Why Gold Will Underperform For Another 40 Years Without Stagflation, Despite Central Bank, ETF, China And India Tailwinds

by: Tariq Dennison

- Gold has underperformed major asset classes over most of the past 80 years for reasons that are unlikely to change anytime soon.

- Recent drivers for gold appreciation include G7 central bank activity, ETF flows, China and India, which are unlikely to drive future long-term outperformance.

- Gold mining stocks performance has been loosely related to gold, but with greater volatility and company-specific risk.

- Gold needs stagflation to outperform. Money printing has yet to spark inflation, while technology and real assets continue to produce positive real returns.

- Recent drivers for gold appreciation include G7 central bank activity, ETF flows, China and India, which are unlikely to drive future long-term outperformance.

- Gold mining stocks performance has been loosely related to gold, but with greater volatility and company-specific risk.

- Gold needs stagflation to outperform. Money printing has yet to spark inflation, while technology and real assets continue to produce positive real returns.

Past performance is supposed to be no indication of future results, but when an asset class has a long consistent history of underperformance or outperformance, I like to know why. Gold is considered an inert metal, chemically but also economically, and while it may outperform nominal GDP growth for maybe a decade or so, any long-run rise in the price of gold will be closer to the rate of inflation as the supply of paper currency increases vs. the relatively fixed total supply of gold. The past decade has provided gold with three additional tailwinds that are unlikely to provide much additional upside in coming decades: lax central bank policy, demand from India and China, and ETF allocations.

An 80-year History of Gold Performance

An 80-year History of Gold Performance

For the past 40+ years, gold has underperformed stocks, real estate, and even bonds on many metrics.

For Americans, this 40-year period was preceded by another 40 years when it was illegal for US citizens to own gold, but fortunately for them, gold also underperformed in those four decades as well. When the Gold Reserve Act outlawed American ownership of gold 1934, gold was confiscated from individuals at $20.67/oz to be immediately revalued at $35/oz, where it remained until Nixon halted foreign conversions of the dollar to gold in 1971. Following this "Nixon shock," gold quickly and steadily rose to $192/oz in late 1974 before declining back to around $100/oz in the late summer of 1976. If an investor had instead taken the $20.67 in 1934 and invested it in the Dow Jones Industrial average, this amount would have still grown to over $800 by late 1974, even after the 2-year ~40% bear market of 1972-1974. In percentage terms, the 40-year difference between the 1934 official rate and the 1974 high works out to an average gold appreciate (or dollar depreciation) of about 5.7% per year compared with an average total return of 9.4% for the Dow stocks.

For Americans, this 40-year period was preceded by another 40 years when it was illegal for US citizens to own gold, but fortunately for them, gold also underperformed in those four decades as well. When the Gold Reserve Act outlawed American ownership of gold 1934, gold was confiscated from individuals at $20.67/oz to be immediately revalued at $35/oz, where it remained until Nixon halted foreign conversions of the dollar to gold in 1971. Following this "Nixon shock," gold quickly and steadily rose to $192/oz in late 1974 before declining back to around $100/oz in the late summer of 1976. If an investor had instead taken the $20.67 in 1934 and invested it in the Dow Jones Industrial average, this amount would have still grown to over $800 by late 1974, even after the 2-year ~40% bear market of 1972-1974. In percentage terms, the 40-year difference between the 1934 official rate and the 1974 high works out to an average gold appreciate (or dollar depreciation) of about 5.7% per year compared with an average total return of 9.4% for the Dow stocks.

