LIBOR: A Sign Of Stress Or Something Else

by: Brad Thomas

- Short-term funding rates have been increasing for banks, making some investors nervous.

- The increase in LIBOR is not financial stress related, but the result of a regulatory change.

- Our thoughts on the situation and why it is occurring.

- The increase in LIBOR is not financial stress related, but the result of a regulatory change.

- Our thoughts on the situation and why it is occurring.

There has been a decent amount of chatter over the last few months about the rise in the London Inter-Bank Offered Rate ("LIBOR") and what it might mean for investors. While much has been said about this topic, we have fielded a number of questions regarding the move and what our thoughts are on LIBOR. We do indeed have thoughts on the subject and this article is our attempt to explain it in the best way we know how.

As usual, this story begins with regulatory changes ("we are from the government, we are here to help") and the resultant impact.

From the SEC's final rule on money market reform (17 CFR Parts 270 and 274) we get the background reason for the regulatory change (emphasis ours):

As discussed in significant detail in the Proposing Release, during 2007-2008 money market funds were exposed to substantial losses, first as a result of exposure to debt securities issued by structured investment vehicles ("SIVs"), and then as a result of the default of debt securities issued by Lehman Brothers Holdings Inc. ("Lehman Brothers"). All but one of the funds that were exposed to losses from SIV and Lehman Brothers securities obtained support of some type from their advisers or other affiliated persons, which absorbed the losses or provided a guarantee covering a sufficient amount of losses to prevent the fund from breaking the bank.

The Reserve Primary Fund, which held a $785 million position in Lehman Brothers debt, ultimately did not have a sponsor with sufficient resources to support it, and on September 16, 2008, the fund announced that it would re-price its securities at $0.97 per share. It subsequently suspended redemptions as of September 17, 2008.

The cumulative effect of these events, when combined with general turbulence in the financial markets, led to a run primarily on institutional taxable prime money market funds, which contributed to severe dislocations in short-term credit markets and strains on the businesses and institutions that obtain funding in those markets. During the week of September 15, 2008, investors withdrew approximately $300 billion from taxable prime money market funds, or 14 percent of the assets held in those funds.

The severity of the problems experienced by money market funds during 2007 and 2008 prompted us to review our regulation of money market funds. We sought to better understand how we might revise rule 2a-7 to reduce the susceptibility of money market funds to runs and reduce the consequences of a run on fund shareholders. Our staff consulted extensively with staff from other members of the President's Working Group on Financial Markets. We talked to many market participants and reviewed a report from a "Money Market Fund Working Group" assembled by the Investment Company Institute ("ICI Report"), which recommended a number of changes.

From the SEC press release:

From the Federal Register (the source of the effective and compliance dates):

The compliance date for our amendments related to liquidity fees and gates, including any related amendments to disclosure, is October 14, 2016. We are adopting a compliance period of two years for money market funds to implement the fees and gates amendments instead of the proposed one-year compliance period.

The compliance date for our amendments related to floating NAV, including any related amendments to disclosure, is October 14, 2016. We are adopting, as proposed, a compliance period of two years for money market funds to implement the floating NAV amendments.

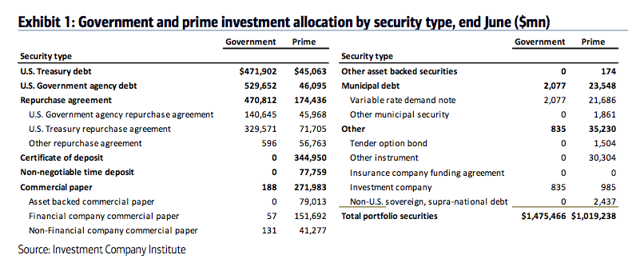

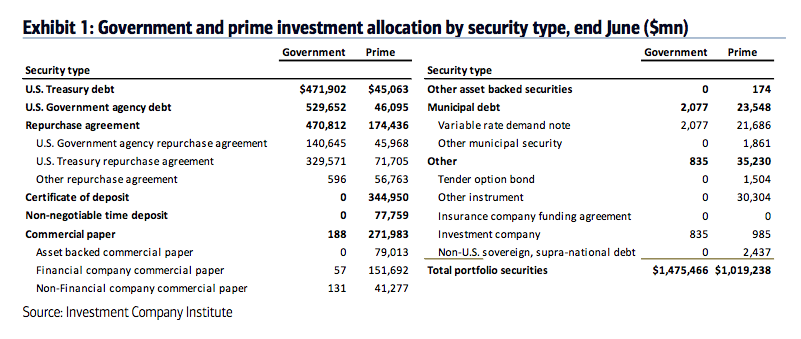

And how does this affect LIBOR, you ask? Well, let's take a peek at what these prime funds invest in:

(BAML/ICI)

(BAML/ICI)

Notice that big number next to Certificate of Deposit in the prime fund column, the $344B one?

