Witness The Butterfly Effect

by: The Heisenberg

Summary

- Look out, here comes another Heisenberg reality check.

- Behold the effect of new regulations.

- "Folks don’t always see the connection to their lives, in reality, it is so consequential".

- Behold the effect of new regulations.

- "Folks don’t always see the connection to their lives, in reality, it is so consequential".

If I could go back and give one piece of advice to the 19-year-old Heisenberg, it would be this: think about life the same way you think about investing - holistically.

I've made a lot of bad decisions in my time (judging from the rich, peaty aroma wafting up from the short glass in front of me, this Balvenie DoubleWood 12 neat isn't one of them), and owing to a seemingly ingrained sense of entitlement mixed with narcissism and a dash of arrogance, I rarely considered how my decisions affected others. That is, I didn't take a holistic approach to life and I didn't put much effort into evaluating consequences.

On the other hand, I've always thought about investing holistically; as an inextricably linked set of markets (NYSEARCA:SPY) that can only be understood by reference to an overarching interconnected liquidity regime. The speed with which money moves these days makes that conception all the more crucial.

It's with that in mind that I wanted to revisit what's going on with LIBOR, which is sitting at 7-year highs.

I've talked quite a bit about why this is the case and I encourage you to review those discussions (here and here). Deutsche Bank sums it up with three bullets:

- Prime fund outflows

- Dollar liquidity squeeze

- Fed expectations

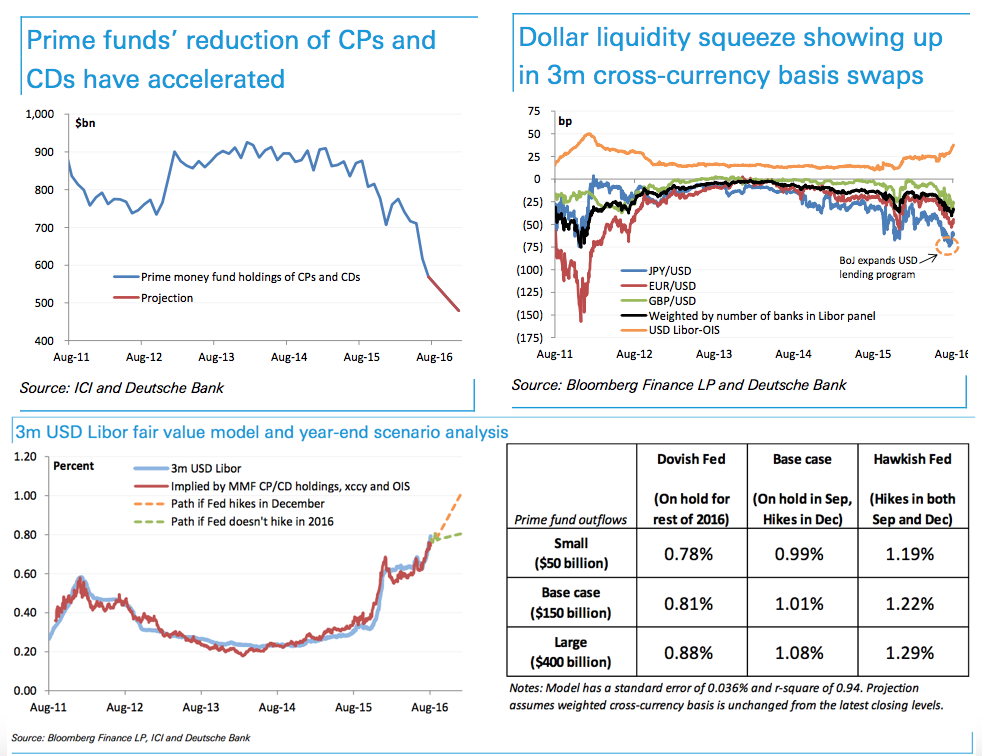

Again, I'm not going to recount the details because I've done so exhaustively in the pieces linked above, among others, but here are some visuals for you which depict prime funds reducing exposure to commercial paper, the stress in cross-currency basis swaps, the LIBOR-OIS spread, and Deutsche's LIBOR projections:

(Charts: Deutsche Bank)

(Charts: Deutsche Bank)

Now note that four out of nine of Deutsche's projections have LIBOR remaining elevated, but sticking below 1% by year-end.

