US corporate bonds: The weight of debt

Expansion plans are in question after a focus on dividends and share buybacks

by: Michael Mackenzie and Eric Platt

There was no shortage of buyers when Microsoft sold $20bn in bonds this summer to fund its acquisition of LinkedIn. After years of low interest rates — and with rates in some countries heading into negative territory — debt issued by US companies such as Microsoft looked very attractive compared with the meagre returns offered by government bonds.

But after Donald Trump’s pledge to push for an aggressive fiscal stimulus of the US economy, these blockbuster corporate debt sales suddenly look like hallmarks of a very different market environment. As investors and markets try to anticipate what a Trump presidency will mean, one early conclusion is that a dose of fiscal shock treatment will result in much higher interest rates and accelerating inflation.

Markets have moved with remarkable speed to price in these outcomes, with about $2.1tn wiped off global bond prices since the election.

A sharp upward movement in rates would be bad news for the investors who have piled into debt that pays a very low fixed rate of return. Rising inflation and falling bond prices stand to hammer the value of their portfolios.

A troubling question also confronts US companies, which have been on a stunning debt binge in recent years. How will they finance their expansion to capitalise on the stronger economy that Mr Trump’s proposed fiscal splurge will aim to unleash?

“How much fiscal stimulus can you get through with [corporate] debt burdens where they are?” asks Bob Michele, JPMorgan Asset Management’s global head of fixed income.

“Companies have been so used to issuing [debt] with the 10-year yield at 2 per cent it’s going to be a bit of a shock.”

© FT Gaphic / Dreamstime, Getty

© FT Gaphic / Dreamstime, Getty

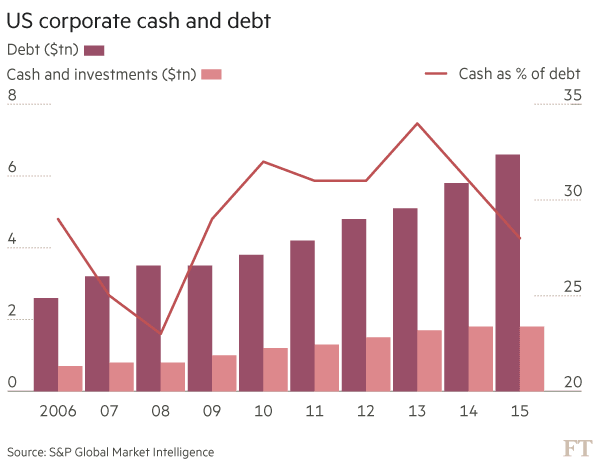

Over the past decade corporate debt in the US has risen by three-quarters to $8.4tn, according to the Securities Industry and Financial Markets Association. Money market obligations, which include short-term company borrowings, lift that figure to $11.3tn. Only the market for US Treasuries has climbed at a faster pace.

The legacy of this debt has stretched corporate balance sheets for all but the top echelon of S&P 500 companies with large cash holdings.

Much of the debt sold by companies in recent years has been used to buy back their own shares, pay out higher dividends or finance big mergers and acquisitions. While these buybacks funded by cheap borrowing have boosted earnings, a missing ingredient has been spending on investment to build their businesses. Now with Mr Trump and a Republican-controlled Congress looking to ignite the US economy, companies will need to finance business investment, adding to an already hefty amount of debt in a market of rising borrowing costs.

Didier Saint-Georges, managing director of fund manager Carmignac, says a higher potential US growth rate requires a much stronger investment cycle from companies. The problem he sees is that the bond market, which has seen a punishing sell-off since the election, is anticipating an outcome that could take 12 to 18 months to register.

“In the meantime the cost of capital is going up,” he says. “And we need private investment to pick up.’’

The US Federal Reserve is expected to raise rates at its meeting next week. With Steven Mnuchin, Mr Trump’s pick for Treasury secretary, talking about accelerating US growth in gross domestic product to 3 or 4 per cent a year, bond markets are concerned about the pace of rate rises in 2017 and beyond.

Easy credit

Central bank policymakers have been “encouraging” the boom in debt issuance, says Dan Ivascyn, Pimco’s chief investment officer, including by the outright bond-buying programmes under way by the European Central Bank, Bank of England and Bank of Japan that have pushed rates ever lower.

