Hawkish Fed Torpedoes Gold But Here Is Why We Think It Will Not Drop Far

by: Hebba Investments

.

- The Federal Reserve took a lot of investors by surprise as it raised rates but also issued a pretty hawkish statement.

- Speculative gold traders lowered their net long position for the sixth week in a row.

- This data was before the Fed decision, thus positions are probably much more bearish than shown below.

- On the physical side, gold demand in India and China is emerging at significant levels.

For the fifth week in a row investors saw net speculative long gold positions decline and gold dropped for a sixth straight week during the Commitment of Traders (COT) report trading week (Tuesday to Tuesday), as the golden metal dropped by another 1% during the trading week. What is interesting is that this all happened BEFORE the Federal Reserve decision - which means current long positions are even lower.

More importantly, we are seeing some very interesting demand arising from both China and India. Indian gold imports spiked in November on both a monthly and year-over-year basis, while in China gold premiums soared to some of the highest levels since 2013.

We will give our view and will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three-day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

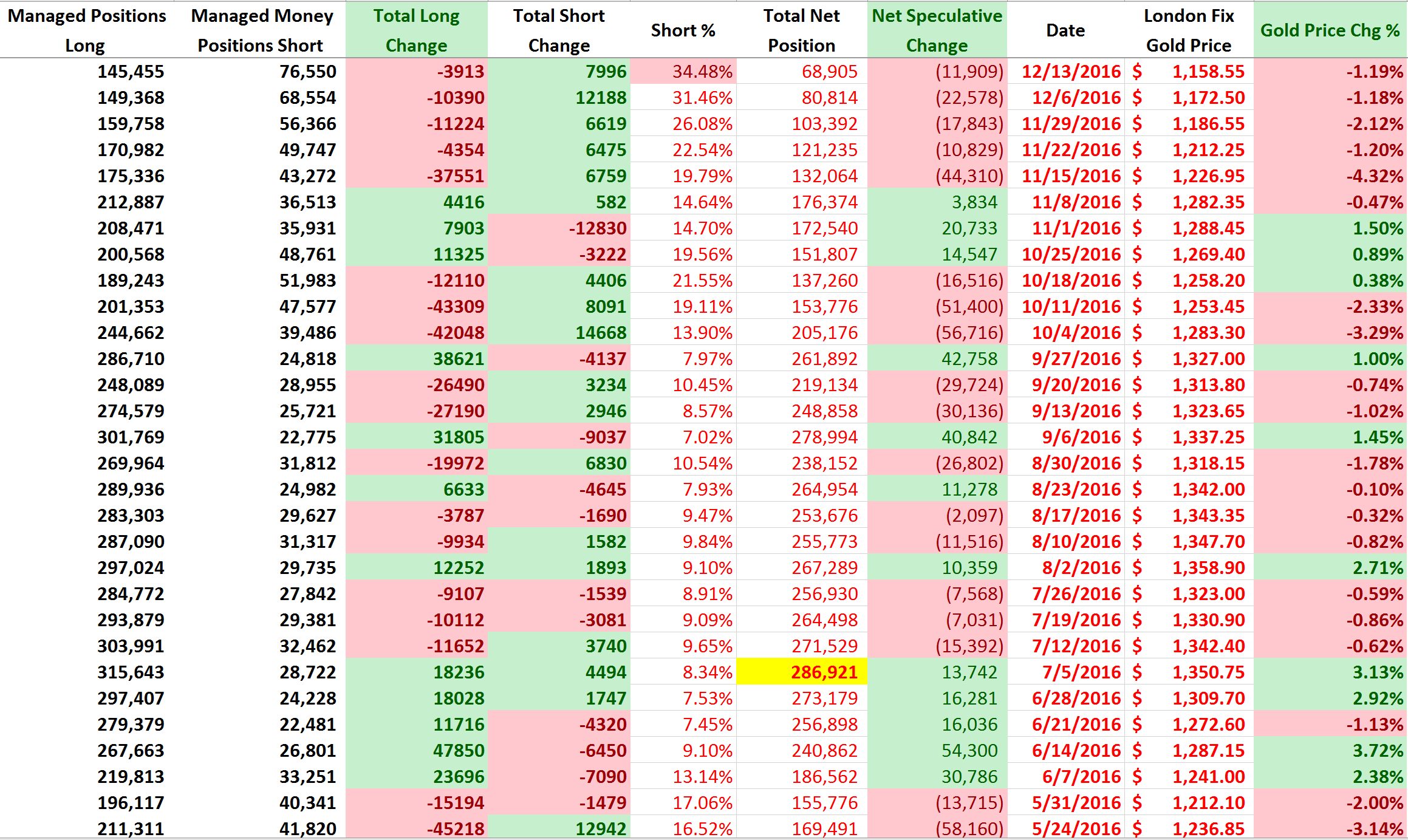

This Week's Gold COT Report

This week's report showed a drop in speculative gold positions for a fifth straight week as longs decreased their positions by 3,913 contracts on the week. On the other side, speculative shorts increased their own positions by 7,996 contracts on the week.

