When Will The Next Too Big To Fail Bank Fail?

by: Kurt Dew

Summary

- The next Too Big to Fail (TBTF) bank could fail within three years.

- This is the most arresting observation by Natasha Safer and Lawrence Summers in their recent article.

- Safer and Summers find the banking system dramatically riskier than do government officials.

- This article compares the methods of the two camps and asks why they differ.

- The Safer and Summers position is far more persuasive.

- This is the most arresting observation by Natasha Safer and Lawrence Summers in their recent article.

- Safer and Summers find the banking system dramatically riskier than do government officials.

- This article compares the methods of the two camps and asks why they differ.

- The Safer and Summers position is far more persuasive.

Our life is frittered away by detail. Simplify, simplify.

-- Henry David Thoreau

To listen to President Obama or Fed Chair Yellen, the problem of large bank failures in a liquidity crisis has been brought under the regulator's firm control. Natasha Safer and Lawrence Summers hold an opposing point of view. They suggest the next Too Big to Fail (TBTF) liquidity crisis might be as close as three years away. This article argues that Safer and Summers' approach is both more useful and more accurate than that of the regulators. And, normal humans can understand it.

Contrasting Safer and Summers with the regulators.

These dramatically different views are held for at least three reasons:

- First, both the President and the Chair have views tinged by their current responsibilities within government and regulation. Chair Yellen denied that politics influence Fed monetary policymaking in a news conference this week. Not only is that false, it would be irresponsible of the Fed if it were true. Politics affects and is affected by monetary policy. The two are interdependent. This is not in any way a failing of the Fed. It is simply a statement of the Fed's responsibilities. Lawrence Summers, on the other hand, has moved his headquarters from the Administration to academia. Rarely, however, has a person with such weighty previous responsibilities within government been so thorough in changing perspective. By reading the piece, coauthored by Natasha Safer, Have Big Banks Gotten Safer? analyzing bank regulation, you would have no idea of his past responsibilities. Not so with former Fed Chairman Bernanke, to compare Summers with another giant of the Crisis. Bernanke is still very much former Chairman Bernanke, not yet completely Professor Bernanke.

- Second, the opinions of regulators and political office-holders, on one hand, and those of Safer and Summers, on the other, are based on entirely different ways of measuring the risks confronted by banks. The President and the Chair are entirely focused on the book values of risky financial instruments and measures of risk provided by apparatchiks such as the rating agencies. There is a nod given to the banks' own statements of their risks. For example, the banks are allowed to provide their own forecasts of losses under duress. But there is evident regulatory skepticism about bank veracity. While I share this skepticism, I am no less skeptical about regulatory veracity. Safer and Summers, in contrast, focus on the measures of risk provided by financial markets. These measures are preferable to book values and agency ratings for important reasons.

- Market measures of risk are provided by investors, with skin in the game, collectively; not by staff, with no skin in the game, individually.

- These measures, by virtue of their market location, cannot do what they should not do - divorce the issue of risk from the inseparable issue of profitability.

- Market measures of safety innately include the direct impact on the banks, both positive and negative, of the decisions of office-holders and regulators. This, politicians and regulators scrupulously avoid.

- Third, Safer and Summers believe in the value of simplicity in policy. The current regulators are lost deep in the weeds of detail.

Why the difference?

Government officialdom must legislate and regulate based on reports formed of solid rock, rather than the shifting sands of markets. Nonetheless, in addressing the extremely important question, "Is Dodd Frank delivering greater bank safety?" any source of information, particularly if that source is more likely accurate than reports provided to regulators, ought to be carefully considered in deciding how to proceed with bank regulation. The bottom line on the difference between market measures of bank safety and soundness is provided by Haldane and Madouros' delightful " The Dog and the Frisbee." This is a "must read" by two economists at the Fed, but located in the "show me" state where heretics are safer than those located in the belly of the beast, Washington D.C. Safer and Summers explain the point thus: "[Haldane and Madouros] note that in a horse-race between the simplest market measure of risk (the market value of equity relative to unweighted assets) and the most complex regulatory measure (the Basel Tier 1 ratio), the explanatory power of the simple measure in predicting bank failure is about 10 times greater than the complex one."

Conclusion

I reaffirmed several of my prior beliefs from analyzing Safer and Summers' work.

- Bank regulation is far too complicated. Both Safer and Summers, and Haldane and Madouros, provide thoroughly convincing arguments that bank regulation is lost in a welter of unnecessary complexity. Between the Fed's Comprehensive Capital Analysis and Review (CCAR), the requirement that TBTF institutions submit "living wills," and the capricious manner in which both sets of regulations are enforced and evaluated, billions are wasted by both regulators in banks in the name of appearing to be thorough. The rules are not thorough; they are obscure, and of marginal relevance.

- Risk and return are not separable concepts. When one only, risk, is regulated, the effect is ultimately to drive the profitable, risky, side of the banking business into other financial venues. In other words, the bank regulators, like invasive parasites, are slowly destroying their bank hosts. The big banks have substantial culpability however, and are helping to marginalize themselves due to these factors:

- The OTC dealer banks have contributed in a major way to their own comeuppance. They have built their oligopolistic prison brick by brick. That the government is institutionalizing the big bank's irrelevance is only a second drink at the trough of foolish avarice.