Despite the risk debt carries, this encouragement from central banks has helped to make companies more comfortable with it than ever before, says Diane Vazza, the head of global fixed income research at Standard & Poor’s. “Credit has been easy and access to capital markets has been unfettered to even the lowest quality issuers,” she adds.

Steven Mnuchin, Donald Trump's pick for Treasury secretary, wants to boost economic growth © FT Graphic / Dreamstime, Reuters

Steven Mnuchin, Donald Trump's pick for Treasury secretary, wants to boost economic growth © FT Graphic / Dreamstime, Reuters

Top-rated US companies have amassed 2.4 times net debt compared with their earnings before interest, taxes, depreciation and amortisation — a scrutinised investor metric. This is the highest level since 2002 and the fourth consecutive quarter it has increased, says Bank of America.

“Leverage, if not at all-time highs, is close,” says Monica Erickson, a portfolio manager with DoubleLine Capital.

Credit ratings have been dragged lower by the boom in debt issuance. Two decades ago, more than 66 per cent of the companies rated by S&P held an investment grade rating; today it is 45 per cent. The percentage of groups with an A or higher rating has roughly halved over that period. Now only two US companies — Microsoft and Johnson & Johnson — carry the highest triple-A opinion.

Unless companies are confident in economic growth and have projects to invest in, they are likely to continue to use their cash to buy back stock and issue dividends, Ms Erickson says.

While popular with shareholders, buybacks and dividends did not leave companies with ready cash to invest in their business when conditions improved.

“Issuing a bond and dividending it out to equity holders isn’t creating the same type of investment and structural reform and improvement across corporate America,” Mr Ivascyn says. “It is less ideal.”

Others warn that the high levels of outstanding corporate debt loom as a limit on the ability of the US economy to fund a deficit-driven expansion. A surge in Treasury debt to fund infrastructure projects, a key promise of Mr Trump’s, would push up interest rates and possibly limit the ability of companies to sell debt in the right quantities and at the right prices.

In 2000 and then 2007, booming credit and elevated equity markets were followed by major busts that rippled far across the financial system. The recent rise in debt levels has prompted uncomfortable comparisons.

“We are back to levels we saw in 2000, but the big difference is we reached those levels right at the brink of the recession,” says Scott Minerd, Guggenheim Investments’ global chief investment officer.

“The [next] recession is another two to three years away, so given this kind of debt load it starts to remind me of subprime borrowing in 2005. We are nowhere near this ending. We’re just piling more and more debt on the corporate sector.”

Regulators have been voicing their concerns over the rising debt bubble and the risk it poses to financial markets. They are becoming louder, with Fed officials discussing this at their September policy gathering. That followed a warning over credit risks this summer from the Office of Financial Research’s latest report on risks to US financial stability. “Caution is warranted,” Mr Ivascyn says.

“There is a lot of debt in the world and nominal growth is low.”

For now, high cash levels held by US companies, which are tilted heavily towards the big tech groups, and a low forecast for debt defaults in the coming years suggests concern about leverage is misplaced.

The resurgence of equity indices, including the small-cap Russell 2000, which has set a string of records, could also prove a bulwark against the excessive debt if the market for initial public offerings rebounds in tow. IPOs could help pay down rising debt burdens.

Much depends on whether the proposed fiscal stimulus measures under Mr Trump will bolster earnings for companies next year and offset a rising interest rate environment.

Andrew Milligan, head of global strategy at Standard Life Investments, says there needs to be an improvement in the bottom line “to support valuations and the large debt build-up by companies”.

A tax holiday that prompts repatriation of cash held overseas by global US companies, a move investors expect during the Trump administration, could help boost investment. Mr Milligan says it is unclear whether companies will plough any repatriated profits into capital investment or simply boost buybacks.

“Repatriation could flow through fairly quickly and lead to a noticeable rise in share buybacks.”

Moreover, some argue that blue-chip companies that have locked in ultra low borrowing rates — and in some cases are selling bonds with a negative coupon — will find no problem repaying the debt.

Beyond the top echelon of US companies, cash balances are more diffuse. S&P data show that a record stash of $1.84tn in cash and investments held by non-financial companies masks a $6.6tn debt burden.