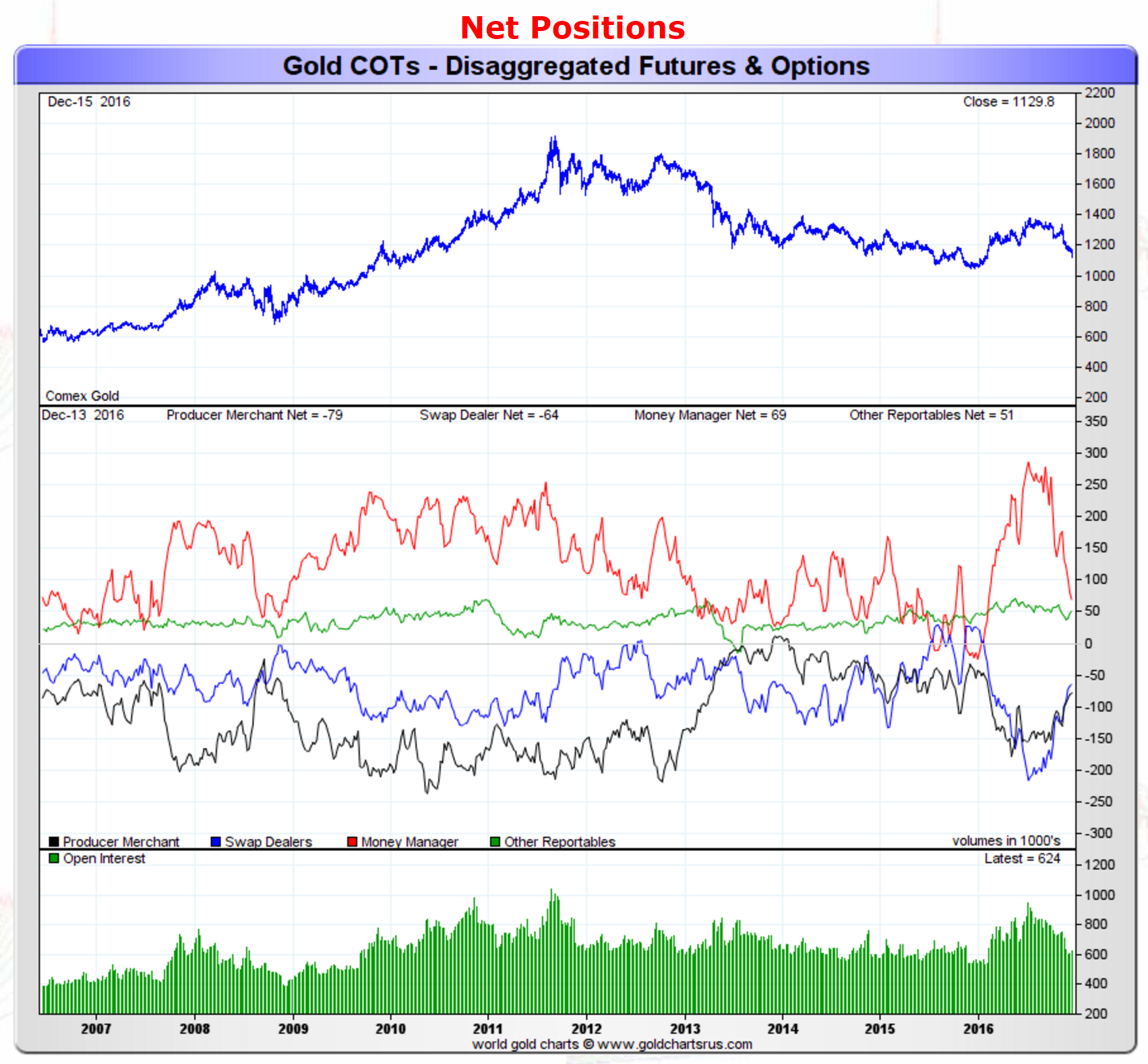

Moving on, the net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, the decline in speculative traders continued as the net long position fell to some of the lowest levels since early this year.

Speculative positions now stand at only 69,000 net long contracts - some of the lowest levels this year and that is a bit dated as gold has fallen further since these numbers were published.