- Our financial system outside the banks is still highly vibrant and creative. As Safer and Summers indicate, the share of the financial intermediation outside the banks is growing as the share inside the business declines.

- There has been no reduction in the risk of bank failure. Based on their analysis of these market measures:

- Various measures of the relative market volatility of bank liabilities and equity relative to those measures before the crisis.

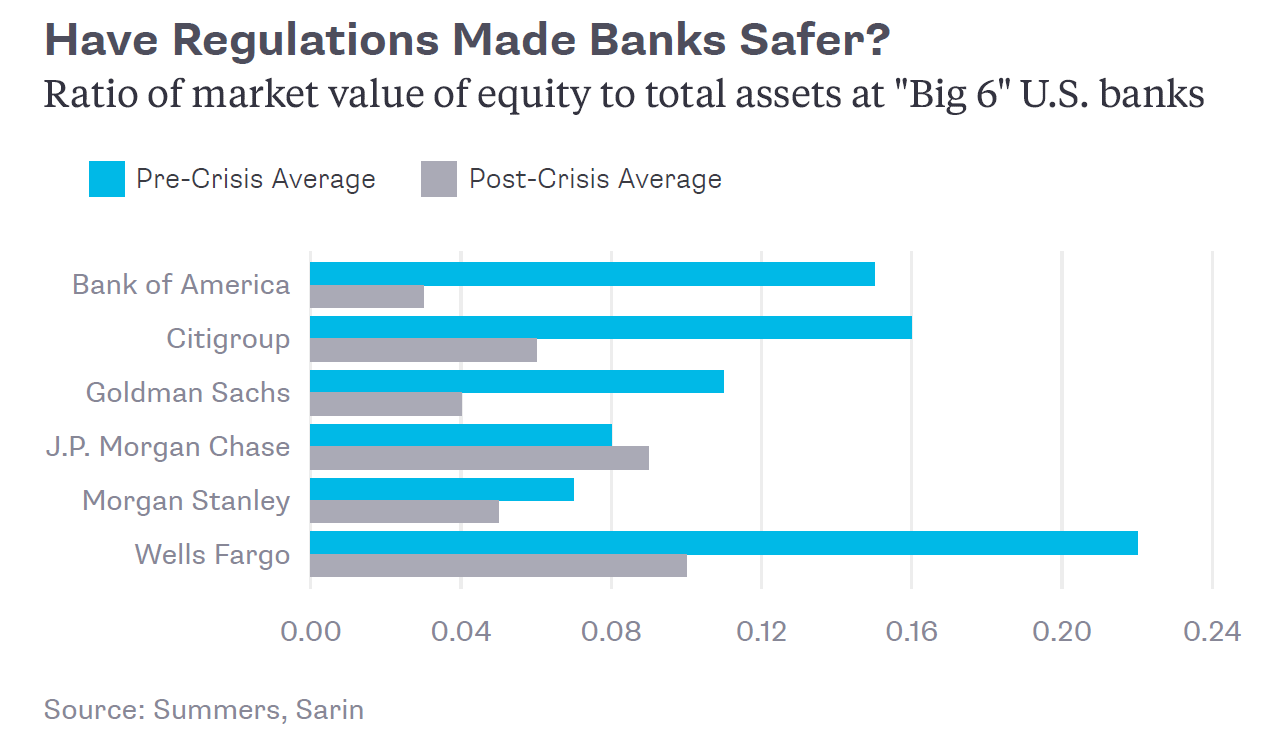

- The ratio of the market value of equity to bank assets at the major banks, Bank of America (NYSE:BAC), Citigroup (NYSE:C), Goldman Sachs (NYSE:GS), JP Morgan Chase (NYSE:JPM), Morgan Stanley (NYSE:MS), and Wells Fargo (NYSE:WFC), have fallen dramatically as demonstrated by the graph below.

- Forward-looking measures of the relative volatility of bank equity embedded in options prices.

- The evolution of the bank's equity betas since the crisis.

- The riskiness of bank wholesale secondary market liabilities, as measured by credit default swap spreads.

- PE ratios.

- Preferred stock prices and yields.

Safer and Summers find that all these measures provide evidence that every form of claim on bank assets and income is riskier relative to market measures of performance now than during the period preceding the crisis.

- Regulations have cut the banks off from their pursuit of the technologically inevitable course of future finance - servicing of the needs of corporations that are moving away from primary financing toward secondary financing. Though discouraging asset-lite activities such as primary market issuance, secondary market trading, and merchant banking; regulators have sent banking back to an obsolete past.

- Regulators are denying the banks the ability to adapt to the changing structure of non-bank corporate risk-taking: more smaller and newer ventures; fewer bigger established ventures.

Big banks and their big customers begin to look more and more like dinosaurs.

0 comments:

Publicar un comentario