Enter The Dragon: China's Trials And Travails In The Age Of Trump

by: The Heisenberg

Summary

- Presenting two ways to characterize China.

- Reviewing a compendium of chaos from China's financial markets.

- Pondering whether the president-elect is tilting at windmills in the East.

- Reviewing a compendium of chaos from China's financial markets.

- Pondering whether the president-elect is tilting at windmills in the East.

Let's dumb it down.

There are basically two ways we can characterize China: 1) as a rising superpower that will, in due course, resurrect a global bipolarity that hasn't existed since the fall of the Soviet Union, or 2) as a schizophrenic basket case weighed down by a dizzying array of competing directives as the Politburo tries in vain to maintain a communist political order while simultaneously marking a transition to a more market-based economic system.

I'm inclined to go with the latter characterization, and as such, president-elect Trump's anti-China posturing seems a lot more like Don Quixote tilting at windmills than it does a brave new commander-in-chief standing up to the mighty dragon from the East.

"The biggest surprise since Donald Trump's election victory is his decision to pick a fight with China," FT's Edward Luce wrote over the weekend, in a piece called "Donald Trump's Collision Course With China."

While I like the article, I can't for the life of me figure out why Luce is surprised by Trump's determination to "pick a fight with China." The new president couldn't have made his misgivings about the country any clearer on the campaign trail - China is "stealing" our jobs, gutting our domestic manufacturing industry, and manipulating its currency.

Since winning the election, Trump has ruffled more than a few feathers in Beijing by implicitly (and later explicitly) questioning America's "One China" policy, ratcheting up the protectionist banter, and most recently, calling China's seizure of a US naval drone "unprecedented" (well, actually he called it "unpresedented" but later corrected the spelling) before ultimately telling the Chinese they could "keep" the small craft.

Beijing may be expanding its influence by, among other things, pushing for the internationalization of the RMB and declaring what amounts to an (unwanted) Chinese Monroe Doctrine in the South China Sea, but the country faces a laundry list of problems, many of which revolve around the economy and domestic financial markets.

These problems have been on full display since Trump's election. Indeed, Trump has sent shock waves through China without even realizing it. It's not a phone call with Taiwan or Twitter posturing about the theft of a naval drone that's hurt the Chinese over the last six weeks or so, it's the soaring dollar (NYSEARCA:UUP) and rising US Treasury yields (NYSEARCA:TLT) that have done the damage. Let me give you an example.

Last week, the FOMC hiked rates. That was expected. What wasn't expected was the shift in the dot plot which showed that the Fed now sees three rate hikes in 2017 as opposed to two. The reason for the more hawkish outlook: expectations for an even tighter labor market, higher economic growth, and higher inflation surrounding the implementation of Trump's fiscal stimulus initiative. Just hours later, the following headline hit the terminal:

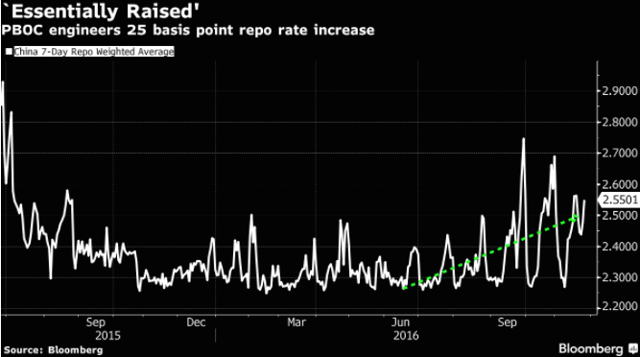

CHINA 10-YEAR SOVEREIGN BOND YIELD SURGES 22 BPS TO 3.45%

That was the biggest jump on record and prompted authorities to halt trading in some futures contracts that had fallen by as much as 2% in early trading. This was the reaction from various brokerages (via Bloomberg):

BOCOM International managing director for research Hong Hao

- Faster than expected rise in yield could see leveraged positions being squared, risk of snowball effect

- PBOC would try to keep money rates relatively steady to prevent excessive yield rise

- 10-yr yield may reach 3.8% near term; but further rapid pickup unlikely

Shenwan Hongyuan Asset money manager James Yip

- Rising rates negative for equities

- Selloff much quicker than expected; weakness to remain unless PBOC sends "comforting signals," such as by providing short-term funds

- No particular reason to go long now, nothing pointing toward reversal

Commonwealth Bank of Australia China economist Andy Ji

- While PBOC may be concerned pace of correction is too quick, compared with 2013 cash crunch market is not too distressed yet; liquidity risks yet to translate into credit or systemic risks

- Hard to see yield coming off significantly even in the mid-term

- Defaults could be delayed if PPI continues to rise

- Yields running ahead due to Fed hike expectation, but more because of domestic inflation and oil price outlook

- China onshore rates likely to continue to advance, with Shibor overnight rate to trade above 2.5%, if not higher: Ji