Clearly the speculative froth is no longer present in the gold market.

Clearly the speculative froth is no longer present in the gold market.

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red line which represents the net speculative positions of money managers, shows a drop in speculative positions for the week which should be no surprise since silver tends to track gold.

But what is interesting here, and as we said last week, is that silver speculators have been much more bullish on silver and "sticky" with their positions as opposed to gold speculators.

The Federal Reserve Meeting, Indian Gold Imports, and Chinese Gold Premiums

Last week we mentioned that we expected the Federal Reserve to raise rates but issue a dovish statement. Looks like us and a lot of others were wrong - Janet Yellen and the Fed decided to not only raise rates but to be hawkish with their statement and expectation of three interest rate hikes in 2017. Now, we will not take this opportunity to comment on the Fed's decision except it really comes down to if there will be economic consequences to increased debt - we think with global leverage and the end of the 30-year bond market there will be. But that is a discussion for a different piece, but we do want to point investors to a very thought-provoking article by Patrick Watson of Mauldin Economics that brought up an interesting change to the Fed's website before this move in rates - worth the read.

But what we do want to look at are a couple of things with the gold market - and both are way to the East.

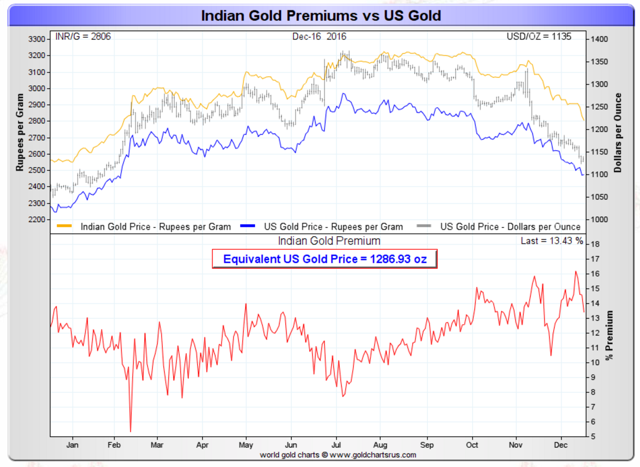

Indian Gold Imports Surge Despite Demonetization

Many sources have been claiming that Indian gold demand has plummeted because of demonetization and the lack of hard currency to purchase gold. That was also evident in the large drop in gold premiums that we noted in a previous piece about India.

It looks like gold demand rebounded quite sharply in India, as despite demonetization, based on recently released government data imports were up significantly. As reported in a Bloomberg Quant piece:

Gold imports rose to 15 month high of $4.4 billion compared to $3.5 billion in Oct-16 as seasonal demand for gold and demonetization lead to spike in sales, with unaccounted money reportedly being utilized for purchases…

Premiums have been jumping around a bit, but they are still at some of the highest levels of the year:

Source: Gold Chartsrus

Source: Gold Chartsrus

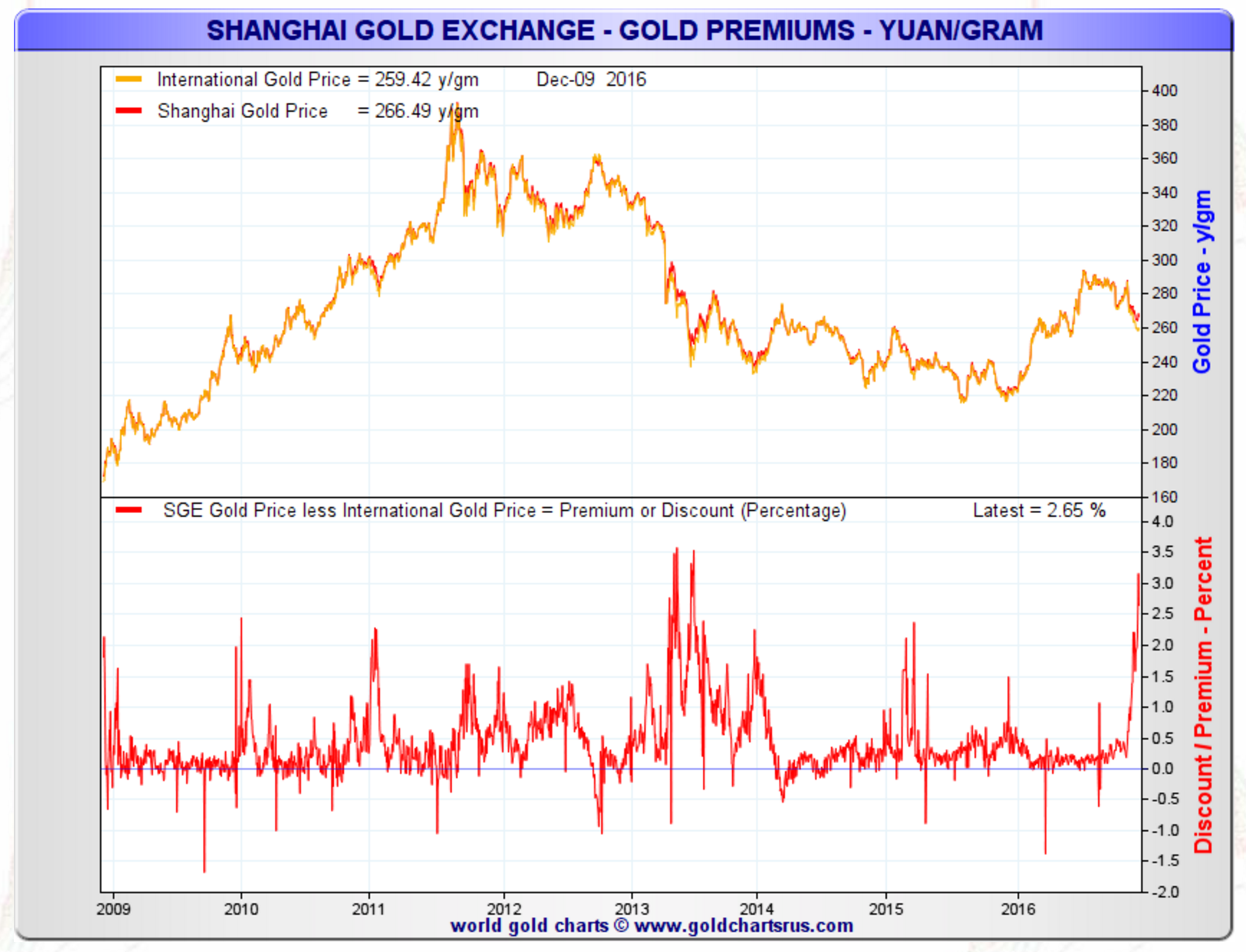

Chinese SGE Gold Premiums Surge

Moving over to China we see gold premiums spiking to some of the highest levels since 2013:

Source: Gold Chartsrus

Source: Gold Chartsrus

Now, of course that big surge in premiums doesn't mean we will see gold jump - but it certainly suggests that demand is strong in China.

Our Take and What This Means for Investors

Janet Yellen's Fed put a hawkish spin on the rate increase and that dropped gold and bonds as the markets were expecting a much more dovish tone. Based on the Fed statement, it looks like they believe that it is time to raise rates and the economy is strong enough to bear greater rates.

We have some serious doubts on that (as well as the consequences of higher rates across the globe), but regardless that is the path the Fed is taking so we must wait and watch for the consequences.

We have some serious doubts on that (as well as the consequences of higher rates across the globe), but regardless that is the path the Fed is taking so we must wait and watch for the consequences.

Is that good or bad for gold? The answer is… it depends.