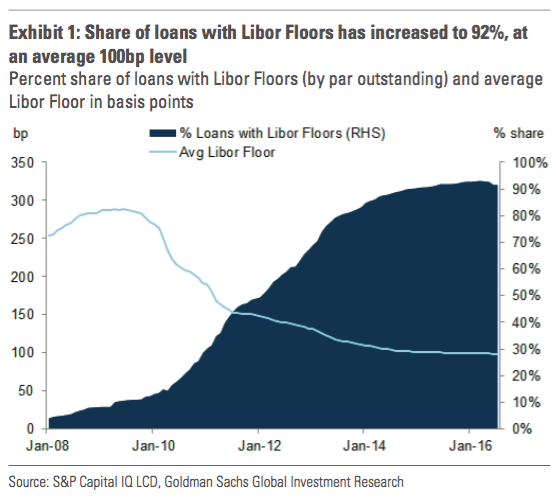

Well, that's not going to make investors in CLO equity tranches very happy. Here's the problem. More than 90% of loans have LIBOR floors.

(Chart: Goldman)

I know, I know, this sounds complicated already, but don't lose me here, I've got your back.

Ok, so you're a CLO (collateralized loan obligation). You bundle loans, slice them up, and sell them to investors. Your assets are the loans, your liabilities are payments to investors in the CLO. After the crisis, the market puts LIBOR floors in place to make sure lenders don't get shafted if the post-crisis easy money regime drives rates into the ground.

Typically, the floor is 100 bps. Basically, you - the CLO - get 100 bps guaranteed plus a spread. If LIBOR rises above the floor, you get whatever LIBOR is plus that same spread.

Simple enough, right? Now think about this. Your liabilities don't work that way. Investors in the CLO get the floating rate. Whatever's left over after all the other tranches get paid goes to the equity tranche. Well, as long as LIBOR is below 100 bps (the floor), the spread between the LIBOR floor and whatever LIBOR actually is is basically just free money for the equity tranche. Let's say you're in the equity tranche and LIBOR is 25 bps. Well, if you're leveraged 10 times, you're picking up 7.5% per year. Here's how Goldman explains it:

Rising Libor rates has most directly affected holders of CLO equity tranches, who have benefited from the "subsidy" gained from the spread between Libor rates and the Libor floor on the asset side, while liabilities "float," and are paid without Libor floors. In the low Libor environment over the past few years, CLO equity investors have benefited from this disconnect between assets and liabilities. A year ago, for example, the 75bp subsidy from the asset side of equity CLOs-calculated as the differential between the spot Libor rate (25bp in July last year) and the average Libor floor (100bp) - would increase total cash payments to equity holders by 7.5% on an annualized basis for CLO equity investors that are 10x levered.

However, as Libor has increased recently, the income that CLO equity investors have earned on the floor vs. Libor arb has stagnated. With only a 20bp differential between Libor spot (80bp) and Libor floors (still at 100bp), the equity distribution from the Libor floor decreases to only 2% per annum compared with 7.5% a year ago.

"If Libor spiked tomorrow to anything less than 100 basis points, CLO equities would be under extreme pressure and new CLO formation would probably stop in its tracks," Bruce Martin, who ran non-distressed corporate credit at Angelo Gordon, said in an e-mail Bloomberg got ahold of last May. Here's how Reuters explained the situation earlier this month:

Libor floors have directly benefited holders of CLO equity, the most junior slice of the funds. When Libor was 25 basis points and most loans had floors of 100 basis points, the extra 75 basis points increased annual cash payments to equity investors by around 7.5 percent for CLOs with 10 times leverage, said Mia Qian, a CLO analyst at Morgan Stanley.

CLO equity returns fall when Libor rises but remains below the level of the floor.

Loan interest payments to CLOs remain constant because of the floors in place.

CLOs do not have floors, however, and the rate funds pay to their debt investors rises as Libor increases, which eats up the excess spread that equity holders would otherwise have received.

And here's Moody's warning about the same dynamic way back in 2014:

Increases in short-term rates, widely expected to take place next year, would be a "credit negative" event for U.S.-based CLOs because of the resulting reduction in credit enhancement called excess spread. This is the difference between the interest rate on the notes issued by CLOs and the interest rates on the loans that they acquire. Interest rates on both their liabilities and assets are expressed as a spread over the London Interbank Offered Rate, or Libor.

