The fall in interest rates

Low pressure

Interest rates are persistently low. In our first article we ask who or what is to blame. In the second we look at one outcome: a looming pensions crisis

.

THE story of rich-world central banks and their protracted entanglement with near-zero interest rates was given another twist this week. One of their number gamely announced it still hoped for a more distant relationship, even if it couldn’t bring itself to turn its back on them yet. Another renewed its vows to stick with them.

On September 21st the Federal Reserve kept its target for overnight interest rates at 0.25-0.5% but indicated that, after raising the target for the first time in a decade last year, it hoped to raise it for a second time soon—possibly in December, after America’s presidential elections. Its rate-setting committee said the case for an increase had “strengthened” since its meeting in June, but it decided to wait for more convincing evidence. Earlier that day, the Bank of Japan (BoJ) said it was staying with its target of raising inflation to 2%. Indeed it went further. The bank said it would continue to buy bonds at a rate of around ¥80 trillion ($800 billion) a year, until inflation gets above 2% and stays there for a while. To help meet this “inflation-overshooting commitment”, the bank said ten-year-bond yields would remain at around zero.

The BoJ also stuck with another unorthodox policy. Along with the European Central Bank (ECB) and a handful of smaller central banks, it charges commercial banks a small fee (a negative interest rate) to hold cash reserves. This through-the-looking-glass practice has spread to capital markets. Sanofi, a French drugmaker, and Henkel, a German manufacturer of detergent, both this month issued bonds denominated in euros with a negative yield. Investors will make a guaranteed cash loss if they hold the bonds to maturity. Earlier Germany became the first euro-zone government to issue a bond that promises to pay back to investors less than the sum it raised from them. A large proportion of all rich-country sovereign bonds now have negative yields.

You can’t always get what you want

One side says it is simply the consequence of the policies pursued by the rich world’s central banks. The Fed, ECB, BoJ and Bank of England have kept overnight interest rates close to zero for much of the past decade. In addition, they have purchased vast quantities of government bonds with the express aim of driving down long-term interest rates.

It is hardly a mystery, on this view: central banks have rigged the money markets. They have been aided in this task by new regulations, written in the wake of the global financial crisis, that require banks and insurance companies to keep more of their assets in safe and liquid instruments, such as government bonds. That is helpful, say sceptics, to rich-world governments with large debts which need to keep interest costs low. But it is punishing the thrifty and those who rely on bonds for their income.

On the other side of the divide are those who argue that central banks are merely responding to underlying forces. In this view the real interest rate is decided by the balance of supply and demand for the pool of global savings. The fall in interest rates since the 1980s reflects a shift in this balance: the supply of savings has increased as demand for it has crashed. Short-term nominal interest rates are stuck at zero, or a little below, because, in the absence of inflation, real interest rates cannot fall far enough to clear the world market for savings. Far from rigging things, central banks are struggling to find ways to help the market work so that the economy can function normally. Which side is right?

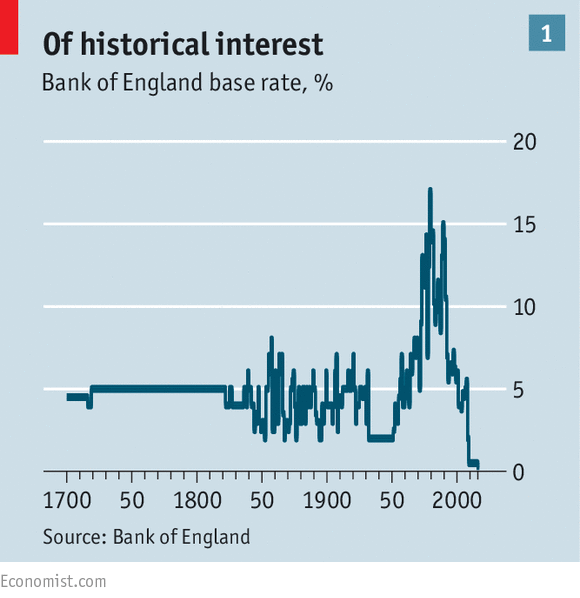

The present combination of low nominal and real interest rates is unprecedented. David Miles, a member of the Bank of England’s monetary-policy committee, has worked out that the average short-term interest rate set by the bank since 1694, when it was founded, is around 4.8% (see chart 1).

Indeed, for over a century after 1719, the bank kept its main interest rate at exactly 5%. But it is the real (ie, inflation-adjusted) rate that keeps the demand and supply of savings in balance.