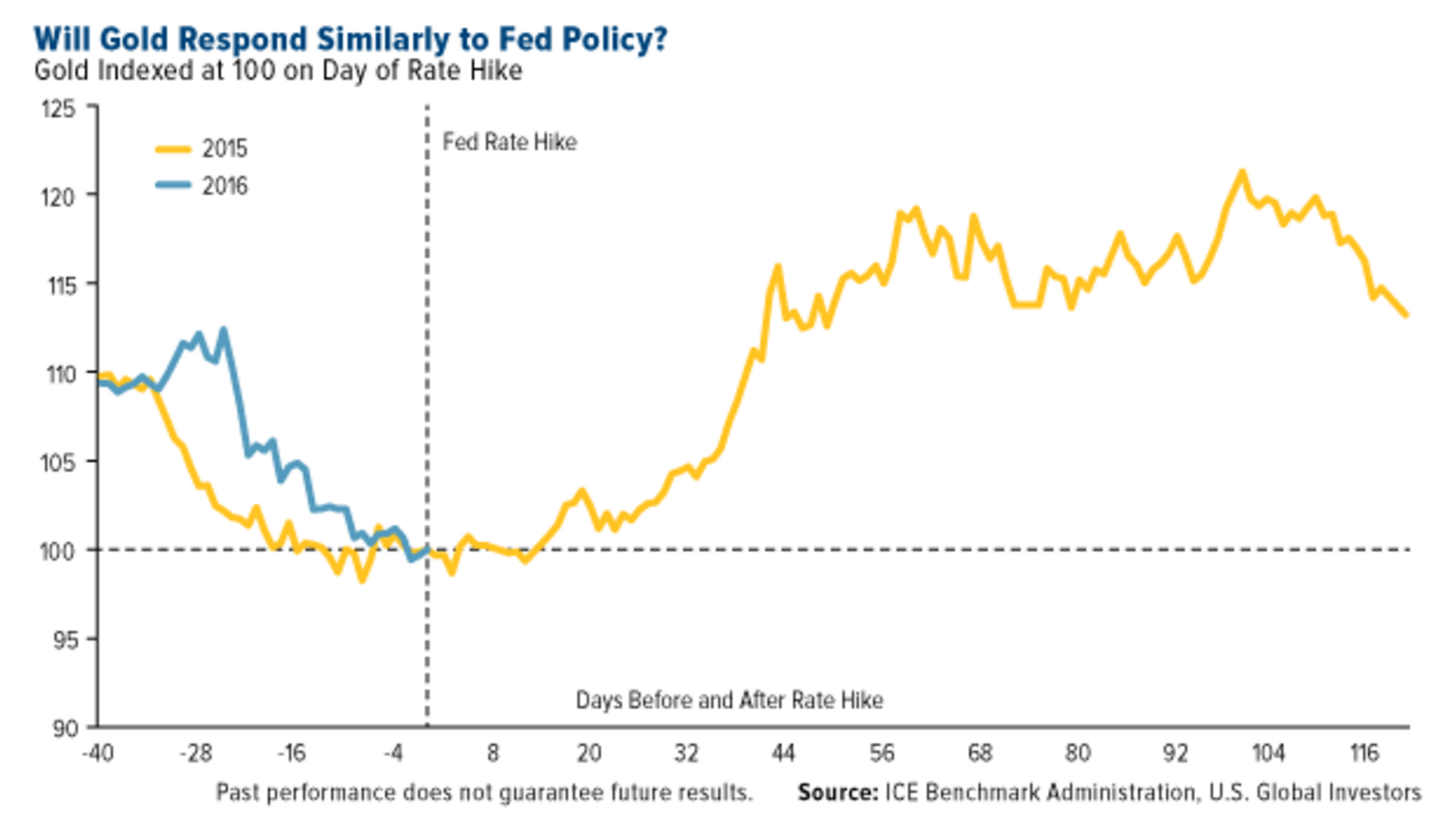

If the Fed is right and the economy can support higher rates and show quality, non-inflationary growth, then that is not a good thing for gold as income-producing businesses are much better suited to that environment. But if growth is inflationary or the consequences of higher rates cause dislocations in bond markets and across the globe with a financial system that is more leveraged with debt than it ever has been, then gold makes a very attractive asset. The point is just simply having higher rates are not the deciding factor to determine gold's direction. The 1970's were a good example of this as gold went up more than 10 times in value, but we do not even have to go that far to see gold reacting positively as we can simply go back to December of 2015 as this chart from US Global Investors shows:

Source: US Global Investors

Source: US Global Investors

On the positive side for gold is that physical demand is picking up in India and China with the recent price drop, and traders are very bearish on gold with six straight weeks of net position declines.

The point is that a strong healthy economy with fundamental growth (and not inflationary growth), would be negative for gold and in that case an investor would want to look elsewhere for alpha returns. But if the Fed is wrong, and the economy cannot sustain rising interest rates AND have fundamental non-inflationary growth, then gold looks extremely oversold here and investors should be licking their chops.

We do not think the world is ready for higher interest rates without some major dislocations in financial markets, especially the all-important bond markets. Almost ten years of extra-easy monetary policy needs to be reversed, and that will not be easy. Add in the fact that rising interest rates will signal a 30 plus year bond market is ending and we have a feeling bond investors (and the governments that need to raise money) will certainly some nasty surprises along the way.

But these things are more medium-term events, in the short-term based on the COT data, gold is extremely oversold and this data was BEFORE the Fed meeting plunge in precious metals.

We are not too concerned about the gold drop here and are taking the contrarian stance on gold here. Thus if investors haven't started re-accumulating gold we think that now is a great time to but gold and ETF's such as the SPDR Gold Trust ETF (NYSEARCA:GLD), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), iShares Silver Trust (NYSEARCA:SLV), and quality precious metals miners and explorers.

We are not too concerned about the gold drop here and are taking the contrarian stance on gold here. Thus if investors haven't started re-accumulating gold we think that now is a great time to but gold and ETF's such as the SPDR Gold Trust ETF (NYSEARCA:GLD), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), iShares Silver Trust (NYSEARCA:SLV), and quality precious metals miners and explorers.

0 comments:

Publicar un comentario