This Is The Reason Gold Dropped On Friday And Here's What Investors Should Do About It

by: Hebba Investments

- Speculative traders increase their positions to close to record highs on anticipated Fed dovishness.

- Recent Fed speak has been pretty hawkish and we believe that the Fed will raise rates in September.

- This is further supported by a surprise Fed speech on Monday that seemed to cause markets to drop.

- While the picture is bearish short term for gold, we think fiscal stimulus and much higher gold prices are on the way.

- Recent Fed speak has been pretty hawkish and we believe that the Fed will raise rates in September.

- This is further supported by a surprise Fed speech on Monday that seemed to cause markets to drop.

- While the picture is bearish short term for gold, we think fiscal stimulus and much higher gold prices are on the way.

The Latest COT Report Shows Traders…

The latest COT report showed a massive build in speculative long positions as traders seemed to think that the weak data is not going to be strong enough to allow the Fed to hike rates when they meet in a few weeks. Much of this speculative build may have been reversed by Friday as traders started to once again change positions on a possible Fed hike based on the recent "Fed speak" and a previously unannounced speech by the central bank's most dovish official, Governor Lael Brainard.

Regardless, as of the Tuesday COT report close, we are again approaching all-time record levels of net long speculators in gold. We will give our view and will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it. What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

This week's report showed a massive increase in speculative gold longs and a good-sized decrease in speculative shorts with longs increasing by 31,805 contracts and shorts closing out 9,037 contracts on the week. Investors should note that the COT report's close is Tuesday, so this data doesn't include the late week swoon in gold which caused the metal to drop slightly on the week despite the strong Monday open.

One thing that is interesting is despite the 40,000 contract increase in the net speculative position, gold was only able to muster a 1.45% gain for the week. We would have expected a bit more of a gain in gold based on that sort of build in net longs - which tells us that other gold players (think physical gold holders and Eastern retail buyers) aren't as bullish.