CCB International Securities Hong Kong-based co-head of research Peter So

- Higher onshore interest rates should help stem yuan outflows and narrow negative carry for Chinese banks to recycle offshore yuan back to onshore; will make it easier for China to squeeze offshore CNH liquidity

- Investors adjusting expectation on Fed hike pace; selloff inevitable in bonds, stocks in coming month on portfolio adjustments, year-end liquidity tightness

On the week, Chinese bonds put up their worst performance in two years, with yields on the 10-year, one-year, and five-year climbing 25, 50, and 27 bps, respectively. On Friday, the day after the rout, China came up short at a bill auction selling only 9.57 billion yuan ($1.38 billion) of 182-day bills in a planned 10 billion yuan sale and only 10.85 billion yuan of 91-day bills in a planned 12 billion yuan sale. It was the first failed auction in 18 months.

One problem - and this underscores the issues created by the competing agendas Chinese authorities are pursuing - is that China is attempting to rein in speculation by making short-term funding harder to come by. Here's WSJ:

China's central bank has guided short-term lending rates higher in order to squeeze out borrowers who are using the cheap money to make risky bets and loans.

Last week, some bondholders, including asset managers and issuers of "wealth management products"-off-balance-sheet investment vehicles used by banks and other institutions to get around regulatory limits on lending-were likely squeezed too much. As a result, they began dumping government bonds-which are liquid and thus easy to sell-to raise cash, analysts say.

What does that mean exactly? Well, it means this (via Barclays):

Chinese banks have offered c.4% yields on wealth management products while the 1y benchmark deposit rate has fallen to 1.5%. To generate higher yields, banks have been taking on more credit risks and increasing leverage in securities investments. A popular trade has been to borrow overnight and 7d in the interbank market, and then add leverage to buy rates or credit products. Such activity has helped to fuel a bond market bubble, which, in turn, has created liquidity and market risks.

So how is Beijing "guiding up short-term lending rates" without officially raising rates, you ask?

Well, by extending the maturity of reverse repos of course. Consider the following from Bloomberg:

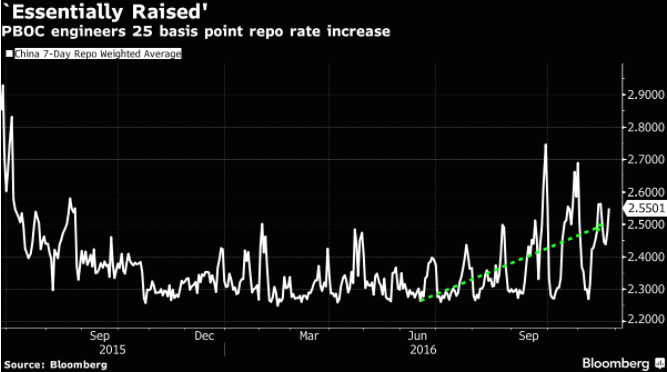

The People's Bank of China has cut back on seven-day open-market operations and is instead injecting more funds through 14-day and 28-day contracts. That's had the effect of raising short-term borrowing costs and pressing up bond yields.

Interbank rates have "basically gone up 20 to 30 basis points," said Ming Ming, the head of fixed-income research at Citic Securities Co. and an ex-PBOC oficial.

Bond returns are being hurt by a PBOC effort to squeeze financial-market leverage.

While the central bank injects money with seven-day reverse repurchase operations at 2.25 percent, it has started offering 14-day and 28-day contracts at rates as much as 30 basis points higher. The end result is secondary market one-week funding costs of around 2.5 percent.

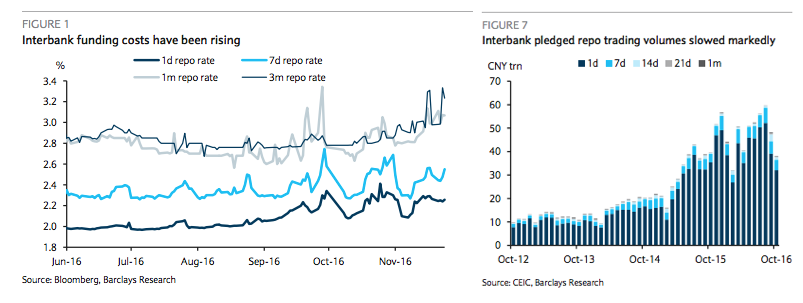

"[Most] telling of the central bank's policy stance, in our view, has been its resumption of longer tenor (14d and 28d) reverse repo operations since late August," Barclays noted, at the end of last month, adding that "we consider this a visible shift in the PBOC's monetary stance."

The bank continues: "These longer tenor and more expensive liquidity provisions from the central bank have led to: 1) an increase in the weighted averages of interbank funding costs (Figure 1); 2) a marked drop in pledged repo trading volumes; and 3) a fall in the share of overnight and 7d repo trading (Figure 7)."