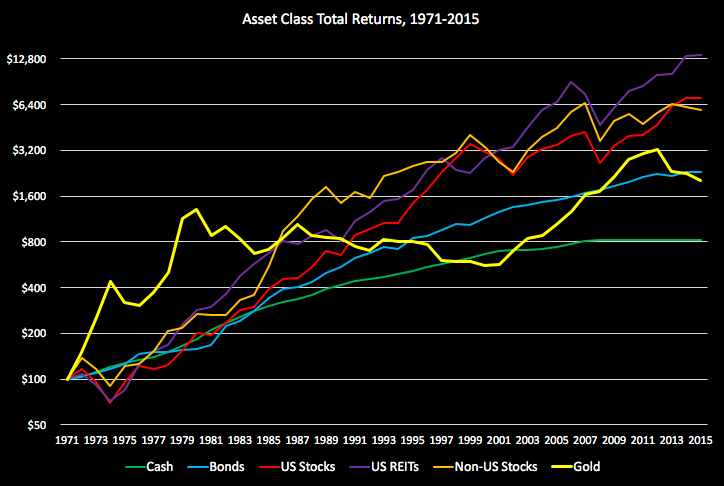

In the 40 years since, gold has appreciated from the $100-200/oz range in the mid 1970s to reach a high of almost $1,900/oz before falling back to the $1,000-1,500/oz range it has traded within for the past 3 years. During the same period, according to data from BullionVault.com whose name implies a bias towards making gold seem like a better investment), US real estate returned an average of 12% per year compared with 11.4% for stocks, 7.5% for bonds and 5.4% for gold. These lower returns for gold also came with far higher risk, with average annual swings in gold prices being 1.5x those of stocks and 2.5x those of bonds. In other words, gold has delivered lower returns with higher risk than these other major asset classes:

Chart 1: Asset Class Returns 1971-2015

Gold Returns: Interest and Capital Gains

Real estate agents make the supply and demand argument that property prices will always rise in the long term because "we're not making any more land." As a resident of Hong Kong, I am of course aware that 6% of Hong Kong territory is reclaimed land, with the current coastline of Central a good 5-10 minute walk away from its 1840 coastline. Of course, "making" land like this makes economic sense in a place where buildings soar above 30 stories high and sell for over US$2,000 per square foot, but in most other property markets, it is practical to treat land as a "fixed supply" asset.

On gold, the stickiest quote I remember from my commodity professor Jonathan Berk is that "Gold is the only commodity the world will never run out of." Gold is like other commodities that miners pull out of the ground, but unlike other metals that get used or oil that gets burned, gold is mostly just cleaned up, shaped into bars, coins or jewelry, and then put right back into the ground (often in a bank vault or basement safe). Of the commodities, this makes it most similar to land in having a "fixed supply," at least until nuclear engineers make it economically feasible to fission off three protons from a mass of lead atoms as alchemists have been trying to do for centuries before they even figured out the structure of element 79.

Unlike land, you cannot grow anything on gold, nor can you earn any income from tenants living on your gold. At best, gold could be lent out at interest like any other currency, but these rates are typically at or near zero for secured or AAA-rated borrowers (the best indicator was the "gold forward" or "GOFO" rate, which was a USD interest rate vs. gold collateral discontinued in January 2015, a chart of which can be viewed here.

A more promising trend is the issuance of gold-denominated bonds. The first I am aware of is the 5-year 0.5% bond issued by RandGold in South Africa, which could be purchased and redeemed in physical Krugerrands. On an even bigger scale, India recently finished issuing its fourth series of gold-denominated bonds with a sovereign guarantee, 8-year term, 2.75% interest rate in gold, and in this latest series, a capital gains tax exemption. In some ways, these gold-denominated bonds in India are similar to the inflation-indexed units of account used in Latin America (for example, the UDI in Mexico or the UF in Chile), which are basically inflation-indexed pesos which have historically had a real interest rate around +2%. Indians have traditionally entrusted a good share of their savings in gold, as will be discussed as a tailwind below.

