What Are The Takeaways From Janet Yellen's Speech For Gold Investors?

Hebba Investments

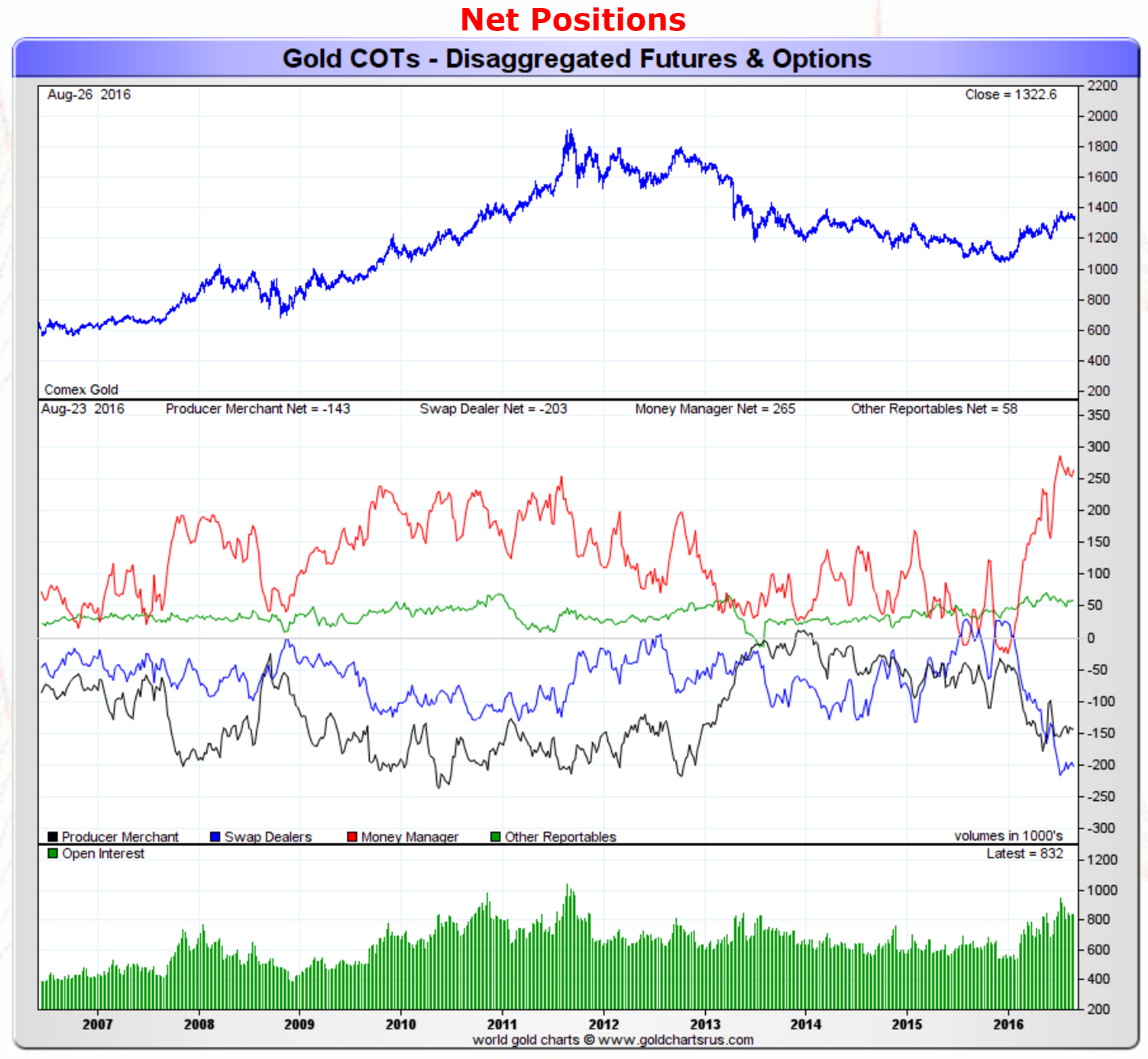

The latest COT report surprisingly showed a net increase in speculative bulls despite a drop in the gold price which was negative.

