A Great Migration Is Underway

by: William Koldus, CFA, CAIA

- The great bond bull market is in jeopardy.

- As interest rates have risen, investor positioning has changed, and is set to change further.

- Who will be the winners, as the shift from a deflationary environment to an inflationary environment continues?

- As interest rates have risen, investor positioning has changed, and is set to change further.

- Who will be the winners, as the shift from a deflationary environment to an inflationary environment continues?

"Be stubborn on vision and flexible on journey"

- Noramay Cadena

"Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria"

- Sir John Templeton

"Life and investing are long ballgames."

- Julian Robertson

Source: Stock photo.

Introduction

The seemingly impenetrable armor of the thirty-five year bond bull market has been pierced, as long-term sovereign bonds have suffered one of their worst sell-offs in recent history.

Building on this narrative, the iShares 20+Year Treasury Bond ETF (NYSEARCA:TLT) had its worst week since its 2002 inception, in the week ending November 11th, 2016, and that sell-off in sovereign debt has continued in the U.S. bond market, and around the world.

Market pundits widely attribute the accelerated rise in bond yields to the unexpected Trump victory in the November 8th, 2016 presidential election. While it is certainly true that the election changed the narrative, from my perspective, it merely hastened trends that were already in place.

With the humpty dumpty crystal ball of market prognosticators broken again, investors, speculators, and traders are trying to put together the pieces in order to get a clearer view of the future.

This has caused a wide range of reactions in asset prices, sometimes contradictory in nature, and some of these moves will turn out to be the real thing, while others will fade with the passage of time.

Thesis

The disinflationary/deflationary narrative is shifting to an inflationary narrative.

Bond Prices React

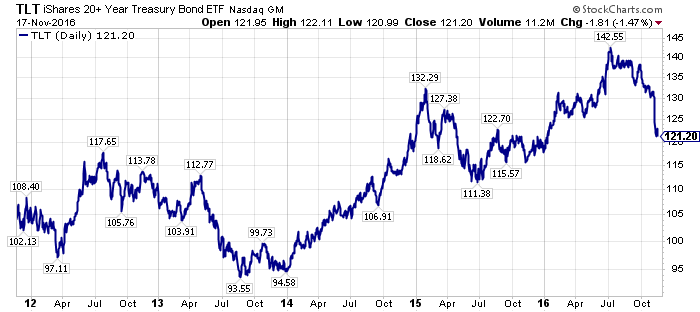

The visual picture of TLT shows the carnage in long-term sovereign debt.

Source: William Travis Koldus, stockcharts.com.

Earlier this year, I postulated that the bond bubble was about to burst, and that prediction is looking better by the day.