The cash is concentrated primarily within 25 groups, including Apple, Microsoft and Google-owner Alphabet. In the past year, the debt level has surged by roughly $850bn, while cash climbed a paltry $17bn.

A strengthening dollar, propelled by the budding view that the Federal Reserve may have to tighten policy more rapidly to tame inflation, could also depress foreign based earnings for US companies at a time when leverage is already above average.

‘Credit ends badly’

Andrew Lapthorne, head of quantitative analysis at Société Générale, says debt sold by publicly listed companies relative to their assets has surpassed the height seen during the technology, media and telecom bubble of 2000.

One crucial difference from past bond market booms is that companies do not face a looming maturity wall, when the bulk of their obligations come due. As commercial paper markets contracted earlier this year, companies began issuing bonds that mature in 20, 30 and 40 years.

The average maturity of investment grade debt has also lengthened, rising from a low of 12 years in 2009 to 17 years by the end of 2015, according to data at Sifma, the US trade group.

That has exposed investors to interest rate shocks, as bond prices rise and fall alongside the move in benchmark sovereign debt. The price sensitivity of long maturity bonds to the direction of interest rates has exacerbated losses within that debt. Prices of US corporate bonds maturing in more than 25 years have declined 5.7 per cent in November. Debt maturing within three and five years slipped 1.4 per cent by contrast.

In an environment of rising yields, prices for 10- and 30-year bonds fall the most and can quickly wipe out interest income earned from holding the paper.

Microsoft’s 30-year bond sold in August fell to 92.30 cents on the dollar last week, down 4.4 per cent since the presidential election. Bonds issued by Apple maturing in 2046 traded on Friday at 92.7 cents on the dollar, down from par as recently as October.

Richard Madigan, chief investment officer at JPMorgan Private Bank, says investors have crowded into corporate bonds and that “credit always ends badly”. Given the rise in overall borrowing by companies, he adds: “Balance sheets are fully loaded.”

Mr Madigan says a bite-back in credit will be intensified by the relative illiquidity of corporate bonds in the secondary market. “The problem with credit is that it takes time to change and it can be very disruptive.”

Although default models look at credit on the basis of whether a company will ultimately pay back the principal owed on debt at maturity — say 10 or 30 years — markets are far more demanding and their opinion can swiftly change, argues Mr Lapthorne.

“The way credit markets work is that we continually ask about the value of a company’s assets. Investors are in effect always asking, can this company repay its principal today, even though the repayment is not actually due for 30 years?’’

With the bond markets in the midst of a brutal post-election sell-off, investors are set to keep asking these questions.

Markets have moved with remarkable speed to price in these outcomes, with about $2.1tn wiped off global bond prices since the election.

A sharp upward movement in rates would be bad news for the investors who have piled into debt that pays a very low fixed rate of return. Rising inflation and falling bond prices stand to hammer the value of their portfolios.

A troubling question also confronts US companies, which have been on a stunning debt binge in recent years. How will they finance their expansion to capitalise on the stronger economy that Mr Trump’s proposed fiscal splurge will aim to unleash?

“How much fiscal stimulus can you get through with [corporate] debt burdens where they are?” asks Bob Michele, JPMorgan Asset Management’s global head of fixed income.

“Companies have been so used to issuing [debt] with the 10-year yield at 2 per cent it’s going to be a bit of a shock.”

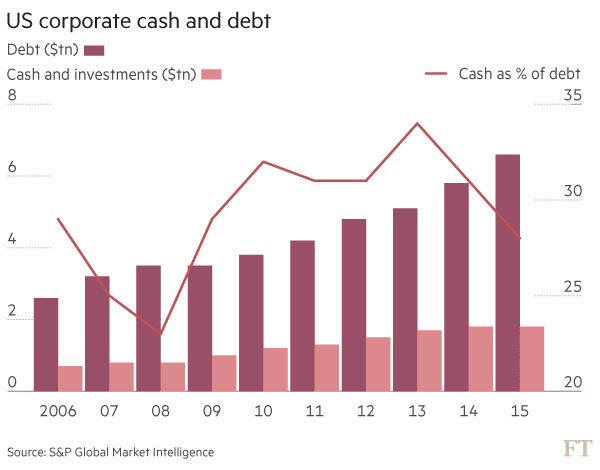

© FT Gaphic / Dreamstime, GettyOver the past decade corporate debt in the US has risen by three-quarters to $8.4tn, according to the Securities Industry and Financial Markets Association. Money market obligations, which include short-term company borrowings, lift that figure to $11.3tn. Only the market for US Treasuries has climbed at a faster pace.

