly express their frustration over political elites that have acted in the view of many to serve only themselves and the ultra wealth at the expense of the masses. And the actions of the Federal Reserve were brought directly into the crosshairs during the debates that have taken place so far during this ongoing transformation.

As a result, interventionist actions to support the stock market by the U.S. Federal Reserve that might have been viewed as acceptable if not lauded this time a year ago are now being viewed with increasing cynicism and met with growing outside pressure given the ongoing negative consequences of these actions on the responsible savers for the benefit of the profligate risk takers.

At the same time, the policy priorities of the soon-to-be new President of the United States may usher in an entirely new policy perspective at the Fed. To begin with, the team that is advising the president-elect on monetary policy has an extensive public record of being more hawkish and openly critical of the Fed and its policies during the post-crisis period. Moreover, we may see the complexion of the still relatively dovish Federal Reserve meaningfully transformed once the new administration is in office. This is due to the fact that two of the seven Board Governor seats are currently vacant and ready to be filled and a third position may soon become available if current Board Governor Daniel Tarullo departs as some have speculated. As for the two top spots among the Board of Governors in current Chair Janet Yellen and Vice Chair Stanley Fischer, their terms are set to expire in February 2018 and June 2018, respectively.

Why does all of this matter to the "buy the dip" crowd? Because the next time we see a measurable stock correction, the potentially more hawkish leadership at the U.S. Federal Reserve may not be so quick to rush out and reassure the markets the next time it is falling by -10% or more over the course of a handful of days or weeks. As a matter of fact, they may not have anything to say at all depending on who is ultimately part of the team or leading the group. And given that vocal and reassuring intervention by the U.S. Federal Reserve has been the primary catalyst for rewarding not only "buy the dip" traders for stepping in but also longer-term investors for staying the course, risks are rising that this catalyst may be delayed or completely missing the next time the stock market starts moving steadily if not sharply to the downside.

So What Can We Reasonably Expect Going Forward?

The stock market will eventually correct once again. It will even fall into a new bear market at some point in the future, but this is a conversation for a later date. The question is exactly when will any such correction take place? Given that the stock market rallied so swiftly in the five weeks after Election Day based on expectations about fiscal policy changes that may ultimately prove wildly optimistic in terms of when these anticipated changes actually take place (if they end up changing at all), some have speculated that such a correction might get underway not after Inauguration Day at the end of next week. Whether such predictions prove prescient or not remains to be seen.

But if such a correction were to take place sooner rather than later, it should be noted that the old sheriff in relatively dovish Janet Yellen is still in charge. And given that the market is currently anticipating between two to three rate hikes in 2017, she has the flexibility to talk these expectations down just as she did in 2016. Not only would such an outcome likely spark another "buy the dips" rally in stocks (NYSEARCA:DIA), but it would also put an upside tailwind into a bond market (NYSEARCA:BND) that struggled at the end of 2016 supposedly due to concerns about the Fed raising rates in 2017 (I would contend it had much more to do with the mass liquidation of Treasuries by a Chinese government trying to offset major capital outflows from the country, but even if this is the case, a Fed dialing back rate hike expectations is short-term to intermediate-term bullish for the bond market (NYSEARCA:AGG)). Such a shift would also likely favor defensive stocks such as consumer staples (NYSEARCA:XLP) and utilities (NYSEARCA:XLU) over cyclicals such as industrials (NYSEARCA:XLI) in the short term to intermediate term as well as the gold (NYSEARCA:GLD) market.

Looking further ahead, the longer we continue into the future and the more the Federal Reserve becomes transformed, the less investors should be complacent in thinking that the next correction in stocks will be fleeting and should be bought. For if the Fed does become notably more hawkish as expected, it may increasingly be led by those who not only believe that managing the daily swings of the stock market should not be a concern of monetary policy, but may also think that taking some of the froth out of a stock market that is currently at historically high valuations in the midst of the second longest bull market in history despite an otherwise lousy economy throughout the post-crisis period might actually be a good and healthy thing.

The Bottom Line

During the post-crisis period, stock market corrections have proven fleeting and provided investors with outstanding buying opportunities. But such "buy the dips" success may not continue into the future. For the primary catalyst for these rallies was the active vocal intervention by a U.S. Federal Reserve that placed propping up the stock market as a key policy priority. And while this stock market supportive group remains in charge of the Fed for now, it is likely that a new more hawkish group of policy makers will be increasingly taking control over the coming year that may care little for supporting the stock market any further than the Fed already has in recent years.

As a result, beware the next correction in stock prices. Don't necessarily jump right in after stocks have fallen anywhere between -7% and -13% thinking that a snap-back rally is right around the corner. Instead, first consider the complexion of the U.S. Federal Reserve at the time when any such stock correction is unfolding. For depending on either who is in charge or is vocally in the ear of who is in charge may go a long way in determining how assertively the Fed will be back if at all to save the day for stocks the next time stocks are plunging to the downside.

In short, still look to "buy the dips," but be more careful when doing it going forward given the new leadership coming to town at the U.S. Federal Reserve.

0 comments:

Publicar un comentario