Buttonwood

The second big shift

The relationship between equity and bond values has changed again

.

INVESTORS who need income have traditionally opted for savings accounts and bonds. That was believed to be the safe approach. In the conventional view, equities were what you bought when you wanted long-term capital gains.

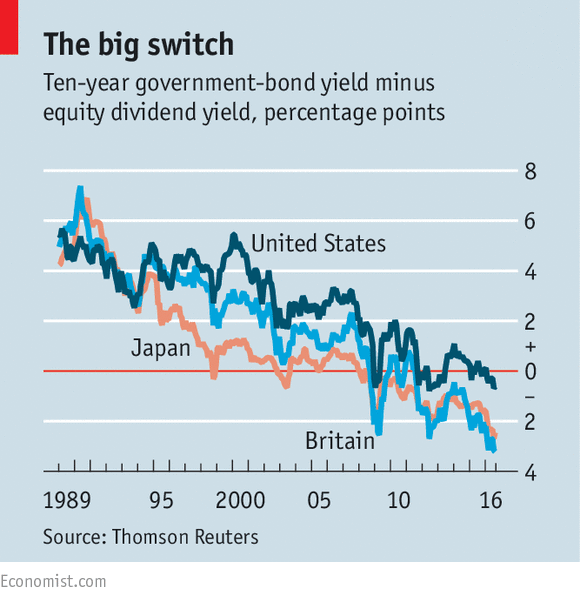

That view was always short-sighted; over 20-year periods around half of the total return from American shares comes from reinvesting dividends. But ignoring the income-generating appeal of equities looks particularly odd now. The dividend yield on shares in America, Britain and Japan is higher than the yield on ten-year government bonds; in the case of the latter two, the difference is more than two percentage points (see chart). The gap is nothing like as big in America, although many would argue that share buy-backs materially boost the effective yield.

For investors who started their careers in the 1980s and 1990s, this relationship looks very weird. For them, the norm was for bonds to offer a yield many percentage points higher than that from equities.

As a result, when, in 2003, the dividend yield on British shares rose above the government-bond yield for a few days, many investors saw it as an historic buying opportunity. London’s FTSE 100 index duly rallied sharply. A closer look at the chart suggests something significant has changed. Equities have frequently yielded more than bonds in both Britain and Japan since 2008, without signalling that shares were a steal.

Financial history shows that the valuation basis for equities and bonds has already undergone one historic change. Up until the late 1950s, it was quite common for equities to yield more than government bonds. That is because equities were perceived to be more risky. Companies pay dividends only after they have satisfied the demands of other creditors, in particular bondholders. The Depression had shown that equities could collapse in price and that many companies could go bust.

So, the institutional investors of the 1930s and 1940s thought it prudent to place the bulk of their assets in bonds.

But from the mid-1950s onwards, these big investors started to change their minds. Memories of the Depression faded. Equities might be individually risky but a diversified portfolio looked much more secure. Over time, the dividend income from shares would rise while the income from bonds was fixed. And as inflation soared in the 1960s and 1970s, that made holding bonds look like a very bad idea. The “cult of the equity” had arrived.

In other words, this first valuation shift between bonds and equities was down to a change in economic fundamentals and in the attitudes of institutional investors. Both factors are probably at play in this latest switch, too.

Since 2008 the developed world has struggled to generate either inflation or consistently rapid growth. That combination is better for bonds than it is for equities. In a sense equities have defied the odds, rallying strongly since the spring of 2009 despite sluggish economic growth.

The reason is that profits (in America in particular) have been high as a proportion of GDP, because wages have been held down. But it seems unlikely that profits can stay elevated indefinitely. And although a diversified portfolio of equities protects investors against the risk of individual company failure, they can still suffer significant losses from a market sell-off.

Japan’s Nikkei 225 is less than half its 1989 peak. Dividend income can be slashed in a crisis; it fell by 28% in America in 2008, for example.

Investor attitudes have also changed. Regulations mean that insurance companies and pension funds have reduced their exposure to equities and pushed up their bond holdings. They are no longer automatic buyers of equities when the market falls. The cult of the equity has lost some important followers.

Central banks have also become huge players in the government-bond markets, pushing yields to negative levels in many cases. That has led some commentators to argue that, rather than equities being cheap, bonds are ridiculously expensive.

This view may turn out to be right. But investors have been betting that Japanese bonds are overvalued for more than 20 years in a trade now known as the “widowmaker”. In the post-2008 world, bond yields seem likely to stay low. That should make investors cautious about using bond yields as a buy signal for equities. The income from equities looks very appealing and (in the absence of a recession) should provide support for share prices. But do not count on share prices rising sufficiently to push the dividend yield below bond yields again.

0 comments:

Publicar un comentario