The legacy of this debt has stretched corporate balance sheets for all but the top echelon of S&P 500 companies with large cash holdings.

Much of the debt sold by companies in recent years has been used to buy back their own shares, pay out higher dividends or finance big mergers and acquisitions. While these buybacks funded by cheap borrowing have boosted earnings, a missing ingredient has been spending on investment to build their businesses. Now with Mr Trump and a Republican-controlled Congress looking to ignite the US economy, companies will need to finance business investment, adding to an already hefty amount of debt in a market of rising borrowing costs.

Didier Saint-Georges, managing director of fund manager Carmignac, says a higher potential US growth rate requires a much stronger investment cycle from companies. The problem he sees is that the bond market, which has seen a punishing sell-off since the election, is anticipating an outcome that could take 12 to 18 months to register.

“In the meantime the cost of capital is going up,” he says. “And we need private investment to pick up.’’

The US Federal Reserve is expected to raise rates at its meeting next week. With Steven Mnuchin, Mr Trump’s pick for Treasury secretary, talking about accelerating US growth in gross domestic product to 3 or 4 per cent a year, bond markets are concerned about the pace of rate rises in 2017 and beyond.

Easy credit

Central bank policymakers have been “encouraging” the boom in debt issuance, says Dan Ivascyn, Pimco’s chief investment officer, including by the outright bond-buying programmes under way by the European Central Bank, Bank of England and Bank of Japan that have pushed rates ever lower.

Despite the risk debt carries, this encouragement from central banks has helped to make companies more comfortable with it than ever before, says Diane Vazza, the head of global fixed income research at Standard & Poor’s. “Credit has been easy and access to capital markets has been unfettered to even the lowest quality issuers,” she adds.

Steven Mnuchin, Donald Trump's pick for Treasury secretary, wants to boost economic growth © FT Graphic / Dreamstime, ReutersTop-rated US companies have amassed 2.4 times net debt compared with their earnings before interest, taxes, depreciation and amortisation — a scrutinised investor metric. This is the highest level since 2002 and the fourth consecutive quarter it has increased, says Bank of America.

“Leverage, if not at all-time highs, is close,” says Monica Erickson, a portfolio manager with DoubleLine Capital.

Credit ratings have been dragged lower by the boom in debt issuance. Two decades ago, more than 66 per cent of the companies rated by S&P held an investment grade rating; today it is 45 per cent. The percentage of groups with an A or higher rating has roughly halved over that period. Now only two US companies — Microsoft and Johnson & Johnson — carry the highest triple-A opinion.

Unless companies are confident in economic growth and have projects to invest in, they are likely to continue to use their cash to buy back stock and issue dividends, Ms Erickson says.

While popular with shareholders, buybacks and dividends did not leave companies with ready cash to invest in their business when conditions improved.

“Issuing a bond and dividending it out to equity holders isn’t creating the same type of investment and structural reform and improvement across corporate America,” Mr Ivascyn says. “It is less ideal.”

Others warn that the high levels of outstanding corporate debt loom as a limit on the ability of the US economy to fund a deficit-driven expansion. A surge in Treasury debt to fund infrastructure projects, a key promise of Mr Trump’s, would push up interest rates and possibly limit the ability of companies to sell debt in the right quantities and at the right prices.

In 2000 and then 2007, booming credit and elevated equity markets were followed by major busts that rippled far across the financial system. The recent rise in debt levels has prompted uncomfortable comparisons.

“We are back to levels we saw in 2000, but the big difference is we reached those levels right at the brink of the recession,” says Scott Minerd, Guggenheim Investments’ global chief investment officer.

“The [next] recession is another two to three years away, so given this kind of debt load it starts to remind me of subprime borrowing in 2005. We are nowhere near this ending. We’re just piling more and more debt on the corporate sector.”

