Anatomy Of A Bubble

by: The Heisenberg

Summary

- It's déjà vu all over again for those of us who remember the bursting of China's margin-fueled equity bubble.

- The amount of leverage embedded in China's bond market is likely far greater than even the most pessimistic of analysts project.

- Last month was but a preview of what's to come.

- The amount of leverage embedded in China's bond market is likely far greater than even the most pessimistic of analysts project.

- Last month was but a preview of what's to come.

I remember the summer of 2015 like it was yesterday.

Greece was on the verge of becoming a failed state. Then finance minister Yanis Varoufakis had become something of a celebrity. To be sure, he relished his renegade image, riding a motorcycle to work and playing spoiler to Berlin's attempts to squeeze concessions from Athens in exchange for the ECB's willingness to increase the amount of emergency liquidity assistance available to Greece via what amounted to a revolver.

At the same time, China's margin debt-fueled equity "miracle" was imploding. During the spring, I watched incredulous as housewives, security guards, and all manner of other everyday Chinese morphed into day traders seemingly overnight. "The rally may last for a few more days," one such newly-minted market maven told Bloomberg in April of 2015. "I'm just taking a lunch break to do some trading because the market is hot," he added.

In the final week of May 2015, Chinese investors created nearly 2 million new trading accounts according to data (which is no longer available) from the China Securities Depository and Clearing Co. That was up nearly 50% from the previous week.

Many of those investors found that leveraging their accounts was easy. For those who may have forgotten, here's a classic chart from BNP which gives you an idea of just how surreal the situation had become by the end of March:

(Chart: BNP)

(Chart: BNP)

Needless to say, much of this leverage was made available via backdoor channels. There were several safeguards in place to make sure things didn't get out of hand. For instance, only investors with at least CNY500,000 in their accounts could trade on margin and those investors were only allowed to lever up two times. Brokerages, not wanting to turn away business, resorted to exotic vehicles like the now infamous "umbrella trust" to get around the rules.

Ultimately, Beijing ended up having to create a massive rescue vehicle for the market which went into freefall in June of 2015. China then embarked on a truly epic witch-hunt. Those deemed "responsible" for the debacle were tracked down, questioned, detained, and worse.

Journalists were jailed, officials "disappeared" - you know, just the usual stuff you'd expect from the Politburo.

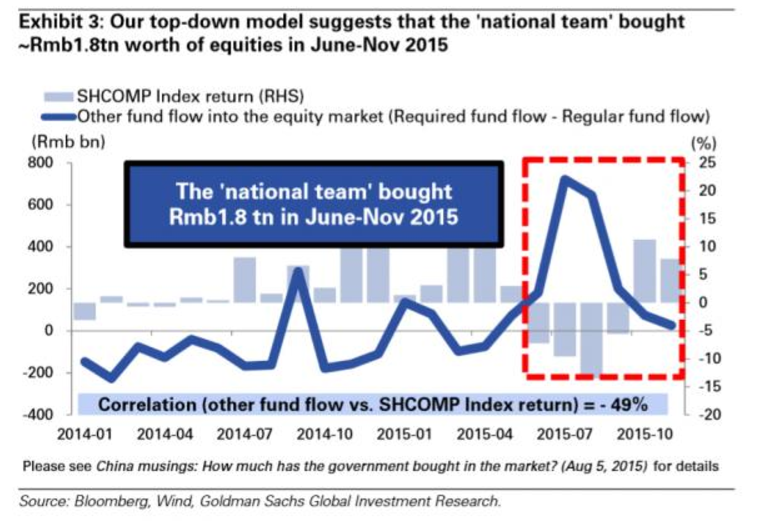

By the time the smoke cleared, Beijing ended up buying some CNY1.8 trillion in stocks in order to stabilize the market:

(Chart: Goldman)

(Chart: Goldman)

I retell that story now because the very same thing is about to happen in China's bond market.

On Friday, I brought you the latest numbers on the amount of leverage in the system. Just as the "official" numbers on margin debt grossly understated the amount of leverage investors were employing to buy stocks in 2015, so too do the headline numbers on leverage ratios in the Chinese bond market paint a completely inaccurate picture of just how levered up market participants truly are.

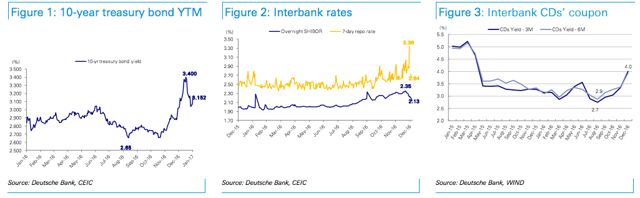

"Bond leverage via regulated repo transactions are relatively low," Goldman said in a note out Friday. "We estimate that as of the end of 2016, leverage in the interbank bond market was around 1.1x (Exhibit 1) and leverage in the exchange traded bond market was around 1.4x (Exhibit 2)."

(Charts: Goldman)

(Charts: Goldman)

But while only CNY4 trillion in repo (a proxy) was outstanding at the end of 2016, Caixin estimates that entrusted bond agreements may total as much as CNY12 trillion. Needless to say, if true that would meaningfully increase the leverage ratio.