Moody's warned that the impact of a spike in three-month Libor would be more pronounced in newer CLOs because a "greater portion" of the loans backing so-called CLO 2.0s, those issued since the financial crisis, include Libor floors. These floors, which can range from less than a percentage point to 1.5 percentage points or more, are designed to protect loan investors from falling interest rates, since the spread on a loan cannot fall below the floor, guaranteeing a minimum return. But when interest rates rise, the Libor floor also acts as an anchor.

"The most direct, and likely most significant, impact of rising rates on CLOs would be a roughly 75 bps decline in excess spread, which is a source of credit enhancement for CLOs," the report, for which Moody's researcher Jeremy Gluck was lead analyst, states. "This loss of excess spread would occur because the interest rates paid on CLOs' mostly floating-rate liabilities will rise nearly in tandem with Libor, while the yields on CLOs' floating-rate assets would not rise until Libor exceeds the relevant floor levels."

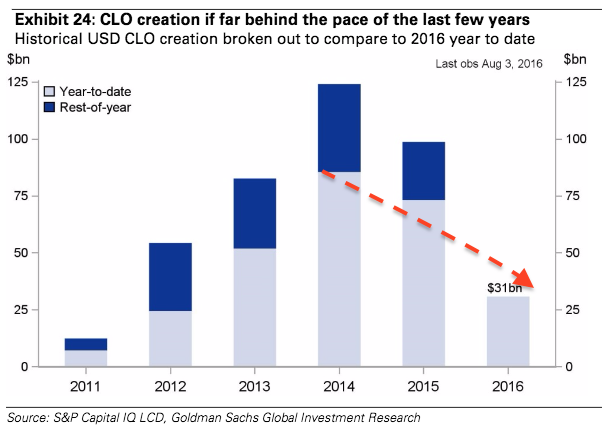

Ok, now let's think about what this means for the market. Here's CLO issuance YTD:

(Chart: Goldman)

As you can see, there's waning interest in the market. That's of course partly due to new regulations on the horizon which some issuers say pose an existential threat to a key funding source for corporate America (read more on that here).

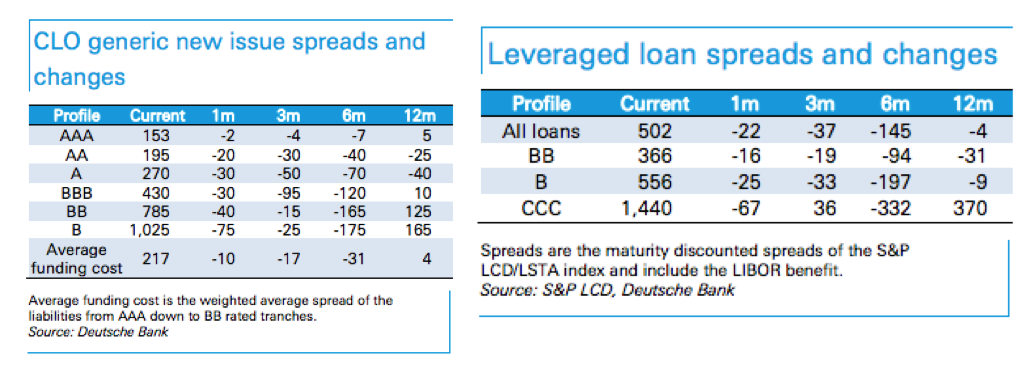

Now the thing is, spreads have continued to grind tighter thanks largely to the irrational exuberance created by continued central bank accommodation. The same can generally be said for leveraged loan spreads. "Despite the signs of rising idiosyncratic risk in US, European and US CLO liability spreads have followed tightening in loan spreads, but still have a little room for further compression," Citi noted, late last month.

But note that the longer-term picture is less sanguine. Have a look at the 12m CLO new issue spread changes for the more junior tranches and also the 12m spread change for CCC leveraged loans.

.

.

