The dollar squeeze

The dollar’s strength is a problem for the world

What the recent strength of the dollar means for the global economy

.

WHEN economic historians look back on the years following the global financial crisis, they might ponder the exact moment at which the boom in offshore dollar-lending reached its zenith. Was it September 2012, when Zambia issued its debut Eurobond (dollar-denominated bond), at a yield of 5.4%, and received $12bn of orders? Perhaps it was a year later, when investors gobbled up an $850m Eurobond issue by a state-backed tuna-fishing venture in Mozambique. In between Petrobras, Brazil’s state oil company, was able to issue $11bn of ten-year bonds in May 2013, a record for an emerging-market firm, at a generously low yield of 4.35%.

Investors had reason to regret those purchases even before the dollar’s latest surge. Between November 9th, when Donald Trump won the presidential election in America, and the Thanksgiving holiday, the dollar rose by 3% against a basket of rich-world currencies. Such a jump in so short a time is rare. The dollar-borrowing binge during these years helps explain why the greenback bounced so sharply.

By the end of last year, governments and businesses outside America had racked up $9.7trn of debts denominated in dollars, according to the Bank for International Settlements (BIS), a clearer for central banks. Of this, $3.3trn was owed by borrowers in emerging markets, much of it sitting on company balance-sheets. In countries with foreign-currency debts, the exchange rate acts as a financial amplifier. A stock of dollar debt is like a short position. When a shock hits, the scramble to short-cover drives up the dollar.

The latest leg-up in the dollar has a proximate cause. Investors expect Mr Trump to find common ground with Congress on cuts to corporate taxes and increases in infrastructure spending. A fiscal splurge may push the Federal Reserve to raise interest rates more quickly, drawing capital back to America and lifting the dollar. If corporate-tax cuts spur multinational companies to repatriate the pile of earnings they have hitherto kept offshore, it will further buoy the greenback.

Monetary policy in the euro zone will stay easy. The European Central Bank is expected to extend its bond-buying programme at its next big policy meeting, on December 8th. And Mr Trump’s election is a “present” to the Bank of Japan, says Paul Sheard of S&P Global. In September it committed to overshoot its 2% inflation target. A weaker yen helps; in the weeks after Mr Trump’s election, it fell by 7%.

If a strong dollar is cheered in Tokyo and Frankfurt, it is rather less welcome in emerging markets—for three reasons. First, sharp falls in currencies put pressure on central banks to raise interest rates, both to prevent further depreciation and to contain the resulting inflation.

Turkey’s central bank raised interest rates on November 24th in response to a fall in the lira to an all-time low against the dollar, for example.

Second, a stronger dollar also has an indirect impact on credit conditions in emerging markets.

A study by Valentina Bruno of the American University in Washington and Hyun Song Shin, of the BIS, found that those emerging-market companies able to borrow in dollars act like surrogate financial firms, lending on a chunk of borrowed funds at home. When the dollar was weak, such firms borrowed freely in global markets. A strengthening dollar, in contrast, causes a general tightening of credit in emerging markets.

A third effect comes from the legacy of past dollar borrowing. As firms rush to pay off their dollar debts, which loom ever larger in home-currency terms, they are likely to cut back on investment and jobs.

.

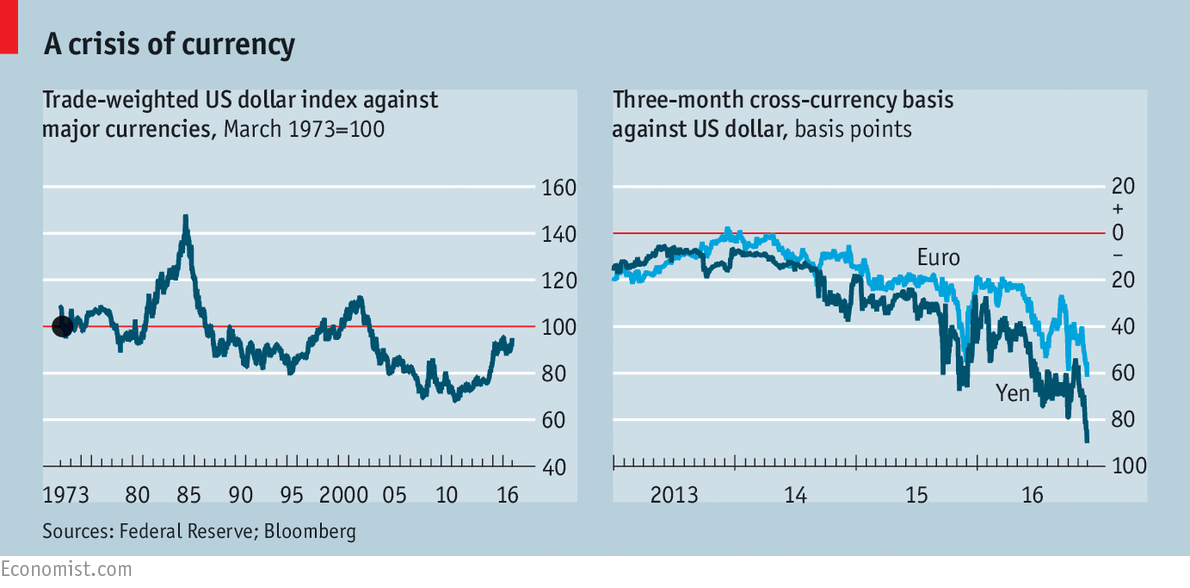

The impact of a stronger dollar is evident in rich-world finance, too. A shibboleth of finance is that foreign-exchange markets follow “covered-interest parity”, which says the forward rate should reflect the current (or “spot”) rate and the gap between interest rates on each currency.

Otherwise an arbitrager could simply buy a currency today, lock in the forward price, pocket the interest and still take a profit when the forward contract is settled. The interest-rate gap implicit in forward markets should be zero. For dollar-yen contracts in three months’ time it has blown out to almost 0.9%. That means firms and banks are paying far more than is normal to buy dollars with the currency risk hedged (see charts). The cost of hedging seems to rise with the dollar’s ascent.

Parallels have been drawn with an earlier period of sustained dollar strength. The dollar’s 50% increase between 1980 and 1985 was brutal for America’s exporters. The pressure for higher trade barriers was only defused by the Plaza Accord of 1985, a rich-country pact to weaken the dollar. The biggest concern about the latest dollar rally is that it will spur not agreement but conflict. Mr Trump seems all-too eager to resort to protectionism in a misguided attempt to balance America’s trade. A stronger dollar might be the trigger for such a disastrous move.

0 comments:

Publicar un comentario