(Charts: Barclays)

(Charts: Barclays)

The PBOC was forced to (temporarily at least) abandon the bias towards longer tenor liquidity ops to restore order. The PBOC injected CNY105 billion in seven-day funds late last week and another CNY95 billion in seven-day funds on Monday.

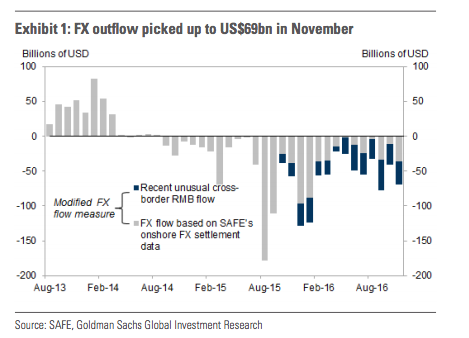

"Increased prospects for inflation-and a more hawkish Fed-come as Chinese regulators have already started to tighten short-term borrowing conditions in recent weeks to cool overheating Chinese markets [where] over the past year, speculators have borrowed from money markets to fund investments in bonds and other financial products," the Journal goes on to note, adding that "a weakening Chinese yuan, which has fallen 7.2% against the U.S. dollar this year, has also kept the pressure on officials to tighten monetary policy and stem capital outflows [as] the country's foreign-exchange reserves plummeted by $69 billion in November to $3.052 trillion, their lowest level since March 2011."

This is what I mean by "conflicting directives." If you engineer a tightening in money markets in order to curtail risk taking, you also risk putting stress on a system that's used to having ample liquidity.

As for the above-mentioned capital outflows, well they're worsening. According to Goldman, China's FX reserves have fallen by some $1.1 trillion since the August 2015 devaluation:

Cumulatively from August 2015 through November, FX outflow according to our measure totaled roughly US$1100bn, while implied FX sales suggested by PBOC's FX position (headline reserves after adjusted for currency valuation effect) were approximately US$630bn (US$540bn).

{kind=link}

Indeed, Treasury data out earlier this month showed China losing its crown as America's top debtor to Japan as the PBOC continues to liquidate US paper in an effort to manage the yuan's decline against the dollar. As a reminder, China can set the fixing lower, but is very often compelled to intervene in the spot market to ensure the currency doesn't overshoot to the downside.

"Some traders believe the $3 trillion mark is a key psychological level for the PBOC, but it risks rapidly churning through its remaining stockpile of reserves if the U.S. dollar keeps climbing and Beijing has to fight to steady the yuan," Reuters says, before noting that "Chinese government economists have put the minimum prudent level of reserves at somewhere between $1.62 trillion and $2 trillion."

Meanwhile, Beijing's efforts to control the amount of money companies can move out of the country have decreased the flow of yuan to the offshore market in Hong Kong, driving up short-term borrowing costs. Here's the Journal again:

In January, traders say the Hibor spikes were caused by the PBOC trying to head off bearish bets on the yuan in Hong Kong that had driven a wedge between the currency's value onshore and offshore.

At the time, traders said the PBOC directed state-owned banks to buy up large quantities of yuan in Hong Kong, driving overnight borrowing costs to an all-time high and squeezing investors out of their negative yuan bets.

Some companies have loans tied to Hibor, but the bigger impact is felt among foreign investors who access the yuan through the offshore market, traders and strategists say.

James Kwok, head of currency management at Amundi Asset Management in London, says he typically bets on a fall in the yuan by buying short-term forward contracts in the offshore market. A rise in borrowing costs makes it more expensive to buy those contracts, which means that the yuan has to depreciate more for such a trade to be profitable, he said.

"The process of authorization is going to become longer now," the head of a French construction materials company told WSJ, referring to the process by which he can move money made in China out of the country. "The procedures will be controlled more strictly."

You can see why I say Trump is tilting at Quixote-esque windmills. China has a lot more to worry about than US naval drones. Be that as it may, Beijing is concerned about the effect a rising dollar will have on emerging markets and also fears Trump doesn't have a good grasp of the intricacies of international politics (Beijing called him "as ignorant as a child" in the Taiwan spat). That's led some to question whether the Chinese may ultimately use a fire sale of US debt as a retaliatory measure.

That of course is not the best course of action as such a move would invariably drive down the value of China's remaining portfolio. "This (dumping U.S. debt) is a bad idea [and] it will not be among retaliatory measures to be considered by the government," one Chinese government policy adviser told Reuters.

The irony in all of this is that, as we saw last January and more poignantly in the aftermath of China's move to devalue the yuan in August of 2015, turmoil in Chinese financial markets and continued pressure on the country's currency can and will create significant blowback for assets across the globe.

In that regard, we'd be better served trying to help Beijing ensure that China's transition to a free floating currency and a consumption and services-led economy goes smoothly than we would attempting to undermine the country in word and deed at every possible turn.

0 comments:

Publicar un comentario