Elections and referendums in the year ahead pose a far different challenge from the financial crisis of recent years

By Greg Ip

The euro has survived sovereign default, recessions, banking crises and bailouts. It may not survive populism.

In the coming year, the eurozone will host at least five elections or referendums that could bring a populist, euroskeptic party to power. In effect, the common currency is about to play multiple rounds of Russian roulette.

The populist threat is qualitatively different from the financial crisis that first erupted in Greece in 2009 and eventually engulfed half the region. In that case, what worried private investors was that a country, or its banks, would default on its debt and be forced to leave the euro. Investors fled, driving interest rates sky-high and plunging the continent into recession.

The European Central Bank ended that panic by effectively promising not to let any country be forced out of the euro. By contrast, the threat today is that a country will choose to leave the euro.

Says Andrew Balls, who oversees bond strategy at Pacific Investment Management Co.: “It’s hard to see how the ECB could combat a French government calling a referendum on the euro.”

The first test comes Sunday, when Italians vote on a new constitution and Austrians elect a new president. Depending on the results, that could pave the way for new elections that eventually bring either the antiestablishment 5 Star Movement to power in Italy or the far-right Freedom Party in Austria. Next year, France, Germany and the Netherlands all hold national elections.

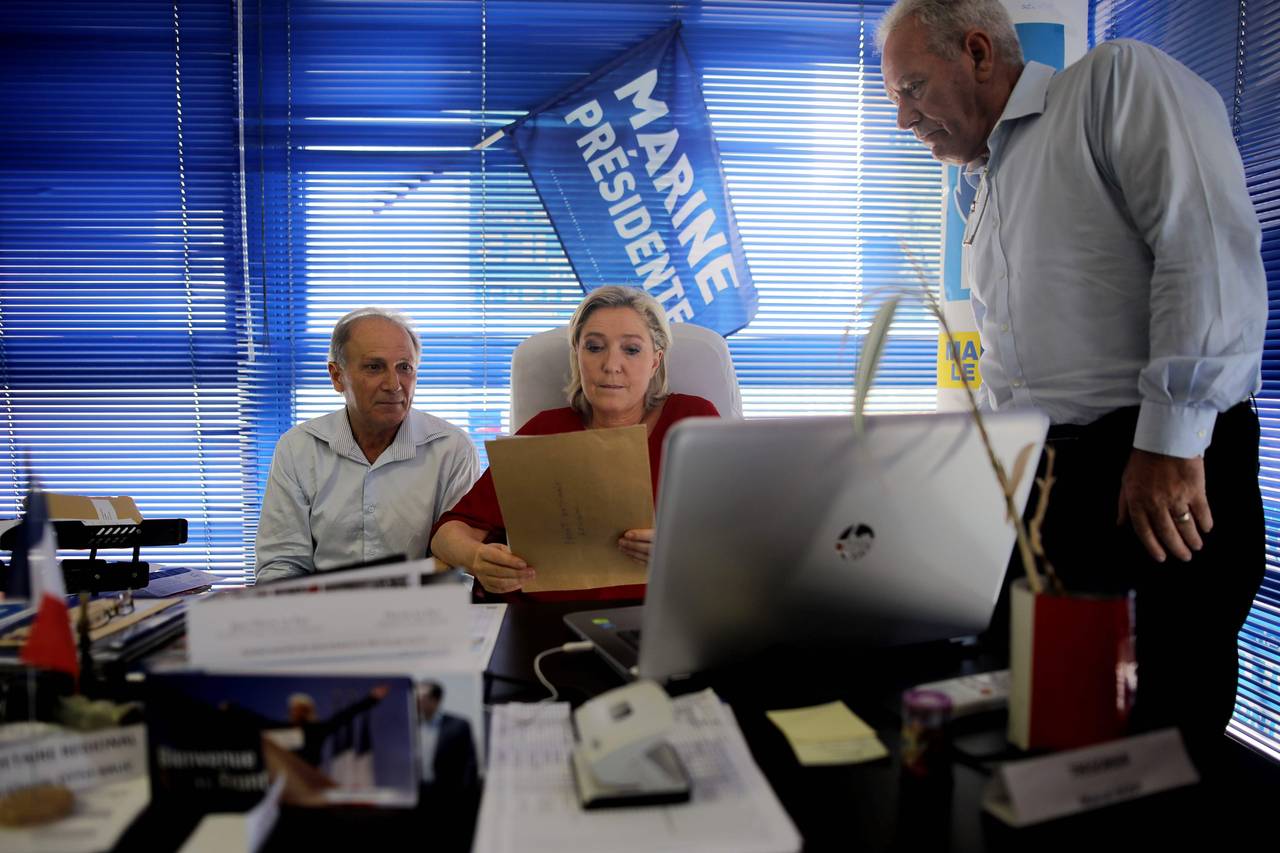

The biggest risk is that Marine Le Pen, leader of the anti-euro National Front, is elected president in France. Mrs. Le Pen isn’t expected to prevail in the second round against the Republican candidate François Fillon, and even if she did, her party wouldn’t control Parliament. Indeed, few of Western Europe’s populist parties are strong enough to form a government by themselves.

But momentum is moving in their favor. To be sure, Britons voted to leave the European Union and Americans elected Donald Trump president for reasons that may not resonate on the continent. Yet the fact that British and American voters defied the establishment and didn’t pay the predicted economic price reduces the stigma for Europeans inclined to cast an antiestablishment vote.

Moreover, the establishment is losing an important ally: Barack Obama is a vocal supporter of the European Union and euro. Mr. Trump and Europe’s anti-euro parties, by contrast, are fellow travelers.

The euro’s durability shouldn’t be underestimated. Despite the misery the euro has brought, polls show solid majorities in every major member country want to keep it. In fact, the euro is much more popular than the populists who would scrap it. Alternative for Germany began as an anti-euro party but languished in the polls until an influx of Middle Eastern refugees elevated its anti-immigration appeal.

Knowing this, populists may soften their opposition to the common currency as they get closer to power. The National Front, for example, may water down its euroskepticism when it releases its 2017 platform.

Yet even if the populists never take control of a legislature, their expanding presence threatens the common currency’s future. If Mrs. Le Pen closes in on the presidency next spring, investors may flee French debt for fear it will be redenominated into francs.

At that point, the ECB’s options are limited. It currently buys about €14 billion of French debt a month as part of a broader bond-buying program to stimulate growth. That’s slightly less than what France must borrow to finance its deficit and refinance maturing debt. The ECB could tilt more of its bond-buying toward France, but it can’t buy enough to absorb a broad-based selloff.

The ECB and the European Stability Mechanism, the region’s bailout fund, can explicitly support French debt only if France agrees to policy changes dictated by the European Commission. “Of course, Le Pen will never do that,” says Mujtaba Rahman of the political risk consultancy Eurasia Group.

Thus, the ever-present risk of a populist government could unsettle markets and undercut still-fragile recoveries. Establishment parties, threatened by the euroskeptic right, will in turn be reluctant to agree to the changes necessary to address the euro’s structural flaws, such as a larger common budget, deposit insurance or debt guarantees. The euro may yet survive the coming year; the coming decade looks much less promising.

Posters in support of the 'Yes' vote in Italy’s coming constitutional reform referendum are seen in Rome on Nov. 30, 2016. Photo: tony gentile/Reuters

Posters in support of the 'Yes' vote in Italy’s coming constitutional reform referendum are seen in Rome on Nov. 30, 2016. Photo: tony gentile/Reuters

0 comments:

Publicar un comentario