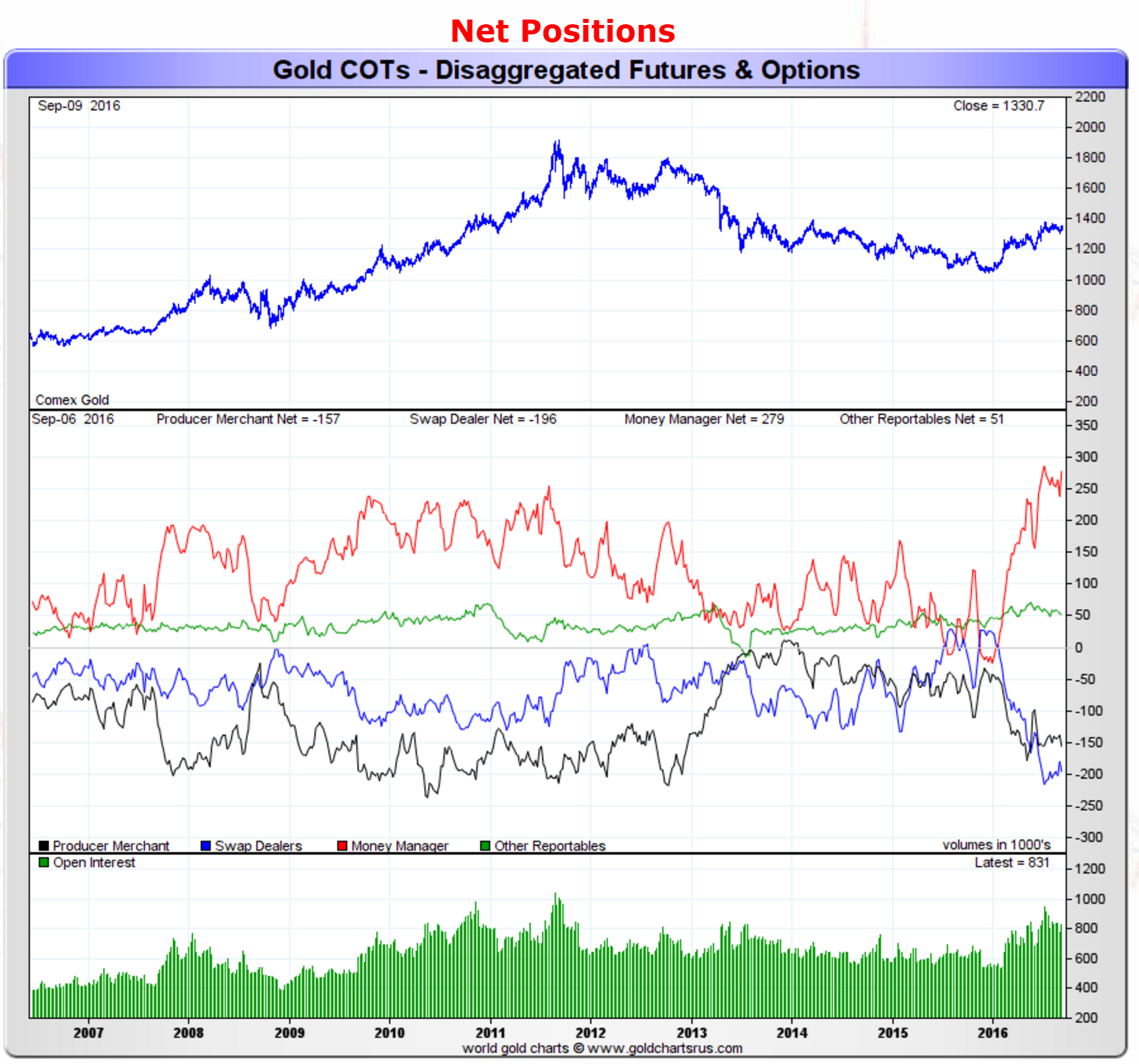

Moving on, the net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, speculative traders whom have pulled back over the past few weeks significantly increased their positions back close to all-time high levels. Currently, those positions sit at a net long position of around 279,000 contracts - only a stone-throw's away from the all-time high seen in early July.

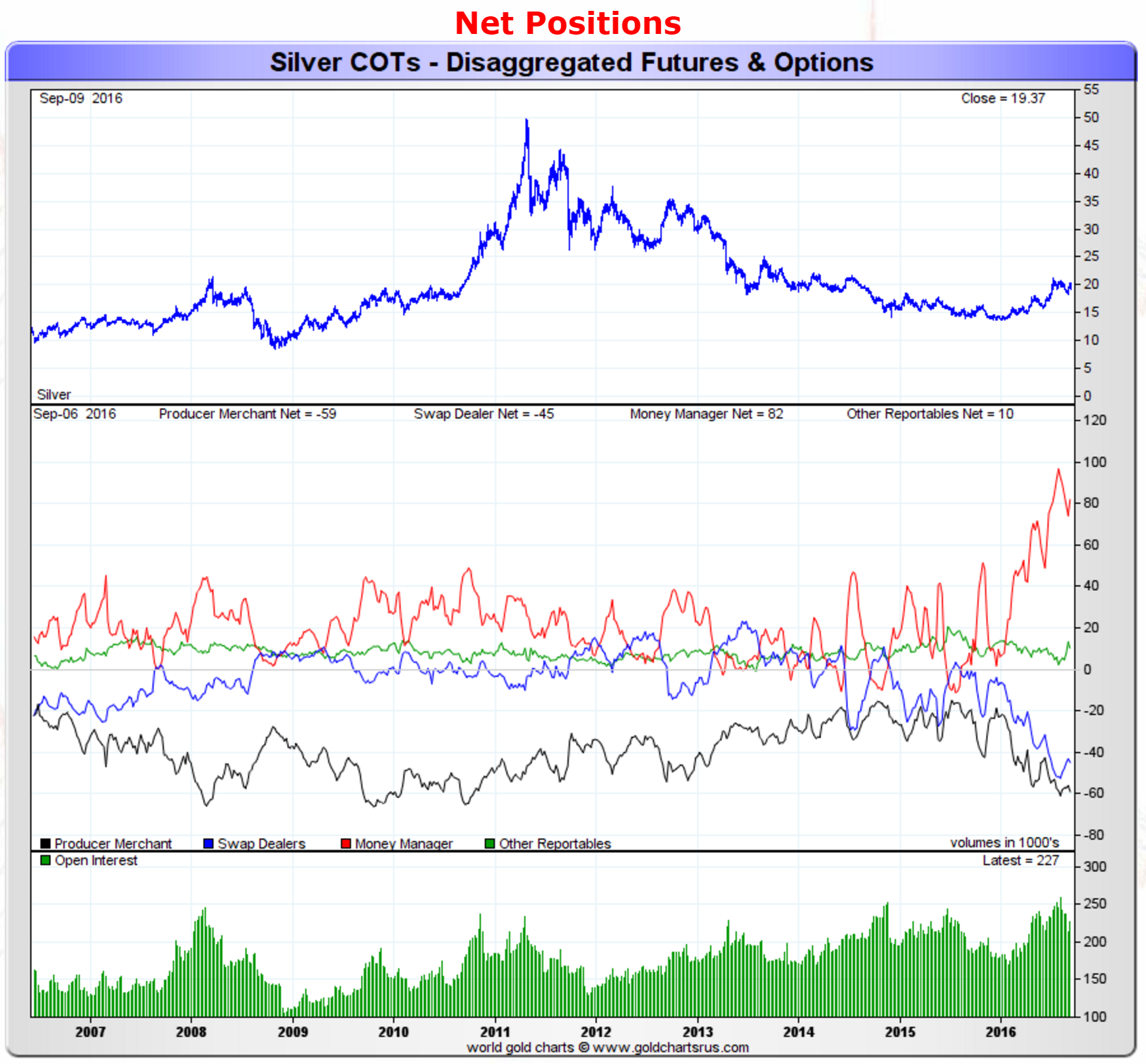

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red line which represents the net speculative positions of money managers, saw a slight increase similar to gold but it was clearly not as large of a rise. Speculative silver traders simply weren't as bullish on silver for the week as they were gold. This may explain silver's underperformance towards the end of the week and we're very cautious on silver right now as we do see the potential for much more downside if speculative traders cannot pick up the slack for retail investors.

