New president has an economic in-tray full of problems

The US system has its strengths but still shows scars from the Great Recession

by: Martin Wolf

In the country of the blind, the one-eyed man rules. The US economy shows significant flaws.

But it is a king when compared with its peers. It has recovered from the Great Recession, with unemployment low and real incomes rising. It also possesses abiding supremacy in new technologies.

Nevertheless, the next administration will take over a country with mediocre growth of productivity, high inequality, a growing retreat from work and a declining rate of creation of new businesses and jobs. At least the US fiscal position is not a really urgent threat. That is to the good, since nothing much is likely to be done about it.

The financial crisis of 2007-09 was a devastating event, economically and politically. But real gross domestic product per head had reached its trough by the second quarter of 2009 and recovered to pre-crisis levels by the final quarter of 2013. Similarly, the unemployment rate peaked at 10 per cent in October 2009 but is now back to 4.9 per cent. The financial sector is also in far better health than during the crisis.

Too many casual observers take this rapid turnround for granted. But the Great Recession could have been another Great Depression. It took bold action by the Federal Reserve, the administration of George W Bush and that of Barack Obama to turn the economy around so quickly. Everyone has benefited greatly from this success.

Nevertheless, the crisis has left deep scars. In the second quarter of 2016, real GDP per head was still only 4 per cent above its pre-crisis peak, almost nine years before. Labour productivity has grown slowly since the crisis, by historical standards, largely as a result of weakened investment. One study estimates US potential output is 7 per cent below levels suggested by pre-crisis trends. Yet average growth of US labour productivity, albeit slowly subsiding, has exceeded that of other leading high-income economies over the past 15 years. This is probably due to its dominance of high-tech innovation: the aggregate capitalisation of the five largest US technology companies is now over $2.2tn.

Yet, the scars left by the crisis, which include diminished confidence in the probity and competence of the financial, intellectual and policymaking elites, also came on top of older ones.

Real median household income increased by 5.2 per cent between 2014 and 2015. But it remains below pre-crisis levels. Indeed, it is below levels reached in 2000 and has even fallen relative to real GDP per head consistently since the mid 1970s. This performance helps explain the tide of disillusionment, even despair, revealed so starkly by this grim election (see charts).

Not surprisingly, inequality has worsened markedly. Between 1980 and the most recent period, the share of the top 1 per cent in pre-tax income jumped from 10 per cent to 18 per cent. Even after tax, it rose by a third, from 8 to 12 per cent. The rise in compensation of chief executives, relative to that of workers, has been huge. The US has the highest inequality of any high-income country and has seen the fastest rise in inequality among the seven leading high-income economies. The divergence among these countries suggests that rising inequality is far more a social choice than an economic imperative.

Closely related to the rising inequality has been a decline in the share of labour in GDP from 64.6 per cent in 2001 to 60.4 per cent in 2014. Workers have not only suffered from declining shares of the pie. Just as significant is the steady rise in the proportion of men aged 25 to 54 neither in work nor seeking it from about 3 per cent in the 1950s to 12 per cent now. Even France had a higher fraction of prime-age men in jobs than the US every year since 2001. Since 1990, the US has had the second-largest increase in male non-participation in the labour force of all members of the Organisation for Economic Co-operation and Development. After 2000, the declining trend in non-participation of prime-age women also halted. The proportion of US women in this age category in employment is now among the lowest of all the members of the OECD.

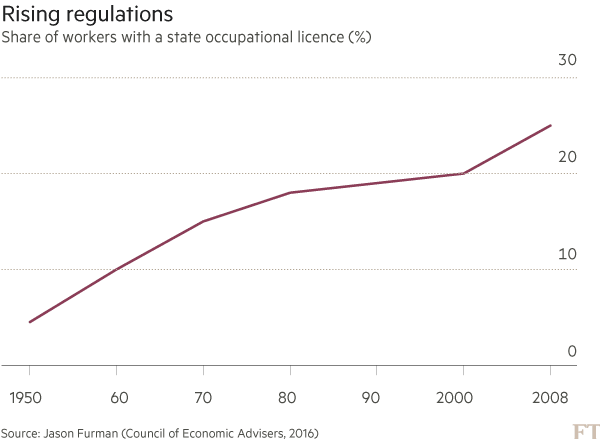

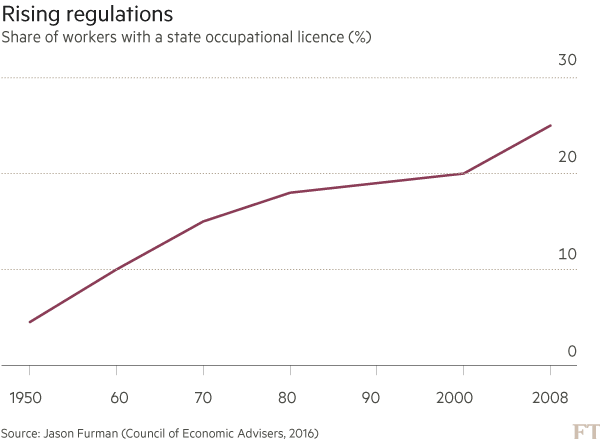

No less disturbing is a decline in economic dynamism. The rate of creation of new jobs has slowed markedly, as have rates of internal migration. The rate of entry of new businesses into the marketplace has also been falling over an extended period, as has the share of ones less than five years old in both the total number of businesses and employment. Meanwhile, business fixed investment has been persistently weak. Evidence also suggests a rising variation in returns on capital.