Yellen's speech was a bit hawkish but in it she introduced some surprising inflationary measures as future monetary policy tools.

Fed Vice Chair Fischer is pushing one or two rate hikes if the data supports it and thus next week's jobs report is extremely important.

With positioning still very bullish and a critical catalyst coming in Friday jobs report we hold our core gold positions but wish to wait further before re-establishing sold positions.

Yellen's speech was a bit hawkish but in it she introduced some surprising inflationary measures as future monetary policy tools.

Fed Vice Chair Fischer is pushing one or two rate hikes if the data supports it and thus next week's jobs report is extremely important.

With positioning still very bullish and a critical catalyst coming in Friday jobs report we hold our core gold positions but wish to wait further before re-establishing sold positions.

The latest COT report showed little movement in trader positions before the Yellen. But since this report only included positions as of Tuesday, it didn't include Wednesday's bear raid and trader responses to Ms. Yellen's speech on Friday. Nevertheless, we saw an increase in speculative gold longs (which surprised us), a decrease in speculative shorts, and also a decrease in the gold price - which is a bit unusual as the gold price tends to follow the speculative money during the COT report week. That means that despite positive speculative flows there's a bit of selling that is over and above these flows and causing a drop in the gold price.

Finally, we will comment on our thoughts on Ms. Yellen's speech and its implications for the gold price. We will give our view and will get a little more into some of these details but before that let us give investors a quick overview into the COT report for those who are not familiar with it.

About the COT Report

The COT report is issued by the CFTC every Friday, to provide market participants a breakdown of each Tuesday's open interest for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. In plain English, this is a report that shows what positions major traders are taking in a number of financial and commodity markets.

Though there is never one report or tool that can give you certainty about where prices are headed in the future, the COT report does allow the small investors a way to see what larger traders are doing and to possibly position their positions accordingly. For example, if there is a large managed money short interest in gold, that is often an indicator that a rally may be coming because the market is overly pessimistic and saturated with shorts - so you may want to take a long position.

The big disadvantage to the COT report is that it is issued on Friday but only contains Tuesday's data - so there is a three day lag between the report and the actual positioning of traders. This is an eternity by short-term investing standards, and by the time the new report is issued it has already missed a large amount of trading activity.

There are many different ways to read the COT report, and there are many analysts that focus specifically on this report (we are not one of them) so we won't claim to be the exports on it.

What we focus on in this report is the "Managed Money" positions and total open interest as it gives us an idea of how much interest there is in the gold market and how the short-term players are positioned.

This Week's Gold COT Report

This week's report showed an increase in speculative gold longs and a decrease in speculative shorts with longs increasing by 6,633 contracts and shorts closing out 4,645 contracts on the week. Despite the positive increase in net positions which usually is paired with an increase in the gold price, we actually saw a slight drop in the gold price - suggesting that speculative traders boosting long positions wasn't enough to counter the selling in gold from other entitites.

Moving on, the net position of all gold traders can be seen below:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red-line represents the net speculative gold positions of money managers (the biggest category of speculative trader), and as investors can see, speculative traders have slightly pulled back from all-time high positions are now net long by around 265,000 contracts. Not much of a pull-back yet in gold or in gold sentiment as speculative traders remain extremely bullish.

As for silver, the action week's action looked like the following:

Source: Sharelynx Gold Charts

Source: Sharelynx Gold Charts

The red line which represents the net speculative positions of money managers, continued its pullback as speculative silver traders cut their long positions and increased their short positions.

Earlier in the week, we published a piece that showed extremely poor silver demand from bullion investors as US Mint sales of silver eagles have been very weak - if speculative demand from paper silver investors doesn't keep up we could see a sizable drop in silver under $18 or $17 dollar level.

