Sayonara, Suckers

by: The Heisenberg

- I'm not worried about Japanese food.

- But I am worried about Japanese banks.

- And not for their own sake.

- But I am worried about Japanese banks.

- And not for their own sake.

- I'm not worried about Japanese food.

I know the best places to get it, the best things to order, the best sushi chefs, hell I even memorized the Japanese names for all of the a la carte sashimi.

But I am worried about Japanese banks. For one thing, the three biggest institutions are going to see their profits decline by something like $3 billion thanks to BoJ policy, but one could write volumes on that and besides, it's so self-evident as to not be very interesting.

Rather, what I want to talk about is Japanese banks' exposure to soaring LIBOR and to the crunch in prime money market funds. As you know, upcoming reforms are set to reduce the amount of unsecured funding available to banks and corporates by hundreds of billions of dollars (see here and here).

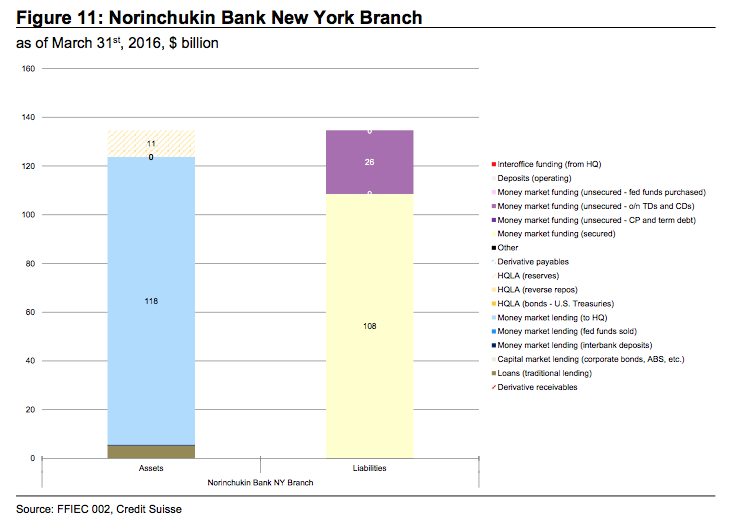

So that's the balance sheet for Norinchukin Bank's NY branch. Notice anything interesting there? I do. There's only $26 billion in unsecured funding. The rest of it is all repo (i.e. secured GCF). Here's how Credit Suisse explains this:

How come Norinchukin can pledge so much in Treasuries without affecting its LCR? Well, as an agricultural cooperative, Norinchukin is not subject to Basel III and so it can utilize its U.S. Treasury portfolio to a maximum extent to raise dollar funding cheaply in New York.

Ok, so that's interesting. Now this next part is key:

Norinchukin also taps the unsecured market to the tune of about $26 billion and if this source of unsecured funding slips away due to prime fund reform, Norinchukin will have that much more funding to do in the repo market, pulling o/n GCF and tri-party repo rates higher and wider. This is because the intermediation of flows away from unsecured to secured markets will flow through primary dealers' balance sheets, and primary dealers -who since July 1st are now all subject to daily average balance sheet reporting - will charge for a greater use of their much scarcer balance sheets through wider repo spreads.