(Charts: Deutsche Bank)

(Charts: Deutsche Bank)Ok, now have a look at this:

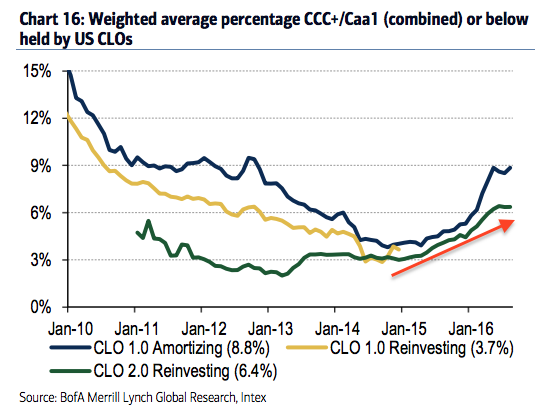

(Chart: BofAML)

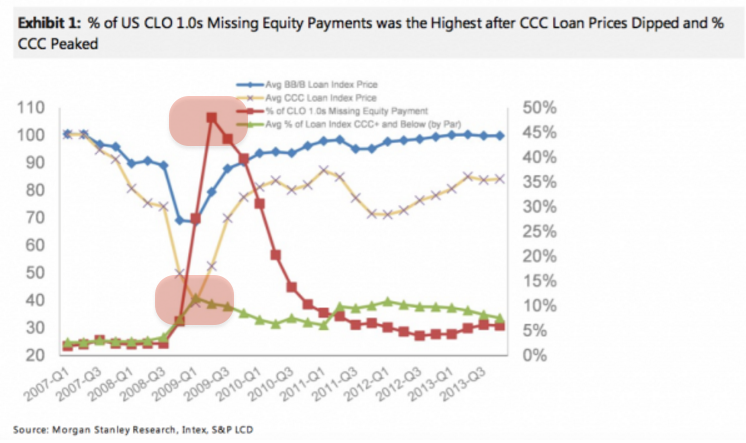

Think of that as the percentage of US CLO collateral pools that's comprised of crap. For 2.0s, it's now above 6%. Do you know what happened to 1.0s back in 2008 when that figure rose above 6%? This:

(Chart: Morgan Stanley)

(Chart: Morgan Stanley)Basically, the equity tranche was screwed. Here's what Moody's had to say on Friday in the rating agency's latest quarterly review of the space:

While the pace of rating downgrades slowed as Moody's completed its review of commodity companies, and liquidity stress eased, other measures of credit quality weakened in the second quarter. The US speculative-grade default rose, as did the percentage of high-yield loans with covenant-lite structures, and the long-term refunding index deteriorated. All told, four of Moody's seven CLO collateral risk measures weakened.

In the past quarter, Moody's downgraded junior and mezzanine notes from 10 CLOs in their amortization periods due to tail risk stemming from credit deterioration.

So tying this all together, the effect the new money market fund regulatory regime is having on LIBOR has the potential to strike yet another body blow to a CLO market that's already in effect dying out thanks in part to still more new regulations ostensibly designed to keep markets safer.

"It is just one more negative sentiment that will weigh on a currently weak market," Steven Oh, global head of credit and fixed income at PineBridge Investments, which oversees about US$77.6 billion of assets told Reuters late last year.

Why should you care? Well, because CLOs buy some 60% of the leveraged loans used to finance things like M&A. Here's how Gretchen Bergstresser, a senior portfolio manager at CVC Credit Partners, put it to Bloomberg, referencing the new risk retention rules for CLOs:

Risk retention has the potential to significantly reduce CLO formation, and by extension this would hurt the loan market and the availability of financing to U.S. companies.

Great. So just think about this for a second. You've got one set of regulations (MMF reform) that's set to reduce financing for corporates by reducing the pool of cash available for the purchase of commercial paper by up to $800 billion. That, in turn, is driving up LIBOR which gradually erodes an effective subsidy for CLO equity tranche investors at a time when i) still more regulations are already weighing on CLO issuance, and ii) equity tranche investors are already staring down an inevitable default cycle. And again, CLO issuance is another key funding source for corporations.

Way to go Washington.

In the end, this is what I mean when I say that you have to think about markets holistically; never in isolation. It's the butterfly effect in action.

Hopefully, you can see why all of this is important when it comes to thinking about your investments. These are the kinds of structural shifts that, if mismanaged, can lead to "accidents."

Let me close with a quote from Meredith Coffey, the Loan Syndications and Trading Association's executive vice president, who spoke to Bloomberg:

While risk retention is esoteric, and folks don't always see the connection to their lives, in reality, it is so consequential to the loan market, companies and the economy that of course the LSTA has spent years educating many folks on these issues.

Thanks for your efforts Meredith. But trust me, you'll need to spend many more years and endure many more crashes before "folks" get it.

0 comments:

Publicar un comentario