Prime funds are a major source of funding for banks.

It might not be so bad if it were just Prime funds transitioning to a floating NAV, but think of this from an institutional investor perspective - a floating NAV increases the accounting work and potential variability of that king of all assets - cash!

As the WSJ reports:

The number of prime funds reporting is projected to decline to 264 after the changes take effect, from roughly 492 such funds a year ago, according to the money-fund research firm.

Meanwhile, the number of government funds is projected to increase to 587 as of mid-October, from about 476 such funds about a year ago.

During the 11-month-period ended July 31, assets invested in prime institutional funds have declined 35% as the new requirements have prompted many investors to shift assets into government institutional funds, which have seen assets increase by 41%, the research firm stated.

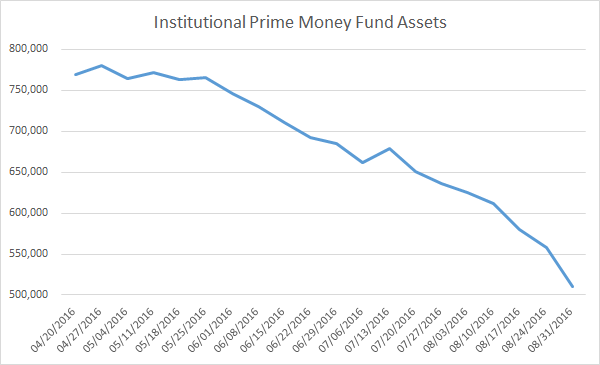

The following chart (using ICI data) shows the extent of the drop in assets:

That is $250 billion in assets in 20 weeks.

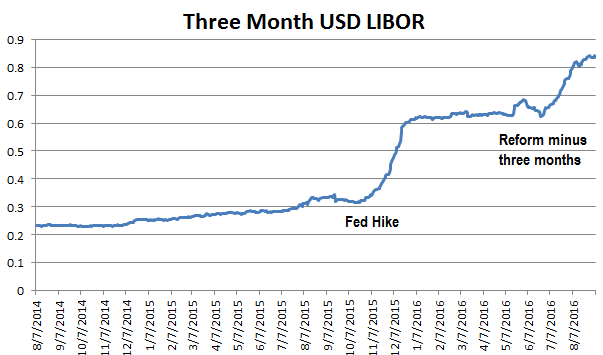

As investors withdraw money from the prime funds, the funds have to build liquidity in order to accommodate the outflows, both current outflows and the outflows expected on F-Day (yep, Floating NAV day). How do they do this? They reduce the weighted average maturity of their portfolios and do not invest much past F-Day. Recall earlier we showed the amount of money these prime funds invested in banks. This factors into the cost of bank funding - the very thing LIBOR (is supposed to) measure. This can be seen in the following chart:

Bottom Line: LIBOR has been increasing due to the lack of the prime fund bid and will not begin to trade on "true" rate fundamentals (if there is such a thing anymore) until we move past the money market reform compliance date. We caution investors not to read much more into the increase in LIBOR, as we do not believe it is a sign of financial stress (aside from the stress felt by prime fund managers and short CD/CP salesman) or weakness in the system.

In the above chart, you can see how three-month LIBOR began to increase at F-Day less three months. We are seeing the same in one-month LIBOR at this juncture, which should give floaters a couple months of decent rates (depending on resets). We do not expect LIBOR to adjust downward quickly after the 10/14/16 compliance date, but expect it to gradually revert to its "normalized" levels as funds determine their liquidity needs and are able to return to longer-term bank financing.

In the next few days we will be building on this by filtering REITs with variable rate debt in order to see who might "pay the price" of the increase in this benchmark rate.

As usual, this story begins with regulatory changes ("we are from the government, we are here to help") and the resultant impact.

From the SEC's final rule on money market reform (17 CFR Parts 270 and 274) we get the background reason for the regulatory change (emphasis ours):

As discussed in significant detail in the Proposing Release, during 2007-2008 money market funds were exposed to substantial losses, first as a result of exposure to debt securities issued by structured investment vehicles ("SIVs"), and then as a result of the default of debt securities issued by Lehman Brothers Holdings Inc. ("Lehman Brothers"). All but one of the funds that were exposed to losses from SIV and Lehman Brothers securities obtained support of some type from their advisers or other affiliated persons, which absorbed the losses or provided a guarantee covering a sufficient amount of losses to prevent the fund from breaking the bank.

The Reserve Primary Fund, which held a $785 million position in Lehman Brothers debt, ultimately did not have a sponsor with sufficient resources to support it, and on September 16, 2008, the fund announced that it would re-price its securities at $0.97 per share. It subsequently suspended redemptions as of September 17, 2008.