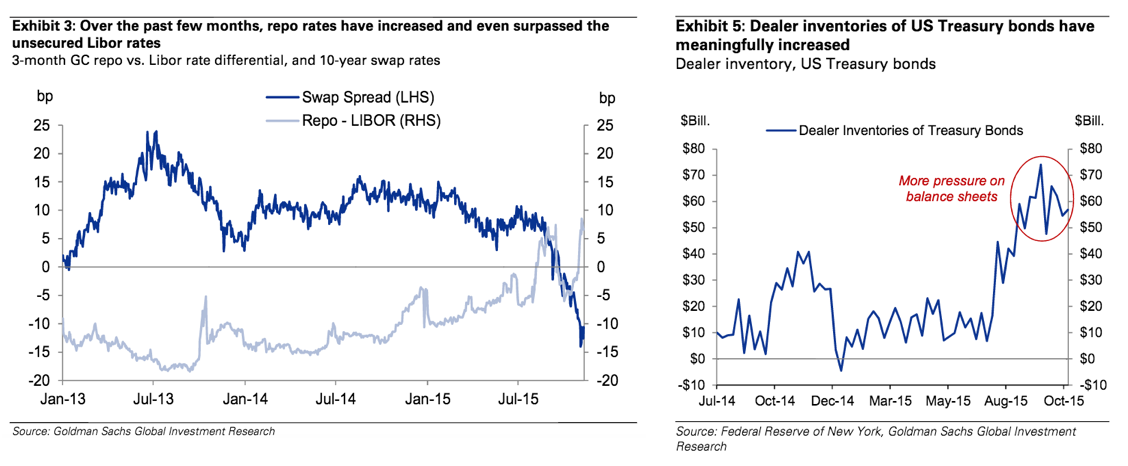

Remember what Goldman said last November about this same phenomenon as it related to foreign FX reserve selling? No? Neither do I, but I know they said something. Wait... let me dig it up.

Ok, found it. Here:

Key to the recent back-up in repo rates have been new bank leverage ratio limits and liquidity rules, especially the supplementary leverage ratio which applies to both on- and off-balance sheet assets and exposures. These requirements make a long position in Treasury bonds vs. swaps more onerous to execute and thus less compelling on a return-on-equity basis. As a consequence, the "convenience yield" on Treasury bonds, that is, the value that investors assign to the liquidity and safety attributes offered by Treasury bonds may have declined.

The selling pressure on Treasury bonds from FX reserve managers has led to a significant increase in dealers' inventories, putting more pressure on balance sheets and likely pushing GC repo rates higher.

{kind=link}

{kind=link}

Don't get bogged down in the terminology. It's supply and demand. You want me to inventory your general collateral (i.e. use my balance sheet), well then you're going to have to pay up because every one else wants the same thing.

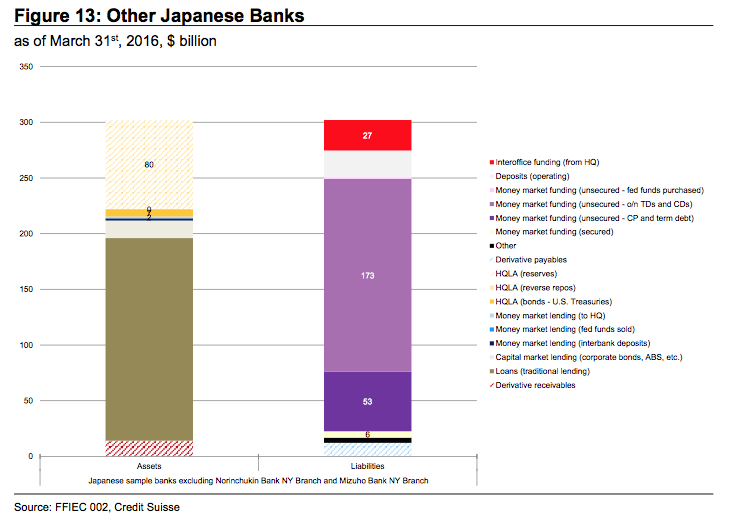

Ok, now let's look at the flip side. Here's the combined balance sheets for New York branches of Sumitomo Mitsui Banking Corp. and the Bank of Tokyo Mitsubishi plus some others.

(Chart: Credit Suisse)

(Chart: Credit Suisse)

{kind=link}

See that giant block of purple and light purple on the liabilities side and that giant block of Exorcist-puke-green on the assets side? Yeah that's the very definition on maturity mismatch.

So here's Credit Suisse explaining what has to happen:

So here's Credit Suisse explaining what has to happen:

As unsecured funding from prime funds becomes less available and more expensive, they will have to pay higher rates to take down a large share of a shrinking CP and CD market (the path they have chosen to date), step up their term debt issuance (no sign to date), or tap the FX swap market through headquarters (no sign yet, as it is costlier than the first).

The sheer size of the New York branches of Sumitumo and the Bank of Tokyo-Mitsubishi is important to highlight in this regard as they are the single largest issuers of unsecured paper to prime money funds. In recent weeks, they have been issuing three-month paper at 90 bps, which while much higher than the comparable Libor fixing at 75 bps, is way cheaper than the all-in cost of raising three-month dollar funding via FX swaps at 125 bps.