For most investors outside of India, the main choices are to either hold physical gold (with all the associated costs and risks) or to invest in a gold ETF, the largest and best known of which is the SPDR Gold Shares (NYSEARCA: GLD). As of August 2016, GLD holds about 960 tonnes of physical gold, about 0.5% of the ~186,700 tonne global supply, but is unable to lend out this gold at interest and so must sell off about 0.4% of the ETF's holdings annually to cover its costs. This may seem worth it for the security and physical administration of an ancient valuable, but paying for vaults, armored trucks and security guards is easily less productive to the economy than paying farmers to harvest land, contractors to improve buildings, or almost any other kind of employee to operate a business that produces something. This may or may not be why US taxpayers are taxed 8 percentage points higher (28% vs. 20%, plus 3.8% healthcare tax) on capital gains from gold held physically or in ETFs.

One of the most common investment cases made for gold is that it is a hedge against inflation as something that holds a fixed percentage of the world's value, unlike the dollar, euro, or yen whose supply can keep increasing as central banks print more of them. Many have criticize the capital gains tax on gold as limiting citizens' freedom to protect their savings from dollar devaluation, although if they were so confident, they would be borrowing dollars at these low rates and buy more gold so that the total gains could more than pay the taxes. The idea of low rates of course is to encourage investors to borrow to invest in more productive assets and businesses, and those investors are likely to continue outperforming gold buyers in the long run by the amount those assets and businesses produce, minus any interest the gold investors can earn on their gold.

Gold's Latest Tailwinds: G7 Central Banks, India, China, and ETFs

Gold's Latest Tailwinds: G7 Central Banks, India, China, and ETFs

Over the past decade or so, three new factors have provided a boost in the demand for gold which helped drive its increase from below US$500/oz in 2005 to an average of over $1,600 in 2012 and over $1,100 in 2015. The factors are: 1.) rising demand from India and China, 2.) launch and growth of GLD and other gold ETFs like the iShares Gold Trust (NYSEARCA:IAU) starting around 2004, and 3.) zero and negative interest rate policies of G7 central banks since the global financial crisis in 2008.

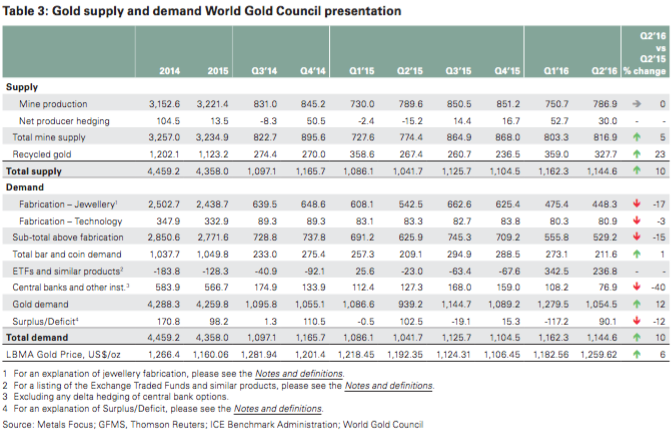

First of all, the biggest base of demand for gold is neither central banks nor big funds, but rather consumer demand in the form of jewelry, coins, and bars, especially from India and China, as shown by charts 2 and 3:

Chart 2: Global Gold Supply and Demand by Type, 2015 and 2016

Chart 3: Gold Demand vs. Supply by Country

Chart 4: GDP of China and India vs. other countries, 2015 vs. 2030

Source: Bloomberg

Source: Bloomberg

It is worth noting that while India's annual demand for gold has increased by around 50% over the last 10 years, China's demand for gold roughly quadrupled over the same decade. This helps explain why jewelers that sell (and buy) large volumes of gold in greater China have performed well over this period, but with more volatility since gold's latest peak in 2011. The below chart compares GLD with Chow Sang Sang (SEHK: 0116 / US Pink Sheets: OTC:CHOWF) since 2004, as well as against the world's largest jeweler Chow Tai Fook (SEHK: 1929 / US Pink Sheets: OTCPK:CJEWF). Chow Tai Fook is about 5 times larger than Chow Sang Sang by market cap, but the former is more diversified into transportation and other sectors while the latter is more of a pure play on China jewelry.