Regulators have been voicing their concerns over the rising debt bubble and the risk it poses to financial markets. They are becoming louder, with Fed officials discussing this at their September policy gathering. That followed a warning over credit risks this summer from the Office of Financial Research’s latest report on risks to US financial stability. “Caution is warranted,” Mr Ivascyn says.

“There is a lot of debt in the world and nominal growth is low.”

For now, high cash levels held by US companies, which are tilted heavily towards the big tech groups, and a low forecast for debt defaults in the coming years suggests concern about leverage is misplaced.

The resurgence of equity indices, including the small-cap Russell 2000, which has set a string of records, could also prove a bulwark against the excessive debt if the market for initial public offerings rebounds in tow. IPOs could help pay down rising debt burdens.

Much depends on whether the proposed fiscal stimulus measures under Mr Trump will bolster earnings for companies next year and offset a rising interest rate environment.

Andrew Milligan, head of global strategy at Standard Life Investments, says there needs to be an improvement in the bottom line “to support valuations and the large debt build-up by companies”.

A tax holiday that prompts repatriation of cash held overseas by global US companies, a move investors expect during the Trump administration, could help boost investment. Mr Milligan says it is unclear whether companies will plough any repatriated profits into capital investment or simply boost buybacks.

“Repatriation could flow through fairly quickly and lead to a noticeable rise in share buybacks.”

Moreover, some argue that blue-chip companies that have locked in ultra low borrowing rates — and in some cases are selling bonds with a negative coupon — will find no problem repaying the debt.

Beyond the top echelon of US companies, cash balances are more diffuse. S&P data show that a record stash of $1.84tn in cash and investments held by non-financial companies masks a $6.6tn debt burden.

The cash is concentrated primarily within 25 groups, including Apple, Microsoft and Google-owner Alphabet. In the past year, the debt level has surged by roughly $850bn, while cash climbed a paltry $17bn.

A strengthening dollar, propelled by the budding view that the Federal Reserve may have to tighten policy more rapidly to tame inflation, could also depress foreign based earnings for US companies at a time when leverage is already above average.

‘Credit ends badly’

Andrew Lapthorne, head of quantitative analysis at Société Générale, says debt sold by publicly listed companies relative to their assets has surpassed the height seen during the technology, media and telecom bubble of 2000.

One crucial difference from past bond market booms is that companies do not face a looming maturity wall, when the bulk of their obligations come due. As commercial paper markets contracted earlier this year, companies began issuing bonds that mature in 20, 30 and 40 years.

The average maturity of investment grade debt has also lengthened, rising from a low of 12 years in 2009 to 17 years by the end of 2015, according to data at Sifma, the US trade group.

That has exposed investors to interest rate shocks, as bond prices rise and fall alongside the move in benchmark sovereign debt. The price sensitivity of long maturity bonds to the direction of interest rates has exacerbated losses within that debt. Prices of US corporate bonds maturing in more than 25 years have declined 5.7 per cent in November. Debt maturing within three and five years slipped 1.4 per cent by contrast.

In an environment of rising yields, prices for 10- and 30-year bonds fall the most and can quickly wipe out interest income earned from holding the paper.

Microsoft’s 30-year bond sold in August fell to 92.30 cents on the dollar last week, down 4.4 per cent since the presidential election. Bonds issued by Apple maturing in 2046 traded on Friday at 92.7 cents on the dollar, down from par as recently as October.

Richard Madigan, chief investment officer at JPMorgan Private Bank, says investors have crowded into corporate bonds and that “credit always ends badly”. Given the rise in overall borrowing by companies, he adds: “Balance sheets are fully loaded.”

Mr Madigan says a bite-back in credit will be intensified by the relative illiquidity of corporate bonds in the secondary market. “The problem with credit is that it takes time to change and it can be very disruptive.”

Although default models look at credit on the basis of whether a company will ultimately pay back the principal owed on debt at maturity — say 10 or 30 years — markets are far more demanding and their opinion can swiftly change, argues Mr Lapthorne.

“The way credit markets work is that we continually ask about the value of a company’s assets. Investors are in effect always asking, can this company repay its principal today, even though the repayment is not actually due for 30 years?’’

With the bond markets in the midst of a brutal post-election sell-off, investors are set to keep asking these questions.

0 comments:

Publicar un comentario