In this sense, Sumitomo Mitsui and the Bank of Tokyo-Mitsubishi appear to be the marginal price setters of the term premium in unsecured money markets at present.

So basically, they'll pay up for the shrinking pie of MMF funds available for unsecured lending up to and until that cost matches the cost of tapping FX swap lines plus some stigma premium.

Here's Barclays to explain the very same thing in far more words than I used:

Here's Barclays to explain the very same thing in far more words than I used:

The Fed maintains swap lines with other central banks, including the ECB, Bank of England, Bank of Canada, and Swiss National Bank, as well. The dollar rate on these transactions is equal to 3m OIS+50bp. Thus, to the extent that the Japanese banks are seen as the price setters in the market for unsecured short-term paper, the swap line should establish a ceiling on Libor - that is, the rate at which a Japanese bank is indifferent between borrowing from money funds or via the cross-currency swap market and using the facility.

But why might an institution prefer to pay more than 92bp (3m OIS+50bp) by borrowing from a shrinking pool of ever shorter maturity prime fund cash?

An institution might borrow at higher rates if it felt that there was some stigma attached to the program.

A Japanese bank wishing to use the BOJ/Fed swap line has two choices. It could pledge JGBs from its inventory to the BOJ and receive dollars in return. Or it could reverse in JGBs from the BOJ, effectively converting its current account holdings at the central bank into dollars. The total cost - on top of the 3m+50bp dollar rate - reflects either of these two approaches to "getting to the swap line". As a result, the 50bp spread to 3m OIS is in practice a soft ceiling on 3m Libor.

At this point, if you follow Heisenberg, you're probably starting to understand why I started pounding the table on this last month (see here and here). An upcoming piece on CLO impact (should be out on Sunday) will drive the point home further.

Quite frankly, this is all anyone is talking about on the Street in terms of market (NYSEARCA:SPY) outlook. It's pervasive and ubiquitous. Need more proof? Here's some excellent color out of Deutsche Bank from their weekly US Fixed Income report (one of the best reads on the Street.. thanks Dominic Konstam and co.):

It's important to remember that MMFs are intermediaries in the short-term cash market and not the final users of corporate cash. That category belongs to the US branches of foreign banks. According to Crane data, institutional prime money funds managed $760 billion of assets at the end of July, with $570 billion of those assets invested across short-term instruments issued by foreign financial institutions. Unlike their US counterparties, non-US banks do not have access to traditional retail deposits. Whereas 80 percent of a US bank's balance sheet is funded by small deposits, that number is just 11 percent for a non-US bank. Hence, they must raise funds somewhere else, such as in the money markets. But how much do foreign banks really rely on MMFs, and if corporate cash ceases to flow into prime MMFs after October, what will happen to foreign banks when the music stops?

The table below breaks down the amount and maturity of short-term instruments foreign banks used to raise funds from institutional prime MMFs as of July 31. Around $424 billion of the $570 billion total were due in 30 days or less. Most banks would prefer to push out the zero-maturity time deposits and increase the amount and maturity of their CDs and CPs. Doing so would reduce their 30-day outflow calculation and improve their LCR ratio. However, redemption uncertainties around reform deadline are causing prime MMFs to do the exact opposite of funding banks at increasingly short maturities, which means that pressure could be building for some banks on the LCR front.

Remember what I said earlier this week? No? That's ok. Here's a refresher:

Now if you're thinking two steps ahead (and should always be doing that in anything you do) you can anticipate how this could trigger a self-feeding loop. You're a prime MMF manager. You have no idea how much money is going to leave your fund between now and October, when the new rules kick in. That creates a maturity mismatch problem. That is, you can't buy any three-month paper because that would tie up funds past the date on which the new regulations kick in. But if you can't take any duration risk, guess what happens to yields? That's right, they fall. And the lower yields on your fund go, the less attractive your fund looks to investors versus a government MMF. That means even more outflows. And around we go.

So, yeah. The exact same thing.

Make no mistake, you will hear more and more and more about this over the next two months. It's quickly becoming one of the more critical market topics as everyone struggles to determine exactly where the fallout will show up.

I can tell you where it probably won't show up. At the sushi restaurant where I'm headed for dinner. The guy pays cash for his fish as I imagine he does for his rent. Smart guy.

For now, sayonara,

0 comments:

Publicar un comentario