Friday's Market Plunge and Our Take

It seems every week there is some Federal Reserve related event that is affecting markets. Last week it was Yellen's Jackson Hole speech, this week we got some late fireworks as evidently a simple press release announcing that a Fed governor will be delivering a speech the following week is enough to spark a selloff in Treasuries, which spread to the rest of capital markets.

The unorthodox thing was that this speech was rather hastily announced the day before the Fed's pre-meeting blackout period, which seems to us a bit unusual. Additionally, since she is a noted Fed dove, the rumors were building that it was going to be more hawkish to increase market expectations of a rate hike (remember the Fed doesn't want to hike rates to an unprepared market).

Peter Hooper, chief economist at Deutsche Bank Securities, wrote a note to clients on Thursday with the following:

As a dovish member, Brainard would carry a lot of credibility delivering a more hawkish message. It could be a coincidence, but it could also be an important opportunity for the Fed to raise market expectations and give the FOMC more room to maneuver at the September meeting. After San Francisco Fed President John Williams failed to budge the market with a fairly hawkish speech Monday evening, we assumed it would likely take an interview with Yellen to turn market expectations about the September meeting around, should they seriously be considering a rate hike. Certainly a good case can be made for moving "soon" (in September) given: (1) payroll growth in recent months now averaging in excess of where the Fed wants to see it, (2) generally improving signs for consumer spending and overall GDP growth (the latest ISM notwithstanding), and (3) relatively favorable financial conditions. I had moved my odds on a September hike to the mid-40s in the wake of recent Fedspeak, but not higher because there is still some room for improvement in the inflation picture. But this development re. Brainard has to place the probability very close to 50%.

We think he's probably dead-on, and as we stated last week, we believe the Fed does want to raise interest rates in September. This part of what we believe is a significant narrative change in the way governments are going to battle this seemingly endless economic malaise around the world - less monetary stimulus (i.e. zero interest rates) and more fiscal stimulus (government spending).

The Narrative Shift

We believe the narrative is changing here as we start to see the signs of a switch in strategy by governments and central banks from monetary stimulus to fiscal stimulus. We don't think it was a surprise that the ECB let down bond markets by not announcing the need for further stimulus - it's clearly central bankers working in unison as the realization that ZIRP and NIRP are not working.

What that means for investors is that we believe rates are going to begin to rise - slightly but move up nevertheless and the Fed will probably begin the process when it meets in September.

Monday's speech by Ms. Brainard will be a key thing for investors to monitor as if she's hawkish then it's a clear signal from the Fed to markets that September is a "live" meeting and rates will probably be moving up.

Here's where it's important to note the narrative shift and see keep the big picture in mind. For the past few years markets have intensely monitored the Fed's interest rate policy as low/negative rates meant loose money, while rate tightening meant the Fed was going to be ever so slightly less accommodative. So if you've been tuned into this show over the past few years then that would be bad for gold. But here's where we believe the narrative is shifting.

While the Fed wants to raise rates, they don't believe the economy isn't very strong at all and thus if they're going to tighten money on the interest rate side there has to be a commensurate loosening somewhere else to balance or even outdo the rate increase. That "somewhere else" is fiscal policy.

As we've stated before, both presidential candidates are promising to significantly increase infrastructure spending to the tune of hundreds of billions of dollars to fight this global economic weakness. It is not just them though as economists, politicians, and governments are all signaling the need for greater fiscal stimulus and spending - the calls are getting louder and louder.

What That Means for Gold Investors

Fiscal spending is actually good for gold investors as it's a key ingredient for classic monetary inflation. While we believe we're already seeing inflation in paper asset prices, replacing monetary stimulus with fiscal stimulus will move inflation from Wall Street to Main Street as it tends to be much more widespread.

But we are not there yet - first we have to see the narrative fully change.

Right now, we believe markets (including the gold market) are fully focused on the old narrative and tightening of money via rising interest rates. Pair that with the large speculative net long position in gold and we have the potential for significant short-term weakness. But we don't believe that will last for long as markets begin to realize fiscal spending is on the way and is much more of an inflationary multiplier than a 0.25% rise in interest rates.

Based on that theory, we believe investors should expect more short-term gold weakness until the Fed makes it move in September, which we think is a likely increase in rates. But they shouldn't be completely out of gold (or worse shorting it) because we have no idea when the market will realize that fiscal stimulus is on the way - don't get stuck picking up those pennies in front the fiscal bulldozer.

So in summary, investors should keep their core positions in the gold ETF's such as the SPDR Gold Trust ETF (NYSEARCA:GLD), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), iShares Silver Trust (NYSEARCA:SLV), and miners such as Randgold (GOLD) and Barrick Gold (NYSE:ABX). Also, those investors who followed our advice and sold out of some of their gold trading positions, now would be the time to start nibbling away and buy some of the old positions back. Keep in mind we don't believe the real buying should be done until AFTER the September Fed meeting until we become more certain the Fed is going to start raising interest rates and some of the speculative traders have sold out of their record-high positions.

0 comments:

Publicar un comentario