.

If savers believe inflation will rise, they will demand a higher nominal interest rate to compensate for the expected loss of spending power. Borrowers, by contrast, will be keen to take on debt if they believe they can pay it back in devalued currency. Mr Miles calculates that inflation in Britain was around 2% in the three-and-a-bit centuries after 1694. That means the real interest rate was around 2.8%, assuming that inflation lived up (or down) to expectations.

That is a bold assumption. Thankfully, these days it is possible to work out long-term interest rates in real terms from the yields on inflation-protected bonds. Mervyn King, a former governor of the Bank of England, and David Low of New York University have estimated a real interest rate for G7 countries, excluding Italy, using such data going back to the mid-1980s. It shows a steady decline over the past 20 years. This era of falling real rates might usefully be split into two distinct periods: before and after the financial crisis of 2008-09. In the first period, real rates fell from above 4% to around 2%. Since the start of 2008, real long-term rates have fallen further, and faster, to around -0.5% (see chart 2).

.

Down, down, deeper and down

This ongoing glut in savings is due to two factors in particular, according to last year’s Geneva Report, an annual study from the International Centre for Monetary and Banking Studies and the Centre for Economic Policy Research. The first is changing demography, mostly in the rich world but also in some emerging markets. Populations are ageing. At the same time, the average working life has not changed much. So more money has to be squirrelled away to pay for a longer retirement. A lot of that saving takes place during the best-paid years in middle age. The size of the world population (excluding China) of peak-earning age (40-64) was rising over the past two decades relative to those of retirement age. As a consequence of this, saving increased and real interest rates have steadily fallen.

A second, related, factor is the integration of China into the world economy. “A billion people with a 40% savings rate; that brings a lot more supply to the table,” says Randall Kroszner of the University of Chicago’s Booth business school, one of the authors of the Geneva Report and a former Fed governor. Even though a massive slug of its GDP goes on investment, China still has savings left over to send abroad. That is why Mr Bernanke also blamed the saving glut for America’s current-account deficit: if China saved a lot, every one else must save less.

Explanations for its unusually high savings pile are also in part demographic. In the absence of a broad-based pension system, the family is the main social safety net. But family networks are a weak form of insurance because of China’s one-child policy. So working people have had to save furiously.

Ageing is not the only long-run influence that has tilted the savings-investment scales. By skewing income to the high-saving rich, an increase in income inequality within countries has added to the saving glut. A fall in the relative price of capital goods means fewer savings are needed for a given level of investment. Both trends predate the fall in real interest rates, however, which suggests they did not play as significant a role as demography or China.

Others reckon the drop in real interest rates reflects a shift down in underlying trend growth, both before and since the crisis. For Larry Summers of Harvard University, this “secular stagnation” is a consequence of a chronic shortfall in demand. Robert Gordon of Northwestern University reckons the trouble lies with the economy’s supply-side. The new digital and robot technologies cannot match the surge of productivity from past inventions such as electricity, the motor car, petrochemicals and indoor plumbing, he argues.

In fact, the historical relationship between real interest rates and economic growth is weak, according to a recent study by James Hamilton of the University of California at San Diego, and his co-authors. They find that the correlation between GDP growth and the real short-term interest rate across the seven most recent economic cycles in America was only mildly positive—and then only if the brief recovery before the second dip of the early 1980s “double-dip” recession is excluded. Include it and the correlation is negative (see chart 3).

..

In the period since the financial crisis, real rates have fallen even faster. The same secular forces have been at work, plus some new ones—notably “deleveraging”. Though middle-aged households were saving hard in the run-up to the crisis, many younger ones were piling on debts to buy overpriced homes. When house prices and incomes started to fall, those mortgage debts loomed much larger and so they saved more.

A related reason for more saving is fear. The severity of the Great Recession belied the relative economic stability that preceded it. Mr Miles calculates that the probability of a decline in British output as sharp as that in 2009 was 0.0004% (or one in 240,000 years) based on the volatility of GDP growth between 1949 and 2006. As people become aware of the possibility of such rare events, their caution could cut the risk-free real interest rate by 1.5-2 percentage points on plausible assumptions.

Low rider

Their defenders say central banks are typically reacting to economic trends, not shaping them.

A lodestar for central-bank policy is the idea of the “neutral” real interest rate, a close cousin of the real rate determined in the market for long-term savings. This is the short-term real interest rate that keeps inflation stable when the economy is running at full capacity, with no idle workers, factories or offices.