Chart 5: 12-year performance of Gold vs. a sample Jeweler, 2004-2016

Source: Google Finance

Source: Google Finance

In India and China, gold jewelry is not solely decorative, but continues to serve a physical store-of-value and transfer-of-value function that Indian and Chinese institutions are not yet trusted enough to fully provide. Unlike the 10, 14 or 18 karat gold (representing 41.7%, 58.5% and 75% gold purity respectively) acceptable in most American jewelry, Indian gold jewelry is typically 22 karat (91.6% purity), while Chinese buyers prefer 24 karat (99.9%). Retail jewelers post the prices at which they buy back gold while often separate out charges for any design or workmanship. On the innocent side, savers in both countries have real reasons to fear keeping all of their money in a bank or other financial institution within borders long known to impose capital controls and hide statistics on non-performing loans. On the more nefarious side, physical gold is still a relatively efficient tool for tax evasion and money laundering. My view on India and China is that I would prefer to invest in them by investing in assets and businesses harvesting high yields from their growth and economic development rather than to try and speculate on whether I can sell my gold at a higher price in those countries many years from now.

Second, and somewhat correlated to India and China demand, has been the launch and growth of gold ETFs as an asset class. GLD is only the largest and best known gold fund holding just less than half of the roughly 2,200 tonnes held by ETFs globally. This total amount held by ETFs represents just over 1% of the known gold in the world, and is roughly equal to annual consumer demand of only India, China and the Middle East in the year 2015. While allocations to these ETFs still have room to grow, both from an increasing pool of global investment capital and from existing capital opening up to maturing gold ETFs; these ETFs are competing with an ever-widening menu of other asset classes and ETFs.

I visualize this by imagining the conservative Indian or Chinese saver who so far has kept a large portion of their savings in physical gold (or physical property) due to mistrust of their country's financial systems so far. When this saver eventually builds the confidence to start allocating a significant share to ETFs, what are the chances of choosing a gold ETF over a dozen other ETFs which could offer diversified exposure to foreign markets, technology, and other strategies, often while paying a dividend?