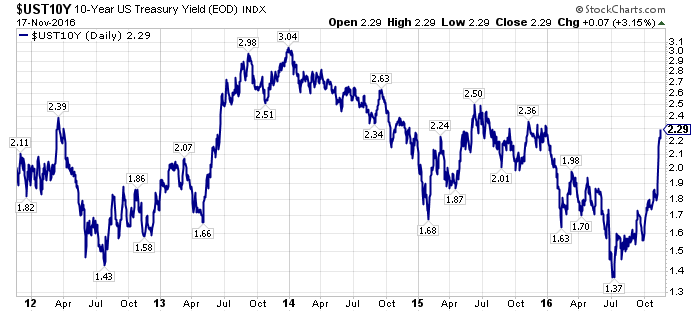

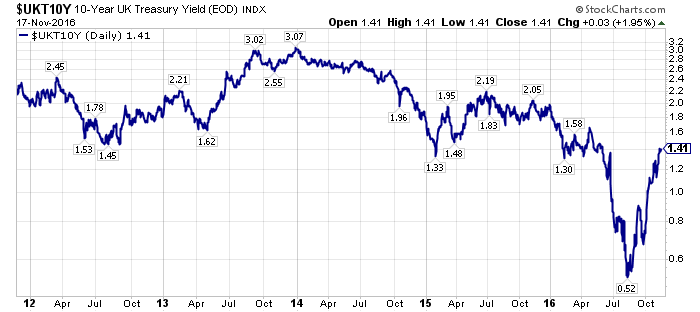

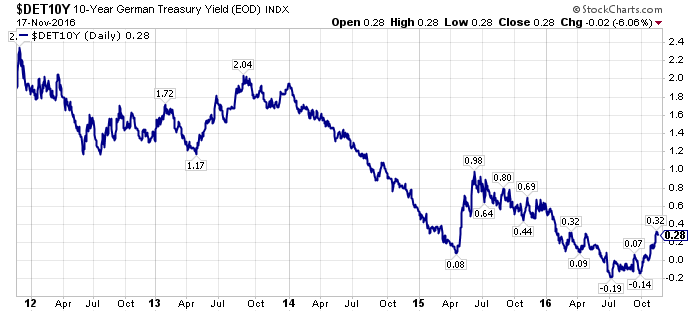

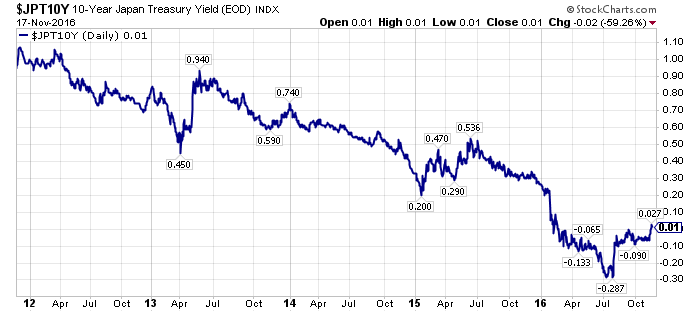

Adding evidence to the bond bubble bursting theory, long-term sovereign bond yields have continued higher around the world, including in the U.S., the U.K., Germany, and Japan.

Source: WTK, stockcharts.com.

U.S. 10-Year Treasury Yields have recovered all of their losses in 2016, U.K. 10-Year Treasury Yields have recovered all of their losses from the surprise "Brexit" vote, which has turned out to be a non-event thus far, and Germany and Japan have seen their yields move substantially off of their 2016 lows, with both countries' sovereign bonds yields now back in positive territory.

Investors Retreat From Yield-Orientated Securities

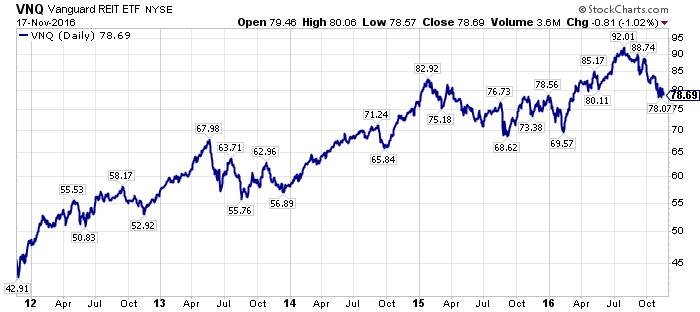

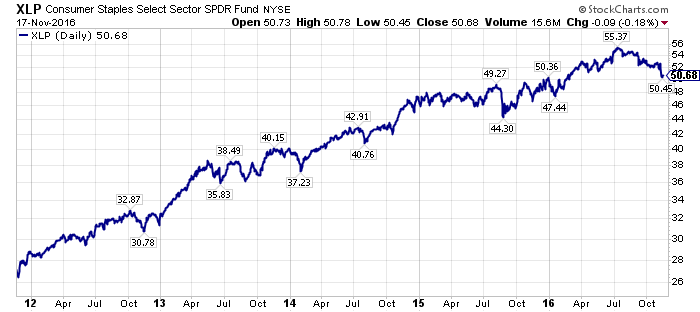

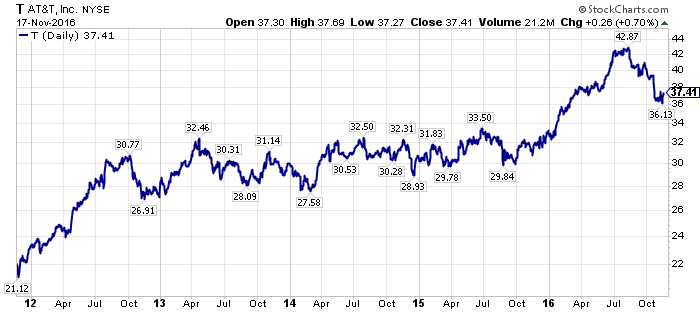

The prospect of lower interest rates for a longer period of time drew investors, like moths to a flame, to yield-orientated investments, including the R.U.S.T. group, which is an acronym for REITs, utilities, staples, and telecom shares.