These are long-term trends, not just post-crisis events.

For all its strengths, the US economy could do better. In addition to the trends identified above, deteriorating infrastructure, worsening relative educational performance and a terrible tax code are challenges. Halting immigrants and imports would be an act of self-harm. The US must build on its historic strengths of an open and dynamic economy, together with government provision of infrastructure, research, education, and balanced tax and regulatory policies. A new administration needs the right diagnosis and co-operation from Congress. Pigs may also fly.

But it is a king when compared with its peers. It has recovered from the Great Recession, with unemployment low and real incomes rising. It also possesses abiding supremacy in new technologies.

Nevertheless, the next administration will take over a country with mediocre growth of productivity, high inequality, a growing retreat from work and a declining rate of creation of new businesses and jobs. At least the US fiscal position is not a really urgent threat. That is to the good, since nothing much is likely to be done about it.

Too many casual observers take this rapid turnround for granted. But the Great Recession could have been another Great Depression. It took bold action by the Federal Reserve, the administration of George W Bush and that of Barack Obama to turn the economy around so quickly. Everyone has benefited greatly from this success.

Nevertheless, the crisis has left deep scars. In the second quarter of 2016, real GDP per head was still only 4 per cent above its pre-crisis peak, almost nine years before. Labour productivity has grown slowly since the crisis, by historical standards, largely as a result of weakened investment. One study estimates US potential output is 7 per cent below levels suggested by pre-crisis trends. Yet average growth of US labour productivity, albeit slowly subsiding, has exceeded that of other leading high-income economies over the past 15 years. This is probably due to its dominance of high-tech innovation: the aggregate capitalisation of the five largest US technology companies is now over $2.2tn.

Yet, the scars left by the crisis, which include diminished confidence in the probity and competence of the financial, intellectual and policymaking elites, also came on top of older ones.

Real median household income increased by 5.2 per cent between 2014 and 2015. But it remains below pre-crisis levels. Indeed, it is below levels reached in 2000 and has even fallen relative to real GDP per head consistently since the mid 1970s. This performance helps explain the tide of disillusionment, even despair, revealed so starkly by this grim election (see charts).

Not surprisingly, inequality has worsened markedly. Between 1980 and the most recent period, the share of the top 1 per cent in pre-tax income jumped from 10 per cent to 18 per cent. Even after tax, it rose by a third, from 8 to 12 per cent. The rise in compensation of chief executives, relative to that of workers, has been huge. The US has the highest inequality of any high-income country and has seen the fastest rise in inequality among the seven leading high-income economies. The divergence among these countries suggests that rising inequality is far more a social choice than an economic imperative.

Closely related to the rising inequality has been a decline in the share of labour in GDP from 64.6 per cent in 2001 to 60.4 per cent in 2014. Workers have not only suffered from declining shares of the pie. Just as significant is the steady rise in the proportion of men aged 25 to 54 neither in work nor seeking it from about 3 per cent in the 1950s to 12 per cent now. Even France had a higher fraction of prime-age men in jobs than the US every year since 2001. Since 1990, the US has had the second-largest increase in male non-participation in the labour force of all members of the Organisation for Economic Co-operation and Development. After 2000, the declining trend in non-participation of prime-age women also halted. The proportion of US women in this age category in employment is now among the lowest of all the members of the OECD.

No less disturbing is a decline in economic dynamism. The rate of creation of new jobs has slowed markedly, as have rates of internal migration. The rate of entry of new businesses into the marketplace has also been falling over an extended period, as has the share of ones less than five years old in both the total number of businesses and employment. Meanwhile, business fixed investment has been persistently weak. Evidence also suggests a rising variation in returns on capital.

These are long-term trends, not just post-crisis events.

For all its strengths, the US economy could do better. In addition to the trends identified above, deteriorating infrastructure, worsening relative educational performance and a terrible tax code are challenges. Halting immigrants and imports would be an act of self-harm. The US must build on its historic strengths of an open and dynamic economy, together with government provision of infrastructure, research, education, and balanced tax and regulatory policies. A new administration needs the right diagnosis and co-operation from Congress. Pigs may also fly.

0 comments:

Publicar un comentario