Our Take on Janet Yellen's Jackson Hole Speech

We would be remiss to write an article on gold and not at least mention Yellen's Jackson Hole speech (see the transcript here), which is generally the most anticipated "Fed Speak" of the year. In our opinion her speech was a bit hawkish (which is what we expected) because she did mention that the data was much improved and "…in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months."

That was further emphasized by Fed Vice Chair Stanley Fischer as he put the focus on next week's August jobs report and forward data, in an interview with CNBC. In the interview, Fischer said that Yellen's comments were consistent with a September rate hike and possibly two hikes this year, but the Fed won't know the course of normalization until it sees the data.

Takeaway #1: Next Friday's Non-Farm Payrolls report will be extremely important in determining the odds of a September rate hike.

Also, Ms. Yellen mentioned something very interesting in terms of future potential monetary policy (emphasis ours):

…future policymakers might choose to consider some additional tools that have been employed by other central banks, though adding them to our toolkit would require a very careful weighing of costs and benefits and, in some cases, could require legislation. For example, future policymakers may wish to explore the possibility of purchasing a broader range of assets. Beyond that, some observers have suggested raising the FOMC's 2 percent inflation objective or implementing policy through alternative monetary policy frameworks, such as price-level or nominal GDP targeting.

Purchasing alternative assets, increasing inflation expectations, and price-level targeting (i.e. injecting money until GDP rises) are all extremely dovish measures. Ms. Yellen caveats the statement by saying the "Fed isn't actively considering these tools", but we don't buy it as central bankers tend to mislead (the Bank of Japan drove interest rates negative a week after denying they would ever consider it) and if they weren't at least being discussed then why mention them at all?

What this should mean for investors that the "Fed Put" is even greater than it was before the speech as the next crisis could mean we see the Fed publicly buying corporate bonds and stocks to directly inject money into the system. If anything, this suggests to us that the next crisis will be the opposite of what policy makers are protecting against as markets tend to surprise - thus expect inflation and not deflation.

What This Means for Investors

The COT report was little moved for the week though we do note that while speculative investors increased net bullish positions the gold price dropped, which is bearish as it usually rises with speculative net position increases. This suggests there's a bit of weakness behind the scenes in the physical market and speculative traders are not strong enough to move the price higher. Of course, the report closed on Tuesday and thus doesn't include the later week moves in gold that drove it down to around $1320.

But the most important event in the gold market occurred on Friday as Janet Yellen gave her widely anticipated Jackson Hole policy speech. The speech was a bit hawkish but may have given investors a hint on the direction of future Fed fire-fighting maneuvers as she mentioned policy options such as purchasing "alternative" assets (think stocks and bonds) and increasing the inflation target from 2% to higher levels - all gold positive.

Finally, Vice Chair Stanley Fischer came out extremely hawkish and suggested the potential for two rate hikes and made next Friday's payrolls report extremely important as if it's a strong number then expect a September rate hike. We are of the opinion that the Fed wants to raise interest rates and will look to do so at the next practical opportunity.

While fundamentally raising or lowering interest rates by themselves is agnostic for gold as gold cares about the real rate and not the nominal interest rate as evidenced by gold rising in the rising interest rate environments (e.g. the 1970's and early/mid 2000's), the current narrative is that traders sell gold on the potential for rising rates and vice versa.

Thus we are still extremely cautious in gold as we are a bit worried about next week's job report being positive and knocking gold down, but we maintain our core positions in gold. But we aren't looking to re-establish any of our sold gold and silver positions just yet until we see more of a pullback in the metals or a bad jobs report and thus we think investors should hold off or lighten up on gold positions in the ETF's and miners such as the SPDR Gold Trust ETF (NYSEARCA:GLD), ETFS Physical Swiss Gold Trust ETF (NYSEARCA:SGOL), iShares Silver Trust (NYSEARCA:SLV), and miners such as Randgold (GOLD) and Barrick Gold (NYSE:ABX).

At $1320 we're getting more interested in buying back some of our sold gold positions but not quite yet as we await next week's job report.

0 comments:

Publicar un comentario