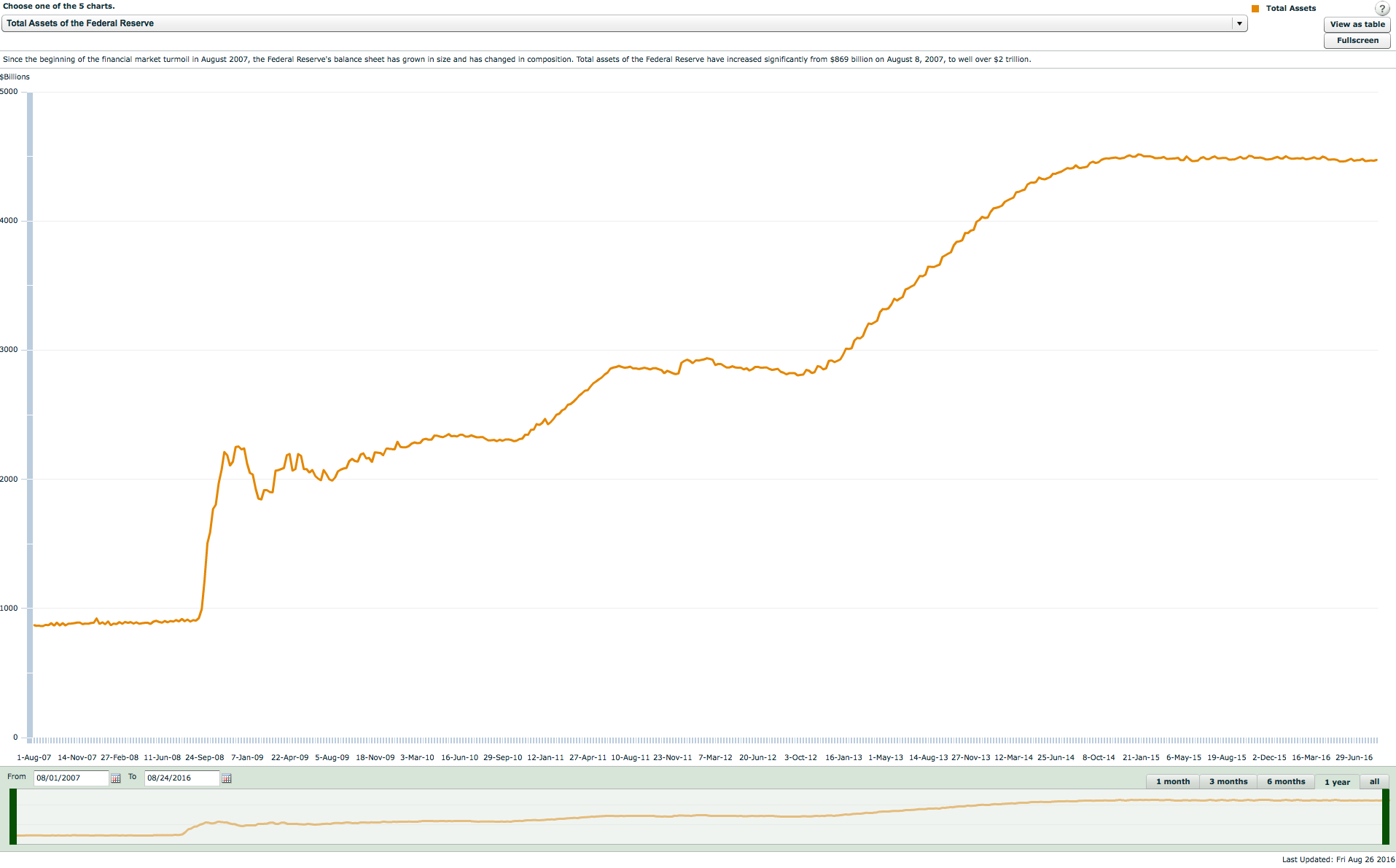

Last, but certainly not least, is the supposed bull case for gold due to lax monetary policy by G7 central banks since the 2008 global financial crisis. Gold bugs may point to a chart like the one below showing the unsustainable expansion of the US Federal Reserve's (and similarly, the European Central Bank's and Bank of Japan's) balance sheet as these currency issuers pumped the world with cheap money through zero (and negative) short-term interest rates and quantitative easing that pushed long-term bond yields in Japan, Switzerland, and the Eurozone below zero. While the Fed's balance sheet has ballooned to about 5 times its pre-2008 size, this has so far only translated to about a 2.5x increase in M1 money supply, and so far has failed to even get inflation up to the 2% levels targeted by central bankers, let alone levels that would get gold bulls excited about hyperinflation.

Chart 6: Fed Balance Sheet

Source: Federal Reserve

Source: Federal Reserve

One benchmark to look at are the yields on Treasury Inflation Protected Securities [TIPS], which currently offer a 10-year real yield around 0% compared with a yield on 10-year US Treasuries of 1.5%. This implies a market expectation of 1.5% inflation per year over the next 10 years in the US, with real interest rates at zero and even lower expectations for Japan and Europe. As much as 20th century economics students might look at what these central banks are doing and fear their policies would lead to inflation, for the past 8 years the problem has been that the money printers have been unable to get inflation up to even a healthy level, let alone a high level. Yellen, Draghi and Kuroda could only wish inflation would start rising to levels that would justify rate hikes to keep inflation in check and return to the familiar and normal economics of their textbooks. That said, I also look back at times where inflation was high, and find that other real assets like land, physical property and REITs, often did at least as well as gold and often better with the benefits of having a positive yield, currently around +2-6% for many real estate assets.

A textbook explanation of inflation is when "too many dollars are chasing too few goods." The lack of inflation despite there being "too many dollars" over the past decade may be explained as "too many dollars chasing too many goods."