These equities, as measured by the Vanguard REIT ETF (NYSEARCA:VNQ), the Utilities Select Sector SPDR Fund (NYSEARCA:XLU), the Consumer Staples Select SPDR Fund (NYSEARCA:XLP), and telecom heavyweights AT&T (NYSE:T), and Verizon (NYSE:VZ), have sold off sharply, as interest rates have risen beyond most investors' expectations.

Source: WTK, stockcharts.com.

By looking at the selected charts above, it is clear to see that a yield bubble had developed, and expanded to euphoria levels in 2016, and this bubble has now popped.

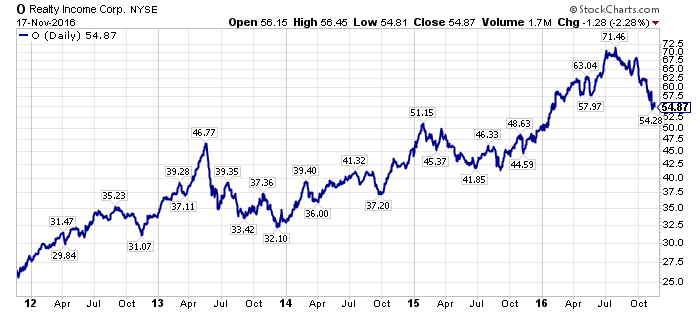

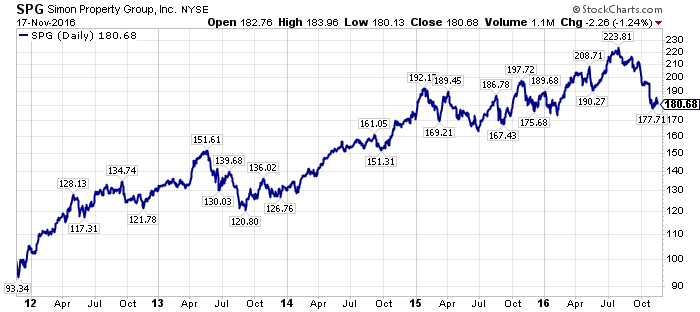

Further evidence is visible in the price performance of the shares of one of the most sought after yield oriented companies, Realty Income (NYSE:O), and the biggest REIT, Simon Property Group (NYSE:SPG).

Source: WTK, stockcharts.com.

Shares of Simon Property Group are now down 3.9% year to date, compared to the S&P 500 Index's gain of 9.1%, as measured by the SPDR S&P 500 ETF (NYSEARCA:SPY). This negative return for SPG shares stands in stark contrast to the 19% gain that shares were sporting at the end of July.

Realty Income shares, which I have been bearish on this summer, are now only up 9.7% YTD, which sounds good in the abstract, but these same shares were up 42.9% at the end of July, so they have given back a significant portion of their previous 2016 gains.

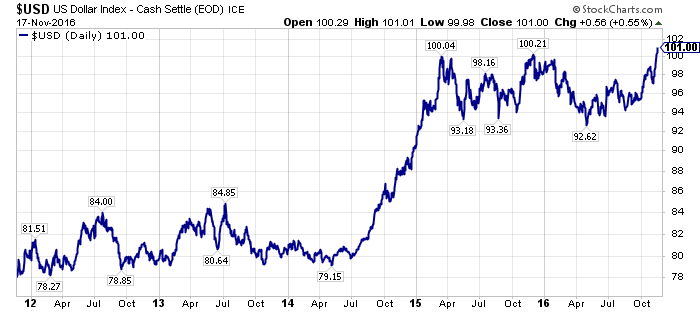

With U.S. Yields Leading, The U.S. Dollar Is Surging

The U.S. Dollar Index has been up nine straight days, and five of the last seven weeks.

Source: WTK, stockcharts.com.