The cumulative effect of these events, when combined with general turbulence in the financial markets, led to a run primarily on institutional taxable prime money market funds, which contributed to severe dislocations in short-term credit markets and strains on the businesses and institutions that obtain funding in those markets. During the week of September 15, 2008, investors withdrew approximately $300 billion from taxable prime money market funds, or 14 percent of the assets held in those funds.

The severity of the problems experienced by money market funds during 2007 and 2008 prompted us to review our regulation of money market funds. We sought to better understand how we might revise rule 2a-7 to reduce the susceptibility of money market funds to runs and reduce the consequences of a run on fund shareholders. Our staff consulted extensively with staff from other members of the President's Working Group on Financial Markets. We talked to many market participants and reviewed a report from a "Money Market Fund Working Group" assembled by the Investment Company Institute ("ICI Report"), which recommended a number of changes.

From the SEC press release:

The new rules require a floating net asset value (NAV) for institutional prime money market funds, which allows the daily share prices of these funds to fluctuate along with changes in the market-based value of fund assets and provide non-government money market fund boards new tools - liquidity fees and redemption gates - to address runs.The final rules provide a two-year transition period to enable both funds and investors time to fully adjust their systems, operations and investing practices.

From the Federal Register (the source of the effective and compliance dates):

The SEC is removing the valuation exemption that permitted institutional non-government money market funds (whose investors historically have made the heaviest redemptions in times of stress) to maintain a stable net asset value per share ("NAV") and is requiring those funds to sell and redeem shares based on the current market-based value of the securities in their underlying portfolios rounded to the fourth decimal place (e.g.,$1.0000), i.e., transact at a "floating" NAV. The SEC also is adopting amendments that will give the boards of directors of money market funds new tools to stem heavy redemptions by giving them discretion to impose a liquidity fee if a fund's weekly liquidity level falls below the required regulatory threshold, and giving them discretion to suspend redemptions temporarily, i.e., to "gate" funds, under the same circumstances. These amendments will require all non-government money market funds to impose a liquidity fee if the fund's weekly liquidity level falls below a designated threshold, unless the fund's board determines that imposing such a fee is not in the best interests of the fund.Federal Register effective date: October 14, 2014.

The compliance date for our amendments related to liquidity fees and gates, including any related amendments to disclosure, is October 14, 2016. We are adopting a compliance period of two years for money market funds to implement the fees and gates amendments instead of the proposed one-year compliance period.

The compliance date for our amendments related to floating NAV, including any related amendments to disclosure, is October 14, 2016. We are adopting, as proposed, a compliance period of two years for money market funds to implement the floating NAV amendments.

And how does this affect LIBOR, you ask? Well, let's take a peek at what these prime funds invest in:

(BAML/ICI)

(BAML/ICI)Notice that big number next to Certificate of Deposit in the prime fund column, the $344B one?

Prime funds are a major source of funding for banks.

It might not be so bad if it were just Prime funds transitioning to a floating NAV, but think of this from an institutional investor perspective - a floating NAV increases the accounting work and potential variability of that king of all assets - cash!

As the WSJ reports:

The number of prime funds reporting is projected to decline to 264 after the changes take effect, from roughly 492 such funds a year ago, according to the money-fund research firm.

Meanwhile, the number of government funds is projected to increase to 587 as of mid-October, from about 476 such funds about a year ago.

During the 11-month-period ended July 31, assets invested in prime institutional funds have declined 35% as the new requirements have prompted many investors to shift assets into government institutional funds, which have seen assets increase by 41%, the research firm stated.

The following chart (using ICI data) shows the extent of the drop in assets:

That is $250 billion in assets in 20 weeks.

As investors withdraw money from the prime funds, the funds have to build liquidity in order to accommodate the outflows, both current outflows and the outflows expected on F-Day (yep, Floating NAV day). How do they do this? They reduce the weighted average maturity of their portfolios and do not invest much past F-Day. Recall earlier we showed the amount of money these prime funds invested in banks. This factors into the cost of bank funding - the very thing LIBOR (is supposed to) measure. This can be seen in the following chart:

Bottom Line: LIBOR has been increasing due to the lack of the prime fund bid and will not begin to trade on "true" rate fundamentals (if there is such a thing anymore) until we move past the money market reform compliance date. We caution investors not to read much more into the increase in LIBOR, as we do not believe it is a sign of financial stress (aside from the stress felt by prime fund managers and short CD/CP salesman) or weakness in the system.

In the above chart, you can see how three-month LIBOR began to increase at F-Day less three months. We are seeing the same in one-month LIBOR at this juncture, which should give floaters a couple months of decent rates (depending on resets). We do not expect LIBOR to adjust downward quickly after the 10/14/16 compliance date, but expect it to gradually revert to its "normalized" levels as funds determine their liquidity needs and are able to return to longer-term bank financing.

In the next few days we will be building on this by filtering REITs with variable rate debt in order to see who might "pay the price" of the increase in this benchmark rate.

0 comments:

Publicar un comentario