A Quick Note on Gold vs. Gold Mining Stocks

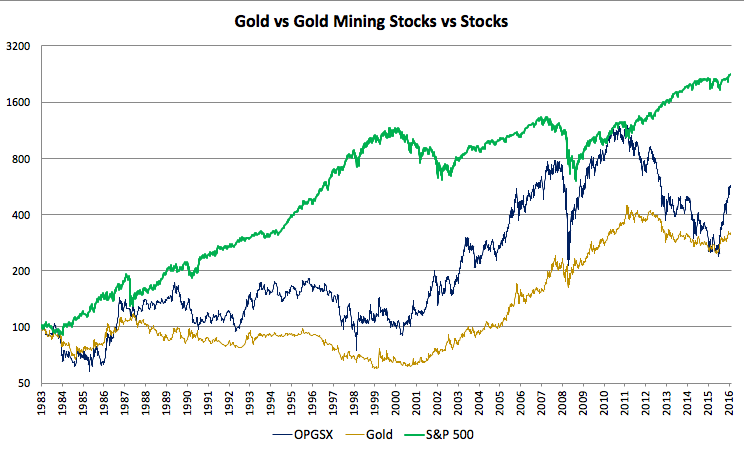

In the decades before GLD made owning gold easy, one of the most common ways for investors to get exposure to gold in their investment accounts was to buy shares of gold mining stocks, especially those of companies which did not hedge their exposure to gold prices. Some investors still prefer this method, with just one vehicle being the VanEck Vectors Gold Miners ETF (NYSEARCA:GDX) with US$10 billion under management. An older fund is the Oppenheimer Gold & Special Minerals Fund (MUTF:OPGSX) on which the below chart compares total returns back to 1983 vs. Gold and the S&P 500 stock index.

Chart 7: Gold vs. Miners

Source: Yahoo Finance

Source: Yahoo Finance

From the chart, it seems that gold mining stocks did provide a somewhat levered exposure to gold prices, with somewhat higher returns and significantly higher volatility. The diversified S&P 500 stock index on the other hand steadily produced higher returns with less volatility over most of the same period, with the major bear markets in 2000-2002 and 2008-2009 being the two times gold outperformed stocks.

While ordinarily I would prefer investing in the stocks of an operating business over an inactive metal, gold mining is a tough business that I admit I do not understand very well, which seems to have high risks and high competition without the benefits of cheap valuations or attractive dividends.

To track a basket of gold mining stocks that do pay dividends, I created a basket on the Motif Investing platform of some of the top dividend paying gold miners, whose dividend yields are still relatively low compared with other sectors.

Investing in gold mining stocks is most suitable to investors interested in understanding company-specific and mine-specific details of these stocks and finding opportunities with significant cost advantages, underpriced reserves, or other sources of alpha where the company could outperform with the gold price risk hedged out.

Conclusion

Over the past 80 years, gold has been a relatively poor investment compared with stocks, bonds, or real estate, especially on a risk-adjusted basis. The increase in the price of gold over the past 10-15 years seems to have been largely driven by the three tailwinds of India/China demand, ETF allocation, and money printing by central banks, but even then this has not been enough to help gold catch up with the performance of the other "living, yielding asset classes."

Over the next 10-15 years, these tailwinds are likely to get even weaker as China and India see better alternatives to allocate savings to, ETF growth levels off, and central bank activities normalize.

What might change all this and lead a scenario where gold might be one of the best performing assets over the coming decades? In a word, what gold would need is stagflation - inflation rising to not just healthy but high levels, coinciding with year after year of decline in the real economy. Even in a stagflation scenario, the real estate assets often rise in value with inflation while also providing a positive real yield. In the short-term, gold can outperform real estate if several years' worth of inflation fears are rapidly priced into it, which is why gold is a volatile asset that is dangerous to buy high. Long term, gold can outperform real estate only if the yield from lending out the former exceeds the real yield from harvesting or renting out the latter.

0 comments:

Publicar un comentario