For those who, like me, are anxious for more color, Deutsche Bank is out with an exhaustive study of the Chinese banking sector and one of the very first issues they tackle is entrusted bond deals and their likely impact on the market.

Of course all of this starts with the PBoC's effort to contain financial risks (risks like too much leverage in the bond market). Essentially, Beijing has purposefully engineered higher short-term funding costs with the aim of reducing market participants' incentive to take risks. I suggest you go back through my previous pieces both here and elsewhere for a detailed breakdown of the steps the central bank has taken (e.g. extending the tenor of liquidity ops).

For now, consider Deutsche Bank's summary (my highlights):

China's rates in the interbank and bond markets have been rising since August 2016.

We believe the liquidity tightness was engineered purposely by the PBOC, which aims to delever the bond and shadow banking markets. In the bond market, speculators (mainly NBFIs, smaller banks and entrusted banks' WMPs) were borrowing short-term interbank liabilities to leverage up and to chase yield.

{kind=link}

To contain the risks in these two markets, PBOC has lengthened the duration of liquidity injection and increased direct lending to smaller banks. This has pushed up interbank rates and increased the funding costs for speculators in the bond and shadow banking markets. With a narrower spread (even negative ones in some cases), these speculators were forced to delever in both markets. This is why we witnessed a notable bond market correction in December 2016.

Got that? Essentially, Beijing is looking to eliminate the spread between what speculators were paying to borrow and the yield they could get on their investments.

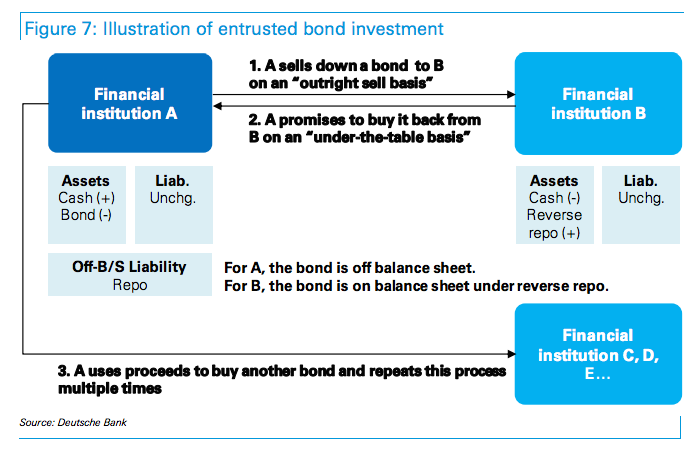

Deutsche Bank goes on to outline just how the entrusted bond deals work (note that this is a far better explanation than the bullet point summary I linked to in Friday's piece):

- First, financial institution A sells a bond to financial institution B on an "outright sell basis".

- Secondly, A promises to repurchase the bond from B at a certain point on an "under-the-table basis".

- From A's point of view, the bond is off balance sheet as A sells down the bond to B, even though this is effectively a repurchase transaction. From B's point of view, the bond is on balance sheet and normally booked under reverse repo or other investment categories.

- Third, A uses the proceeds from selling the bond to buy another bond. A can repeat this process multiple times by dealing with other counterparties to leverage up.

(Chart, bullet points: Deutsche Bank)

(Chart, bullet points: Deutsche Bank)

Note the bolded passage in the last bullet. Essentially, A takes the proceeds from the repo agreement and uses them to buy another bond which is then pledged in an identical deal to still another counterparty. Here's Deutsche Bank again:

The main incentive is to leverage up and to chase yield. Let us assume the bond yields 4%. The funding cost for A to conduct the repo transaction with B is normally interbank short-term rates plus 50bps, i.e., around 3%. As such, in this transaction A could earn c.100bps (i.e., bond yield of 4% minus funding cost of 3%) without consuming any capital or breaching any regulation on leverage, as the bond is off balance sheet. A can repeat the process again to leverage up further and gain a higher return. For example, repeating this process three times makes 7% for A. In the meantime, B earns about 50bps as a commission above the short-term interbank rate.

That's how a massive amount of leverage has ended up embedded in China's bond market.

Note also that this is precisely the type of structure that got Sealand Securities into trouble in December. Essentially, Sealand (which was levered of course) didn't want to honor its end of the agreement and so the firm (rightly or wrongly) claimed that a rogue trader had forged the company seal on the documents tied to the deal.

You can see now why I contend that if we were to get an even steeper bond rout, heightened concerns about counterparty integrity would reverberate through the multiple layers of leverage embedded in the market.

This is a veritable house of cards and no one knows how large it is. There's no telling how levered up some of these brokerages are. Once the entrusted deal is done, the bond is no longer held on the seller's books. Neither are the bonds the brokerage buys with the deal proceeds because those bonds are promptly pledged to yet another counterparty. And so on, and so forth as the leverage pyramid grows.

For those of us whose job it was to cover the collapse of China's equity markets in 2015, this is déjà vu all over again. The only difference is, this time around the PBoC is actually helping to facilitate the unwind as opposed to spending trillions to forestall it.

That may ultimately make the implosion that much more spectacular.

0 comments:

Publicar un comentario