When inflation is low and the economy weak, as has been the case since 2008, central banks should aim to set nominal interest rates below the sum of the neutral real rate and the inflation target. The higher propensity to save means the neutral real rate is lower—probably much lower—than in the past. Since short-term nominal interest rates cannot be pushed much below zero, central banks have resorted to bond purchases to depress long-term borrowing rates and push investors into riskier assets, to give a fillip to the economy. And if interest rates and bond yields were really too low, it should lead to overheating and rising inflation. There are no signs of this.

Even so, something is amiss in bond markets when many rich-country government bonds have a negative yield and firms can sell debt by promising to pay back less than they borrow. This might be fitting if economies were in a deflationary spiral. But GDP growth is not collapsing.

Inflation is low, but is in general moving sideways, not downwards. Big budget deficits in many rich countries mean the supply of new government debt is hardly drying up.

Free falling

What is more, the impact of ever-lower rates may be starting to pall. In principle, cuts in interest rates boost the economy by nudging consumers and companies to spend now and save later. But there are forces working in the other direction, too. If savers have a target level of savings in mind to fund retirement, low or negative interest rates slow down the progress in reaching their goals. For such people, low rates mean less spending now, not more. Similarly, a low risk-free rate of interest drives up the present value of future pension obligations for employers who have promised their workers a defined benefit on their retirement.

Such firms may find that the profits they are obliged to set aside to fill the growing holes in their pension funds leave them little left over for investment. They could of course borrow but the magnitude of some pension deficits means that lenders might view such firms as a poor credit risk. It is likely that in the tug-of-war between the parts of the economy that are induced to spend now and save later by low rates, and those that are spurred to do the opposite, the former is stronger. But with risk-free interest rates at such low levels for such a long time, the fight is probably far less one-sided than in normal times.

Indeed attempts to guard against the impact of low rates may perversely become a cause of even lower rates. Accounting rules and solvency regulations are a spur to bond-buying even at super-low interest rates. To understand why, consider the business of life-assurance companies.

They pledge to pay a stream of cash to policyholders, often for decades. This promise can be likened to issuing a bond. Insurance firms need to back up these promises. To do so they buy safe assets, such as government bonds.

The trouble is that the maturities on these bonds are shorter than the promises the insurers have made. In the jargon, there is a “duration mismatch”. When bond yields fall, say because of central-bank purchases, the cost of the promises made by insurance companies goes up. The prices of their assets go up as well, but the liability side of the scales is generally weightier (see chart 4). And it gets heavier as interest rates fall. That creates a perverse effect. As bond prices rise (and yields fall), it increases the thirst for bonds. Low rates beget low rates.

.

This dynamic might materially affect bond yields if the weight of forced buyers were large enough. In 2014-15 yields on ten-year German bonds fell from around 2% to a low of close to zero, in response to expectations of quantitative easing by the ECB. A study by Dietrich Domanski, Hyun Song Shin and Vladyslav Sushko of the Bank of International Settlements finds that the fall in yields induced German insurers to buy more bonds. Insurers started 2014 with €60 billion-worth of government bonds but ended it holding €80 billion-worth.

Such a rapid rate of government-bond purchases was out of keeping with previous years. Long-maturity bonds were particularly sought after. This episode lends support to the idea that demand for bonds increases even as their price rises, where there is a mismatch of assets and liabilities. Those who worry that central-bank actions have led to distortions in capital markets seem to have a point.

If a growing bulge of middle-aged workers is behind the secular decline in real interest rates, then the downward pressure ought to attenuate as those workers move into retirement. Japan is further along this road than other rich countries. Yet its long-term real interest rates are firmly negative. That owes at least something to the open-ended quantitative easing by the Bank of Japan. A concern is that as more people retire, and save less, there will be fewer buyers for government bonds, of which less than 10% are held outside Japan. Another of the Geneva Report’s authors, Takatoshi Ito of Columbia University, reckons there will be a sharp rise in Japanese bond yields within the next decade. There may be political pressure on the Bank of Japan to keep buying bonds to prevent this.

Slip sliding away

But a lesson from the 1980s is that inflation expectations can take a long time to adjust fully to a new target. Each new round of central-bank action seems to bring less stimulus and more side-effects. The concept of using fiscal policy to fine-tune the economy went out of style around the time when economists were trying to work out why real interest rates were unusually high.

Perhaps it is time to dust that idea down.

0 comments:

Publicar un comentario