The U.S. Dollar Index is now at multi-year highs, and is at an inflection point. Will it break through resistance?

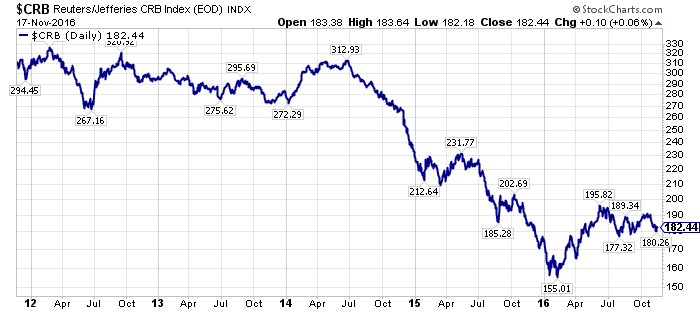

The Stronger Dollar Has Impacted Commodity Prices

The Reuters/Jefferies CRB Index has pulled back, and has been consolidating in a range, after rallying for the majority of the first half of 2016.

Source: WTK, stockcharts.com.

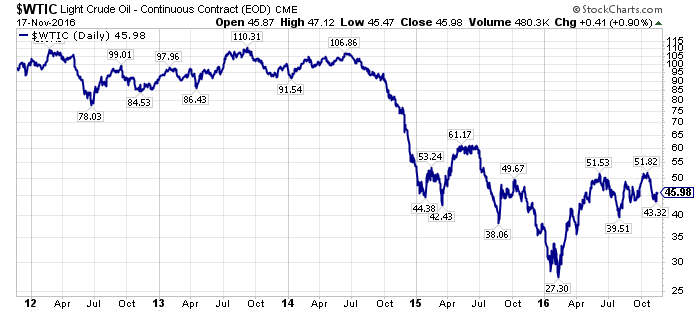

Crude oil prices (NYSEARCA:USO) show a similar price pattern, consolidating within a price range, after a substantial rally in the first half of 2016.

Source: WTK, stockcharts.com.

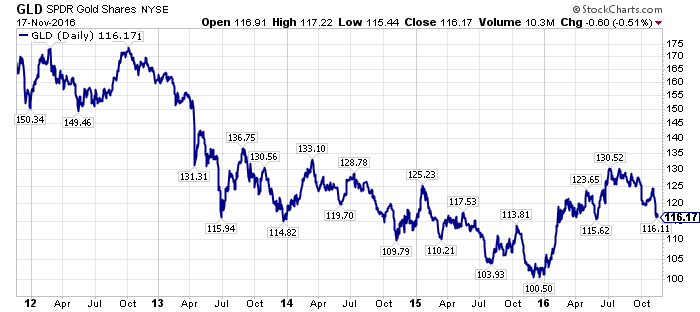

Gold prices, as measured by the SPDR Gold Shares ETF (NYSEARCA:GLD) rallied earlier, and more persistently, than crude oil prices, or the broader commodity index in general.

Source: WTK, stockcharts.com.

Are gold prices bottoming after a multi-month decline that began in July, or are they poised to move lower, pressured by higher interest rates?

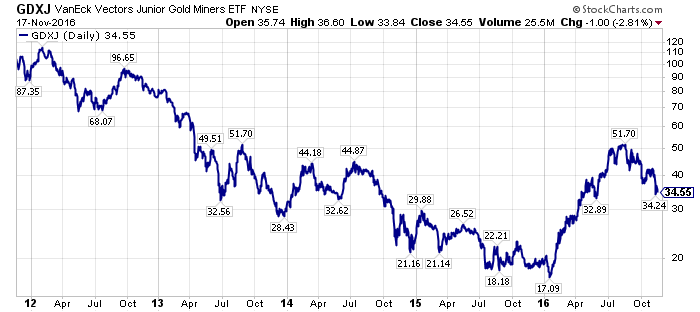

Look for gold stocks, as represented by the VanEck Vectors Gold Miners ETF (NYSEARCA:GDX) and the VanEck Vectors Junior Gold Miners ETF (NYSEARCA:GDXJ) to provide the first clues as to the direction that precious metals prices themselves, will break.

Source: WTK, stockcharts.com.

Precious metal stocks will often lead the precious metals prices themselves at market inflection points.

Commodity Prices and Commodity Stocks Are Still Leading

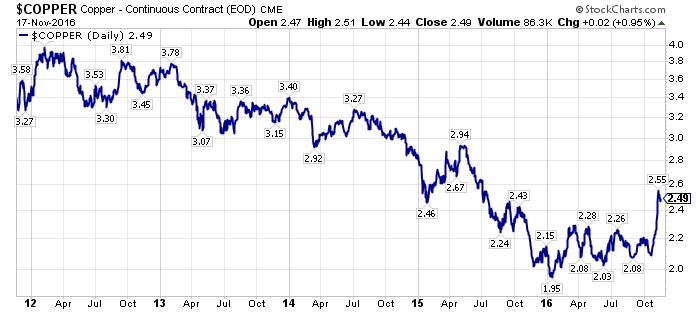

While the price consolidations of the energy market and the precious metals sector have weighed on the broader commodity indices, industrial commodities have turned up, and this is best represented by the price performance of copper (NYSEARCA:JJC).

Source, WTK, stockcharts.com.

Copper prices have surged, and this surge began prior to the results of the U.S. election. The impulse move higher in copper has the red metal joining its zinc, nickel, and metallurgical coal industrial brethren in making significant prices gains this year.

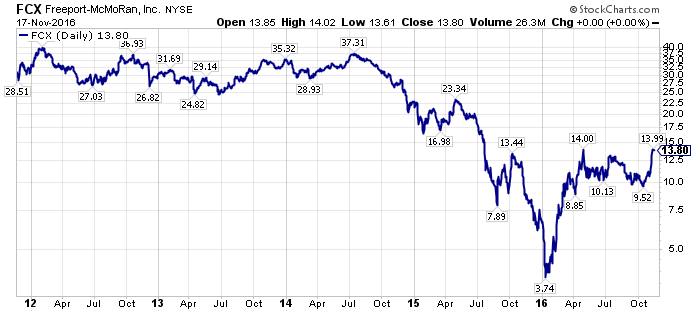

Freeport-McMoRan (NYSE:FCX), one of the earlier companies profiled in my "Too Cheap To Ignore" series of articles, has exemplified the move higher in industrial commodity stocks over the past several weeks.

Source: WTK, stockcharts.com.

The steel sector has joined the infrastructure party, as the world gears up for a potential revival in growth led by infrastructure spending.

The SPDR S&P Metals & Mining Index ETF (NYSEARCA:XME), which counts steel companies AK Steel (NYSE:AKS), Steel Dynamics (NASDAQ:STLD), Worthington Industries (NYSE:WOR), United States Steel (NYSE:X), and Nucor (NYSE:NUE) among its top-ten holdings, has rallied to new 2016 highs, and has now gained 99.8% in 2016.

Source: WTK, stockcharts.com.

U.S. Steel, where my father worked for nearly two decades before becoming a school teacher and athletic coach in the mid 1980s, I know, I am getting older too, is perhaps the prototypical former American industrial giant left behind in a world of globalization. However, this year, its shares have risen 270.1%.

Source: WTK, stockcharts.com.

The unexpected results of the election obviously boosted shares, but U.S. Steel, like much of the inflationary commodity complex, was already well into a recovery that had begun earlier in 2016, when deflationary fears reached their peak.

The Takeaway - The Rotation Into Inflationary Assets Has Accelerated

Source: Stock photo.

A surge in sovereign bond yields has sent retail yield-focused investors scrambling away from their favorite companies, and it has forced institutional investors to reexamine their assumptions regarding the prevalent risk parity strategies.

When the wildebeests of the Serengeti encounter a predator, like a lion, along their migration, the seemingly calm proceeding becomes a jumbled affair, and in similar fashion, the unexpected results of the U.S. election, and to a lesser degree, the U.K. referendum, have scattered market participants.

Once the dust settles, the inflationary trend that has existed since the markets depths earlier in 2016, will become apparent and further strengthened from my perspective. Thus, investors, speculators, and traders should focus on the new market leadership, as they reposition their portfolios and trading books for an investing landscape that is distinctly different from the 2011-2015 investing environment.

0 comments:

Publicar un comentario